This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Sunflower oil is often treated like a “simple” edible oil line item—until a corridor disruption, a winterization miss, or a high‑oleic availability squeeze turns it into an allocation problem. This guide translates sunflower-oil supply chain realities into procurement actions: how to structure specs, lanes, contracts, and alternate suppliers so you reduce variance without increasing stockout risk.

Analyzed at: Mar, 2026

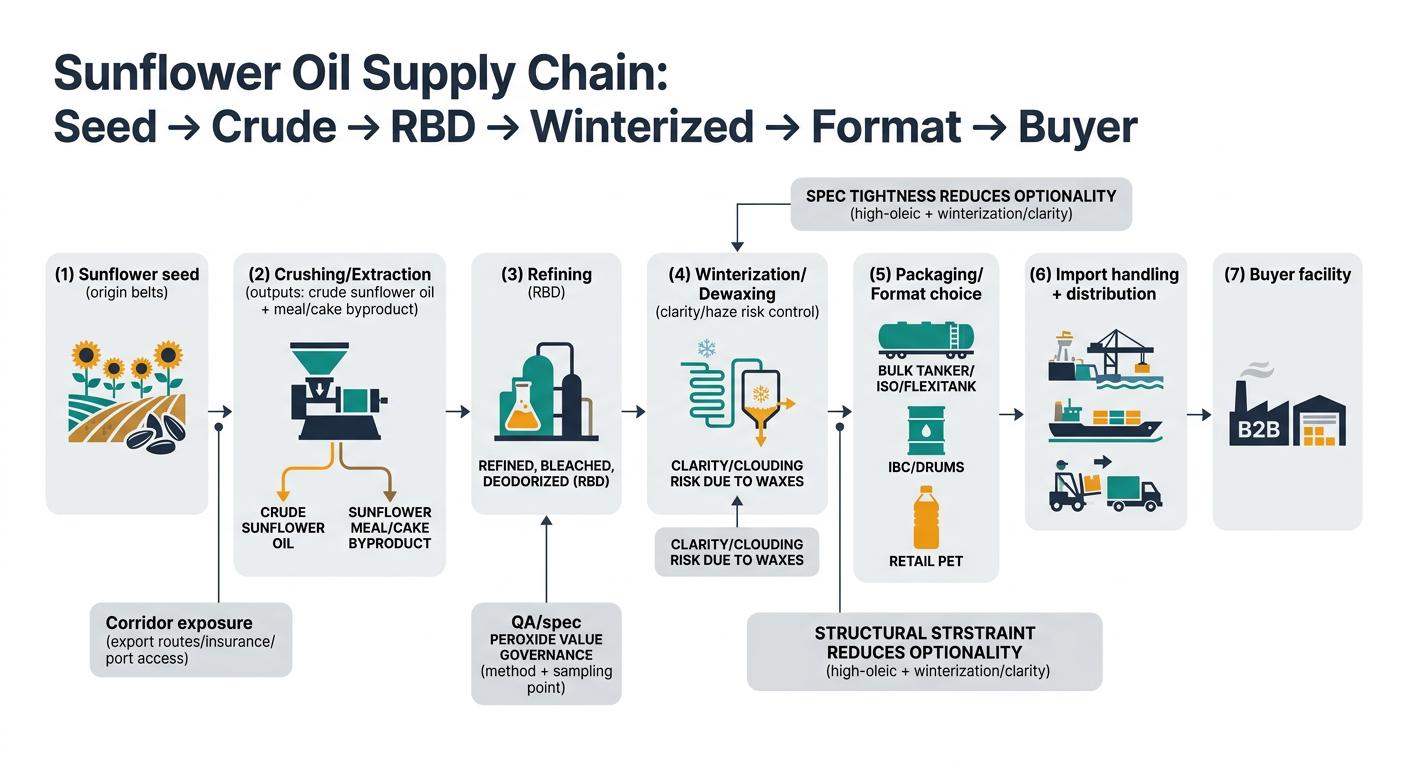

Sunflower oil looks like a simple ingredient, but procurement outcomes are decided by where you enter the chain (seed vs crude vs refined), what spec you lock (standard vs high‑oleic; winterized/dewaxed), and how you move it (bulk vs packed).

Below is the procurement-relevant view: what cost drivers dominate each node, what changes quickly, and what you can influence.

Key insight: In sunflower oil, seed is the biggest cost lever—and it’s seasonal and regionally concentrated. A bad crop (yield + oil content) tightens the whole system.

