This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

This guide translates vodka supply-market signals into concrete sourcing moves (contract structure, award design, and governance). It’s written for procurement leaders who know strategic sourcing well, but may not live in spirits day-to-day—so it focuses on the practical “what to do next” across neutral spirit, packaging, co-packing, and logistics.

Analyzed at: Apr, 2026

Access the live market signals behind this analysis.

Insight: Vodka input costs rarely move in sync. The “alpha” for procurement is exploiting timing gaps between (a) feedstock/energy moves, (b) neutral spirit pass-through, and (c) packaging and freight resets.

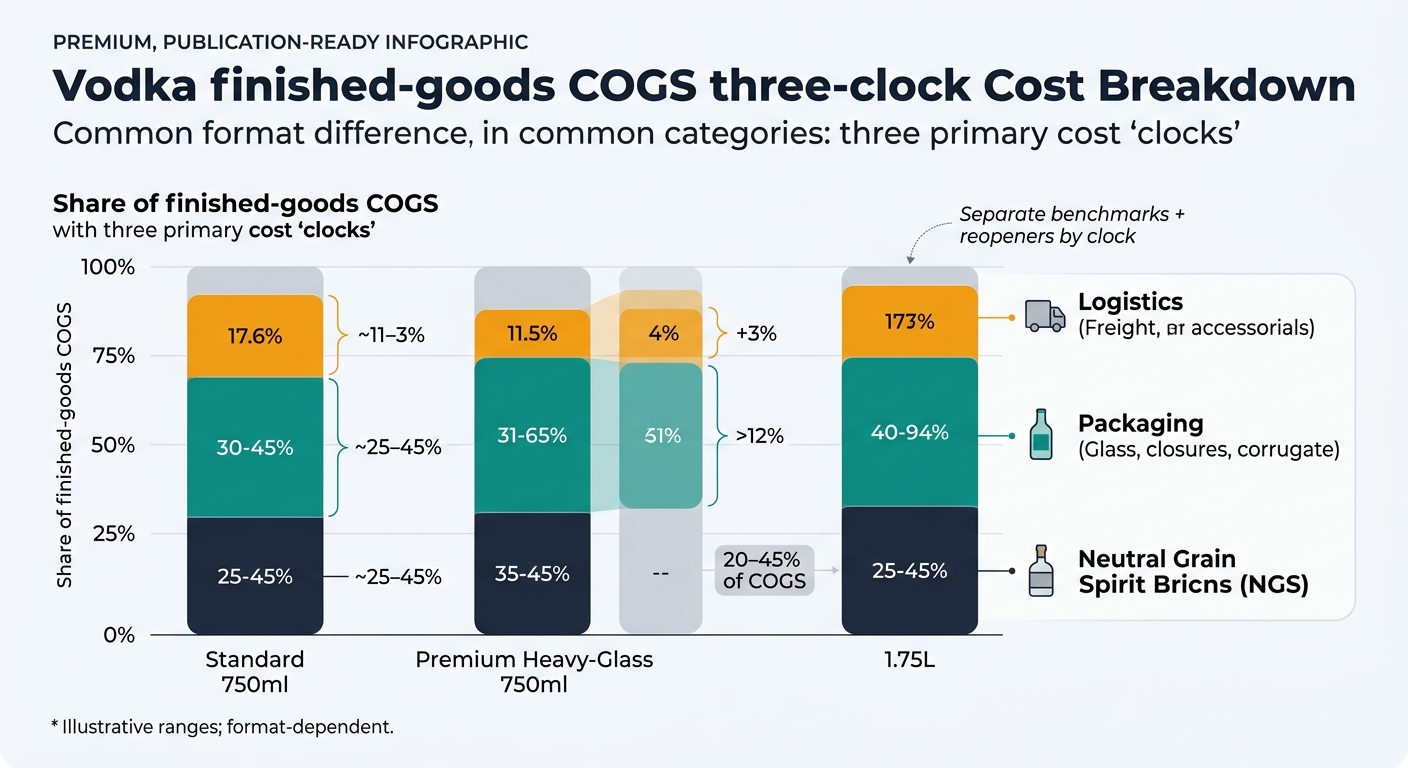

Data (validated framing; ranges are format-dependent): In a typical U.S. supply model, neutral grain spirit (NGS) often represents ~25–45% of finished goods COGS (varies by proof, freight mode, and packaging), but glass + closure + corrugate can rival or exceed spirit cost for premium/heavy-glass formats. When glass tightens, suppliers preserve margin via packaging surcharges even if grain softens; when trucking loosens or tightens, suppliers may delay freight relief (or push increases) until contract reopeners.

