This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Spinach powder is often treated like a simple dehydrated commodity, but procurement outcomes are usually decided upstream (crop routing, yield, and dehydration capacity) and downstream (micro controls, documentation, and spec governance). This guide is written for procurement and sourcing managers who are strong in general sourcing but newer to spinach powder: it focuses on the decisions you need to make (award, dual-source, contract structure, spec trade-offs, and buffers), the realities that drive cost and risk, and what “good” looks like in governance with QA, Ops, and Finance.

(Analyzed at: Apr, 2026)

Spinach powder looks like a simple commodity, but procurement outcomes are usually determined upstream—by how fresh spinach is routed (fresh market vs. processing), how the plant manages microbial risk, and which drying method is used.

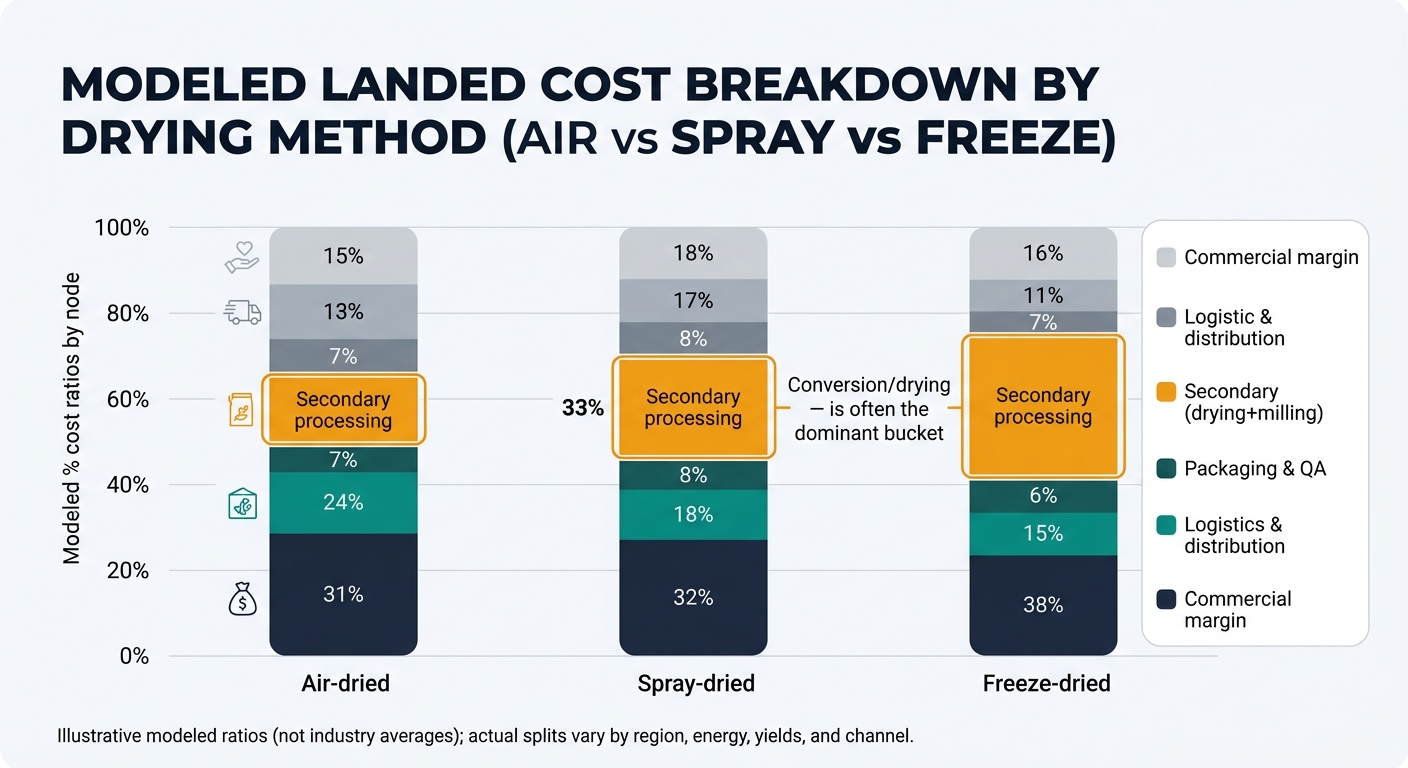

Below is an analyst view of where cost concentrates and where suppliers typically protect margin. This is the section procurement managers use to decide: spot vs contract, dual‑source strategy, and which specs to tighten/relax.

