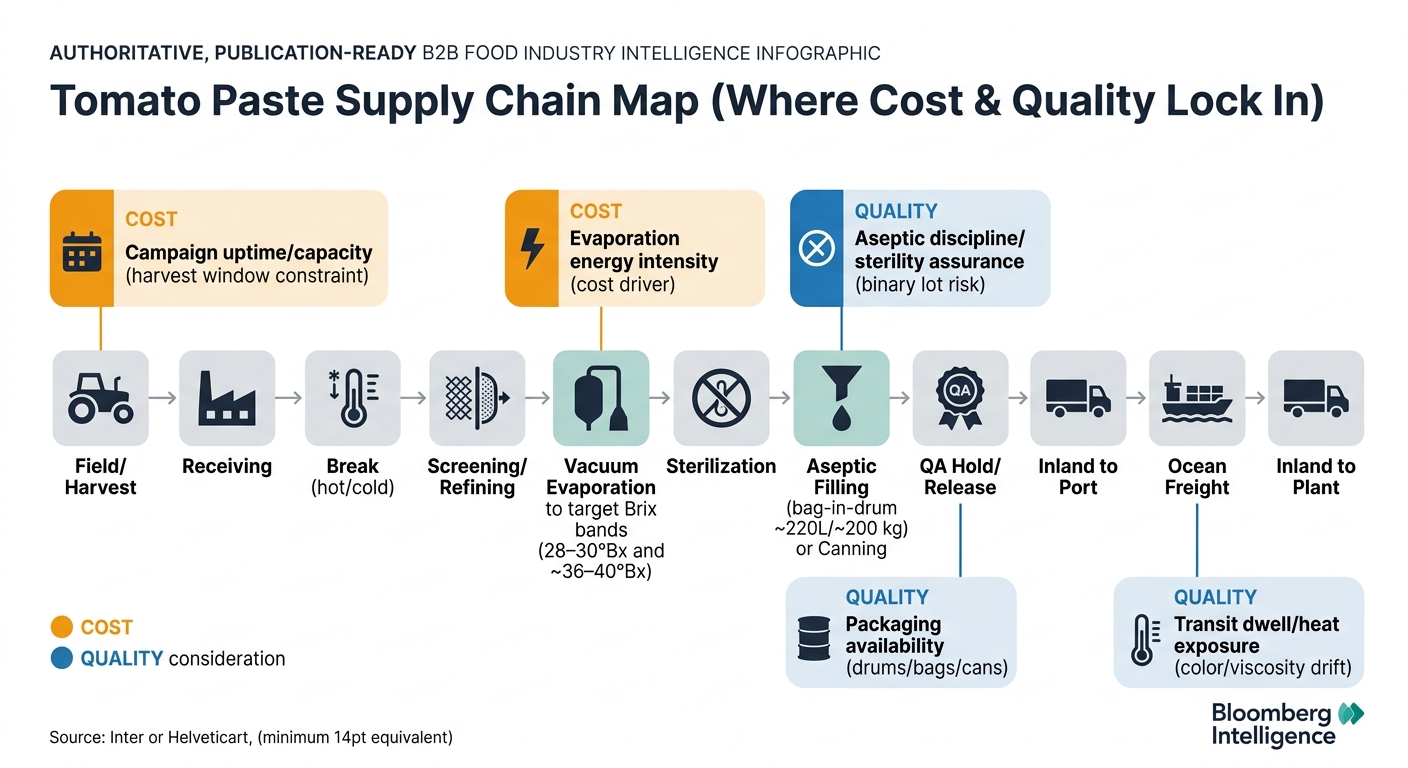

Tomato paste looks like a storable commodity, but procurement outcomes are decided by a short harvest “campaign” and a long inventory tail. This guide maps where landed cost and quality get locked in—so sourcing teams can set the right specs, choose formats, and build resilience without overpaying or over-constraining the supplier pool.

