Tomato paste looks like a simple commodity until you have to cover a short-ship in peak production months. This guide translates the market’s real mechanics—seasonality, processing capacity, and packaging/format constraints—into practical sourcing moves: how to time negotiations, structure contracts, and build alternates that can actually run.

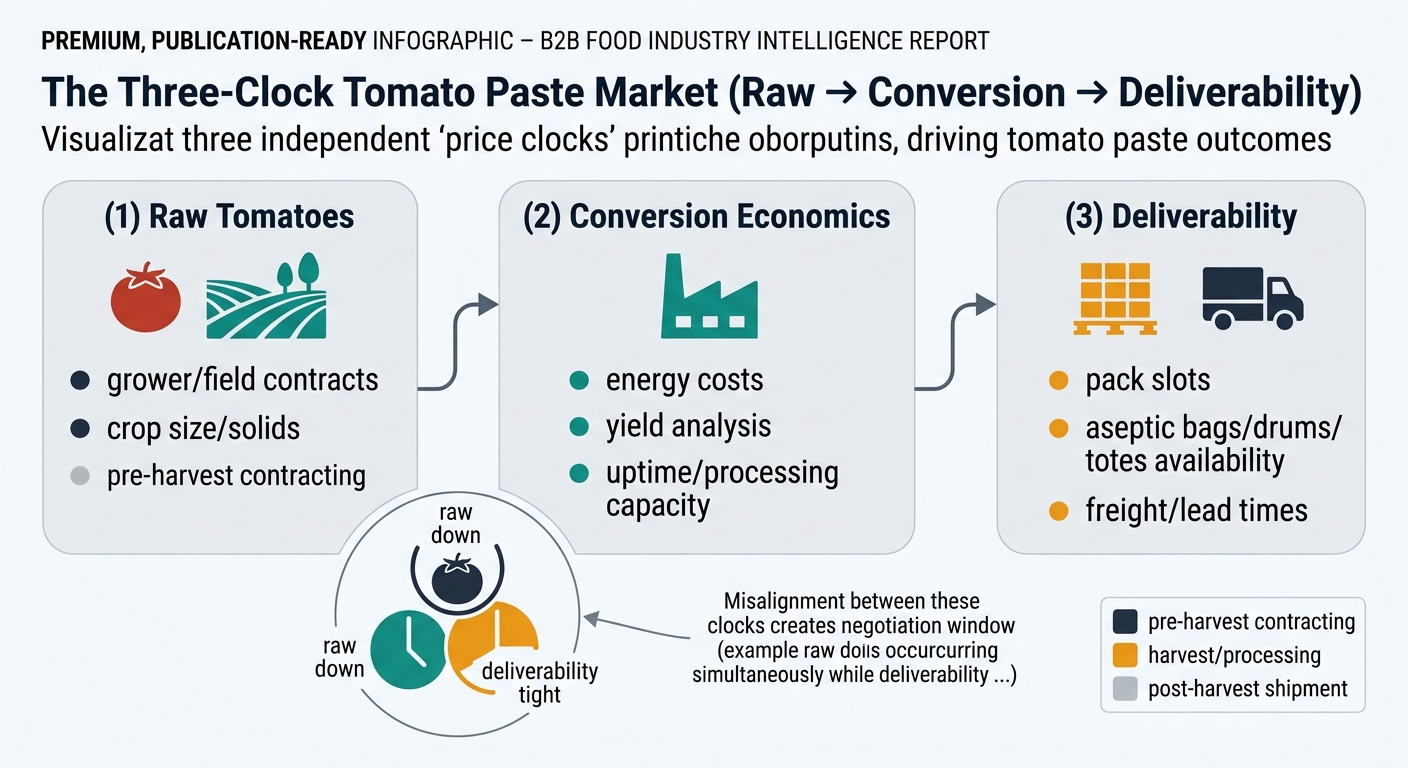

Tomato paste is one of the clearest “lag markets” in food ingredients—right up until a tight-packaging or tight-capacity moment breaks the lag and spot prices gap out.

Quick win: In your next supplier call, ask one question that forces the real constraint into the open: “For my delivery months, what is the limiting factor—tomato solids, evaporator uptime, aseptic bag supply, drum availability, or shipping capacity?” The answer tells you whether to negotiate on price, terms, or allocation protection.

Quick win: Add one governance item to your QBR agenda: “Allocation readiness.” Require the supplier to state (in writing) the order of precedence they use in constrained supply (contracted volume, payment terms, historical lift, strategic accounts). You’re not asking them to confess favoritism—you’re forcing clarity.

Quick win: Reframe your KPI for the category: track “% of volume with allocation protection” and “% of volume with a defined reset mechanism.” Those two metrics correlate strongly with fewer surprises.

Quick win: For each scenario, write a one-page “decision record” template: what changed, what you’re optimizing (cost vs continuity), and what trade-offs you accepted. This prevents reactive, undocumented exceptions.

Quick win: Pick one other category and add a single tomato-style control: “allocation clause + optional volume.” It’s usually the fastest governance upgrade.