Key insight: Fresh spinach economics are dominated by yield volatility + rejection risk + competition with fresh-market demand.

Key insight: This is where spinach powder suppliers either build trust—or create hidden risk. Washing, dewatering, and sanitation are cost-heavy and quality-critical.

Key insight: Drying is often the dominant industrial cost bucket because it is energy-intensive and can be capacity-constrained at peak season.

Key insight: For many buyers, the “price” is not the problem—the documentation and defensibility is.

Key insight: Spinach powder ships ambient, but humidity exposure can cause caking, color degradation, and claims.

Key insight: The downstream application determines which spec parameters are truly “must-have.”

Values below are modeled ratios of final delivered cost (not quotes). They help procurement teams identify where negotiation leverage exists (and where it doesn’t).

Important validation note: These ratios are plausible for decision-making discussion, but they are not “industry averages.” Actual splits swing materially by region, energy prices, plant technology, yields, and whether you are buying manufacturer-direct vs trader. Use them as a framework to ask better questions, not as a benchmark to enforce pricing.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw material (fresh spinach) | 28% | Yield/rejection risk drives volatility |

| Primary processing | 14% | Wash/dewater, wastewater, labor |

| Secondary processing | 30% | Drying energy + milling/sieving |

| Packaging & QA | 10% | Testing + COA + packaging |

| Logistics & distribution | 8% | Freight + warehousing |

| Commercial margin (processor/trader) | 10% | Higher if trader-heavy chain |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw material (fresh spinach) | 24% | Still sensitive to farm supply |

| Primary processing | 16% | More emphasis on slurry prep and control |

| Secondary processing | 34% | Spray drying energy + tighter controls |

| Packaging & QA | 11% | Often tighter spec governance |

| Logistics & distribution | 7% | Similar, but higher claims sensitivity |

| Commercial margin (processor/trader) | 8% | Lower if manufacturer-direct |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw material (fresh spinach) | 18% | Premium is mostly processing |

| Primary processing | 14% | Higher sorting/selectivity common |

| Secondary processing | 44% | Freeze-drying capex/opex dominates |

| Packaging & QA | 12% | High-barrier packaging more common |

| Logistics & distribution | 6% | Similar lanes, higher insurance/handling |

| Commercial margin (processor/trader) | 6% | Often manufacturer-direct for premium |

Procurement teams often treat spinach powder as a single spec item. In reality, it’s a family of products with different economics and risk.

Practical takeaway: Before negotiating price, lock the segmentation: “Which drying method + which mesh + which micro/residue limits + what documentation set?” Otherwise you’ll compare non-equivalents.

Spinach powder pricing often surprises procurement teams because the biggest cost lever is not always spinach itself.

Even though powders don’t support pathogen growth, Salmonella can survive for long periods in low-moisture foods and is a recognized industry challenge. This drives: [1]

These are the recurring failure modes when experienced procurement managers enter spinach powder without category-specific context.

This is not about “more data.” It’s about changing which decisions you can safely make earlier.

Better contracting posture comes from separating cost drivers:

Start qualification when risk signals appear (not after a missed shipment):

What this can and cannot do: intelligence helps you prioritize and time decisions; it does not replace audits, validated lethality steps, or lab testing.

These are the use cases that map to measurable outcomes (budget stability, continuity, governance).

If you source spinach powder, you likely also touch categories where the same intelligence patterns apply:

The transferable lesson: specs + process controls + capacity constraints usually explain more procurement outcomes than “country price averages.”

Spinach powder is a strong example because it forces cross-functional decision-making under uncertainty:

When teams apply intelligence correctly, the measurable shift is not “cheaper powder.” It’s:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.