Tomato paste is manufactured in a compressed, harvest-driven “campaign” window, then stored and shipped for months as a shelf-stable concentrate. That physical reality creates a supply chain where capacity, energy, and packaging are the fixed bottlenecks—not just farm yield.

Insight: The chain is built around a few weeks of high-throughput processing, followed by long-duration inventory holding and global distribution.

Data: Industrial paste is commonly traded in standardized concentration bands—especially 28–30°Bx (double-concentrated) and ~36–40°Bx (triple-concentrated / industrial)—and bulk movement is dominated by aseptic formats such as bag-in-drum. [1]

Procurement Impact: Your “true supply base” is defined by who can (1) run reliably during campaign peaks, (2) sterilize/fill aseptically without failures, and (3) secure drums/bags and container capacity—because those nodes hard-limit availability even when tomatoes are plentiful.

Insight: Tomato paste cost is not “one thing.” It is a layered build-up where upstream solids/yield set the tonnage requirement, processing energy sets the conversion cost, and packaging + logistics determine how much of that value survives to your plant.

Data: The category is sold in standardized concentration forms (commonly 28–30°Bx and ~36–40°Bx), and buyers often control usability with measurable indices like soluble solids (Brix) and consistency tests (commonly Bostwick in industry practice). [1]

Procurement Impact: Even before any commercial conversation, you can “see” where cost will be sticky: solids/yield at farm, evaporation energy at processing, aseptic materials and sterilization discipline at packing, and container/port exposure at logistics.