Quick win: If you can’t explain last quarter’s paste price change in three lines (raw vs conversion vs deliverability), you’re negotiating blind.

Use the current “lag window” to renegotiate structure, not just price: lock your base volume with explicit allocation rules, then keep a smaller tranche on a shorter reset that forces transparency on packaging and conversion drivers. The window exists because raw tomato signals can soften (e.g., California’s $109/ton 2025 grower base price vs $112.50/ton in 2024) while deliverable paste remains sticky when pack slots and packaging are the real constraint. Teams that did this in prior tight cycles didn’t magically beat the market—they simply avoided the variance and emergency spot buys that hit buyers who waited for “proof” after the market had already repriced.

(Analyzed at: Apr, 2026)

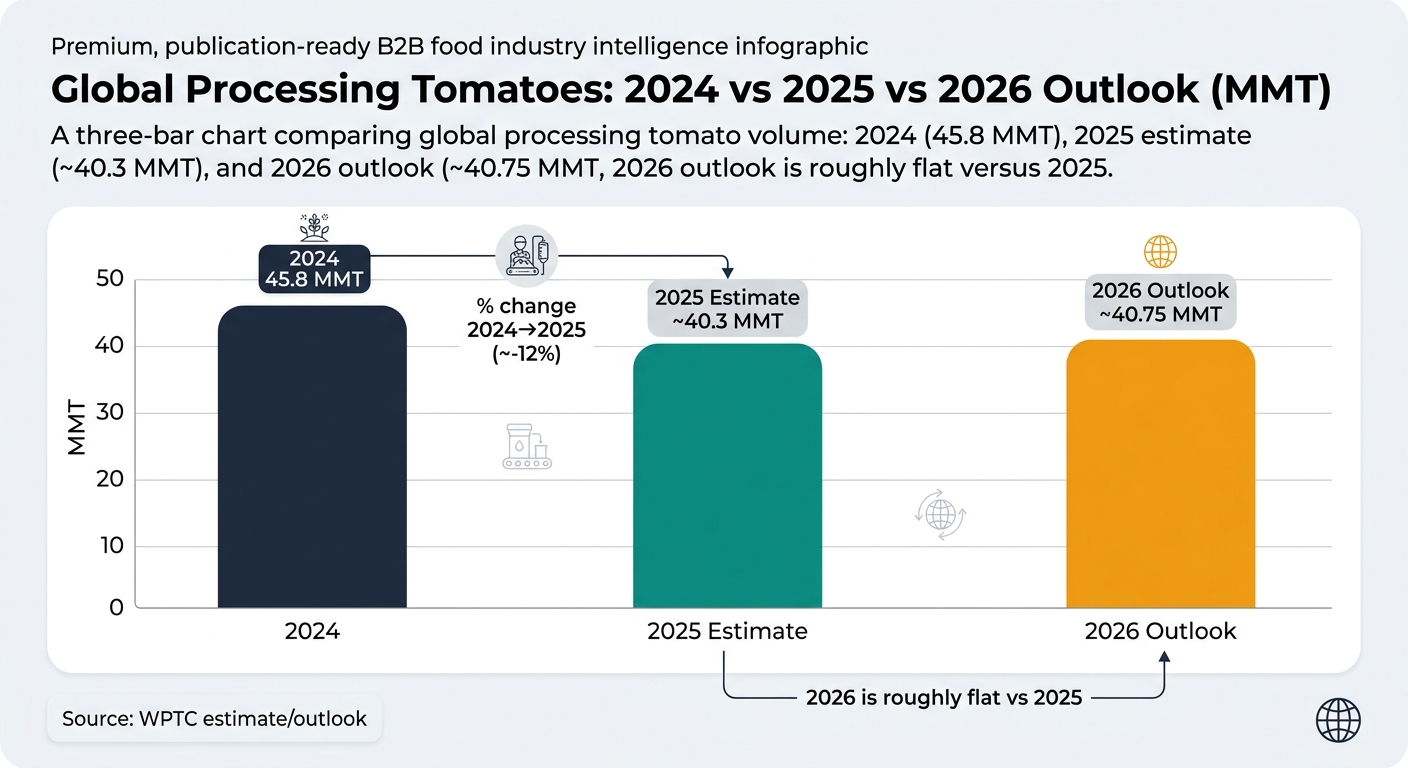

With WPTC projecting 2026 global processing volumes roughly flat versus 2025 (after the sharp 2025 drop versus 2024), the most practical edge right now isn’t trying to “call the bottom” on $/MT—it’s preventing a deliverability surprise when pack slots, aseptic packaging, or freight becomes the binding constraint. In your next renewal, lock 70–80% as protected base volume with explicit allocation mechanics, and keep 20–30% as an indexed/reset tranche tied to objective inputs (packaging + energy + freight) so you can reprice without reopening the whole contract. If you wait until allocation language shows up in offers, you typically end up paying for continuity through spot premiums and expediting—often a mid-single-digit landed-cost hit that finance will treat as avoidable variance, not “market reality.”