Key insight: Sunflower is a crush-margin commodity: crushers balance the value of oil + meal against seed cost. When meal demand changes, it can subsidize or penalize oil pricing.

Supplier quotes can diverge because each crusher has different:

Key insight: Refining is not “just a service.” It adds yield loss + energy/chemicals + QA, and winterization is often the hidden constraint for clear retail specs.

A “cheaper” refined offer may be cheaper because the supplier is:

Key insight: Packaging is where cost per ton can jump and where spec governance becomes real (COA discipline, traceability, contamination control).

Key insight: For sunflower oil, logistics is not a rounding error. Freight, insurance, demurrage, and lane disruption can swing landed cost quickly—especially for concentrated export corridors.

Key insight: Downstream margins don’t just add cost—they shape how fast price moves to you. Retail-heavy channels often lag market moves because of price-setting cadence and inventory.

Assumption: “Final landed cost” refers to delivered-to-buyer facility cost (not retail shelf price). Ratios vary by origin, season, packaging, Incoterms, and market tightness.

| Supply Chain Node | Cost Ratio (% of Final Landed Cost) | Notes |

|---|---|---|

| Seed (farm + local delivery embedded) | 62% | Dominant driver; seasonal and origin-sensitive |

| Crushing / extraction margin | 10% | Includes plant utilization + working capital |

| Secondary processing | 0% | Not refined |

| Packaging & QA | 3% | Basic QA + bulk handling |

| Logistics & trade | 18% | Inland + ocean + insurance/demurrage |

| Supplier/merchant margin | 7% | Varies with tightness and counterparty risk |

| Supply Chain Node | Cost Ratio (% of Final Landed Cost) | Notes |

|---|---|---|

| Seed (embedded) | 55% | Still the anchor |

| Crushing / extraction margin | 9% | |

| Refining + (often) winterization | 10% | Energy/chemicals + yield loss + filtration |

| Packaging & QA | 4% | Higher QA + release discipline |

| Logistics & trade | 16% | |

| Supplier/merchant margin | 6% |

| Supply Chain Node | Cost Ratio (% of Final Landed Cost) | Notes |

|---|---|---|

| High‑oleic seed premium (embedded) | 58% | Premium driven by identity preservation + limited acreage |

| Crushing / extraction margin | 9% | |

| Refining + winterization | 10% | Similar process cost but tighter QA |

| Packaging & QA | 5% | Higher spec/traceability burden |

| Logistics & trade | 14% | |

| Supplier/merchant margin | 4% | Often tighter if under longer programs |

| Supply Chain Node | Cost Ratio (% of Final Landed Cost) | Notes |

|---|---|---|

| Seed (embedded) | 48% | |

| Crushing / extraction margin | 8% | |

| Refining + winterization | 9% | |

| Packaging & QA | 14% | Packaging materials + handling + QA |

| Logistics & trade | 16% | More handling steps |

| Supplier/merchant margin | 5% |

If you source sunflower oil globally, two structural constraints dominate outcomes:

Procurement takeaway: Your true risk is not just price volatility—it’s supplier optionality collapse when the market tightens.

Procurement teams often expect sunflower oil to behave like a single transparent index. In practice, you’re buying a stack of spreads:

Procurement takeaway: A supplier “following the market” may still be overcharging if their basis/spreads are out of line versus peers with similar lanes and specs.

These are common failure modes when a team is strong in procurement but newer to sunflower oil specifics:

Below is how sourcing teams use intelligence outputs to change procurement actions—without pretending intelligence “guarantees” supply or price.

Category reality: Sunflower oil volatility is driven by seed supply shocks, corridor risk, and substitution dynamics in the wider veg-oil complex.

More governance complexity, less variance and fewer emergency buys.

Slightly higher qualification workload now, materially lower allocation risk later.

Broader supplier pool vs tighter product uniformity.

Sunflower oil is a clean example of a broader procurement truth: price is a stack of spreads, and risk sits where optionality collapses. The same intelligence-driven approach applies to other categories many procurement teams manage:

Procurement takeaway: once your team learns to manage sunflower oil with driver decomposition + supplier optionality + governance thresholds, you can transfer the same muscle to other volatile food inputs.

Sunflower oil makes a strong internal case for intelligence-led sourcing because:

Bottom line: Better sunflower oil procurement is less about predicting price and more about building optionality, normalized comparisons, and trigger-based decisions before the market forces your hand.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.