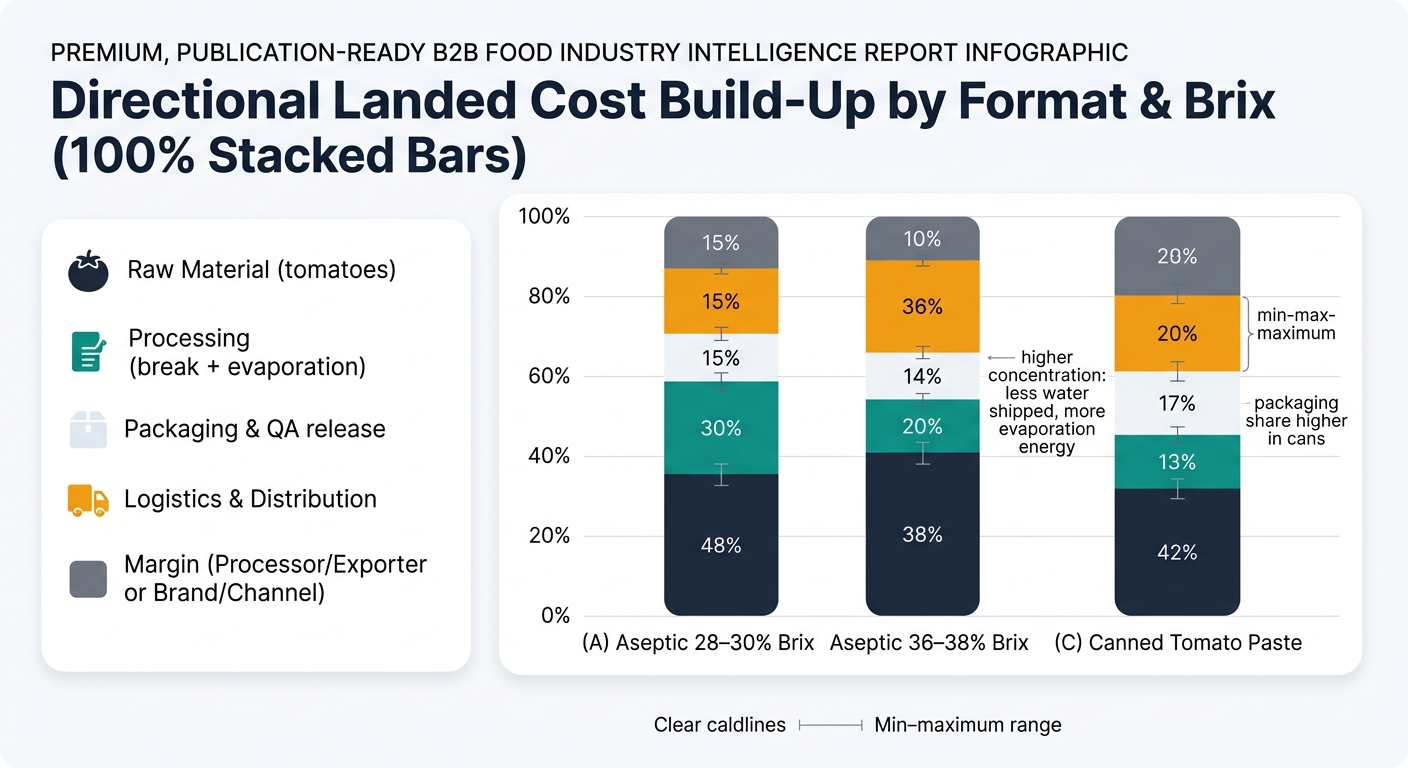

These ratios are directional (they vary by origin, contract terms, concentration, season, and incoterms), but they are structurally plausible and each table sums to ~100%.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw Material Cost (tomatoes) | 30–40% | Driven by solids/yield and harvest deliverability. |

| Processing (break + evaporation) | 20–30% | Energy + throughput + downtime during campaign. |

| Packaging & QA release | 12–18% | Aseptic bags, drums, sterilization discipline, lab testing/holds. |

| Logistics & Distribution | 10–18% | Inland + ocean + port dwell; temperature handling matters. |

| Processor/Exporter Margin | 8–15% | Varies with utilization, inventory position, and quality tier. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw Material Cost (tomatoes) | 28–38% | Higher Brix reduces shipped water but increases processing intensity. |

| Processing (break + evaporation) | 25–35% | More evaporation work; energy and capacity utilization dominate. |

| Packaging & QA release | 10–16% | Similar physical packaging; tighter functional consistency expectations. |

| Logistics & Distribution | 8–15% | Less water shipped per unit solids can help freight efficiency. |

| Processor/Exporter Margin | 8–15% | Often reflects tighter spec/functional performance demands. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw Material Cost (tomatoes) | 20–30% | Tomatoes are diluted by downstream packaging/branding costs. |

| Processing (break + evaporation) | 15–25% | Similar core processing, but canning adds additional thermal/handling steps. |

| Packaging & QA release | 20–35% | Tinplate/ends, seam integrity controls, labeling/cartons. |

| Logistics & Distribution | 10–20% | Heavier, less space-efficient than bulk aseptic; more handling steps. |

| Brand/Co-pack/Channel Margin | 15–30% | Retail/foodservice channel structure adds margin layers. |

Insight: Tomato paste behaves like a storable commodity, but it is produced like a perishable—so constraints show up as “physics problems” (capacity, sterility, packaging, transit) rather than as simple supply/demand.

Data: Objective color control is widely used in the tomato industry, with instrument-based measurement positioned as a standard way to reduce downgrades versus subjective visual grading. [3]

Procurement Impact: If your specs and receiving controls don’t align to these structural realities, you will experience avoidable variance: yield loss in formulation, line handling issues, and higher claim frequency.

(Analyzed at: Apr, 2026)

Treat “campaign capacity + aseptic release” as your first commercial lever, not an afterthought: lock a primary supplier early for base volume, but contractually reserve 20–30% swing volume with a pre-qualified alternate in a different origin/route.

This works because the market remains prone to sharp paste price moves and inventory-driven repricing—major processor disclosures note paste pricing declined after peaking in 2023, underscoring how quickly the market can turn. [4]

What’s at stake is typically not a 1–2% unit-price tweak; it’s the avoidable premium from last-minute cover buys and quality downgrades when a single campaign or a single aseptic lot fails—often landing in the mid-single digits of effective landed cost over a year for teams that run tight inventories.