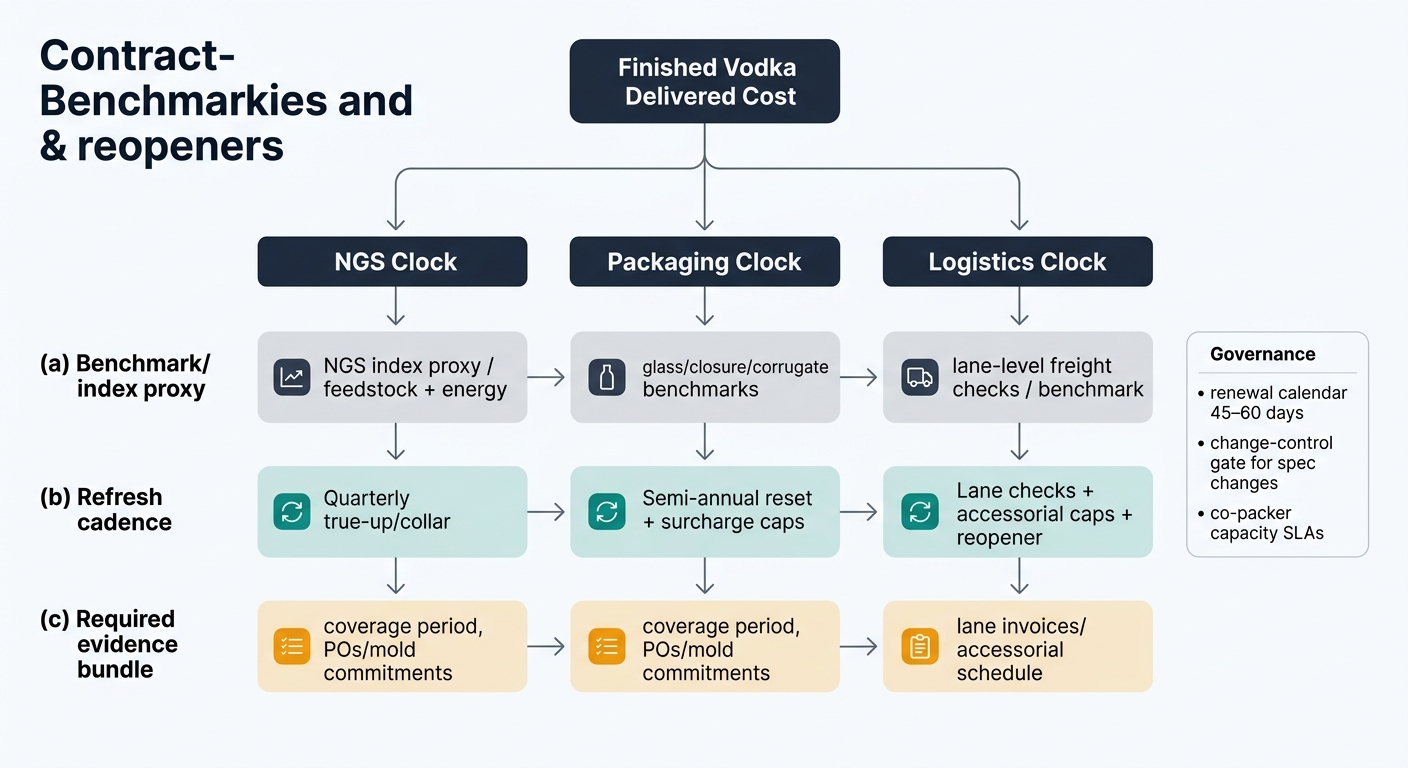

Procurement impact: The best outcomes come from separating negotiations into three clocks:

Quick win: Build a renewal calendar that forces three independent benchmarks (NGS index proxy, glass/closure benchmarks, lane-level freight checks) 45–60 days before renewal, so you negotiate the spread, not a blended story.

Insight: Vodka pricing “disconnects” are structural. Even when upstream grain prices fall, your delivered bottled cost may not—because packaging and capacity constraints create a price floor, and inventory/contract lags delay pass-through.

Data (decision-grade examples; treat as typical patterns, not guarantees):

Procurement impact (how to turn disconnect into leverage):

Key Takeaways:Your best savings windows appear when one clock moves down (grain) while another clock is sticky (packaging/capacity) or moving up (freight). Separate them contractually so you can capture the down-move without accepting unrelated up-moves.

Insight: The difference isn’t “more data.” It’s converting external signals into contract structure, award design, and inventory posture.

Data (before → after, realistic metrics):

| Decision area | Traditional approach (typical) | Intelligence-driven approach (typical) | Measurable outcome |

|---|---|---|---|

| NGS negotiation | Annual reset, supplier narrative | Quarterly index-linked true-up + evidence pack | 2–6% lower NGS variance vs plan |

| Packaging continuity | Single bottle spec, long lead surprises | Dual-approved bottle/closure + mold lead-time tracking | 30–60% reduction in line-stoppage risk from packaging |

| Co-packer performance | Price-per-case focus | Capacity SLAs + OTIF + changeover governance | 2–5 pts OTIF improvement; fewer expedites |

| Freight | Delivered price, no lane checks | Lane benchmarking + accessorial caps | 1–4% landed cost reduction on heavy-glass SKUs |

Procurement impact:

Quick win: Create a monthly “vodka cost delta” memo: top 5 drivers, % impact, and which contracts have reopeners vs are fixed.

Insight: Don’t trade away long-term packaging security for short-term spirit relief.

Data: When glass lead times extend (often quoted 12–20+ weeks for custom), suppliers can hold your schedule hostage.

Procurement impact (play): Lock packaging capacity (molds/POs) first; then negotiate NGS with a downward-only collar for the next 1–2 quarters.

Insight: MOQ pressure is often a utilization signal, not a true cost necessity.

Data: Larger runs reduce changeover loss, but the working capital + obsolescence can exceed the conversion savings.

Procurement impact (play): Offer a run-plan commitment (e.g., 3 smaller locked windows) instead of one large MOQ; trade schedule certainty for MOQ flexibility.

Insight: Small packaging changes create outsized regulatory and scrap risk.

Data: Label fit, closure torque, and case pack changes can trigger rework and write-offs; even a 1% scrap increase on premium glass can erase negotiated savings.

Procurement impact (play): Require a change-control gate: cost impact, validation plan, depletion strategy for old components, and who pays for scrap. Also confirm whether any label changes require a new COLA or qualify as allowable revisions under TTB rules; involve compliance/legal as needed. [2]

Insight: Vodka is a clean example of multi-clock cost behavior—exactly what happens in other “packaging-heavy” or “capacity-allocated” categories.

Data: Similar disconnect patterns show up in:

Procurement impact: Once your team learns to separate clocks and contract them independently, you reduce variance across multiple categories—not just spirits.

Insight: Vodka procurement rewards teams who can prove what should move, when it should move, and which part of the quote is sticky.

Data: Most missed savings come from (i) blended pricing that hides offsets, (ii) packaging dependency that isn’t governed, and (iii) co-packer capacity that isn’t contract-managed.

Procurement impact: The next level of performance is not another negotiation workshop—it’s an operating rhythm that continuously answers:

Logical next step framing: If you can’t quantify the spread between NGS, packaging, and freight in near real time, you’ll keep debating anecdotes—and your results will track the index rather than beat it.

Start Making These Sourcing Decisions with Live Signals

Tridge Eye — The strategy playbook above works — but only with current data feeding it. Real-time price movements, supplier risk scores, and origin alerts turn these frameworks into daily competitive advantages.