This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Soybean oil sourcing rarely fails because teams “didn’t negotiate hard enough.” It fails when procurement decisions are made using a single headline price and a single incumbent quote—while the real constraints sit in crush economics (meal vs oil), refining/packaging capacity, and lane-specific bulk logistics. This guide translates those realities into procurement actions: how to structure contracts, how to benchmark quotes correctly, and how to pre-qualify alternatives before the market turns allocation-driven.

(Analyzed at: Mar, 2026)

Soybean oil looks like a simple edible ingredient, but procurement outcomes are driven by a co-product industrial system (crush + refining + bulk logistics) with several pinch points.

Key insight: In soybean oil, the biggest cost lever is not refining or packaging—it’s the bean-to-oil conversion economics (crush margins) plus the buyer’s lane/spec constraints that determine who can physically supply you.

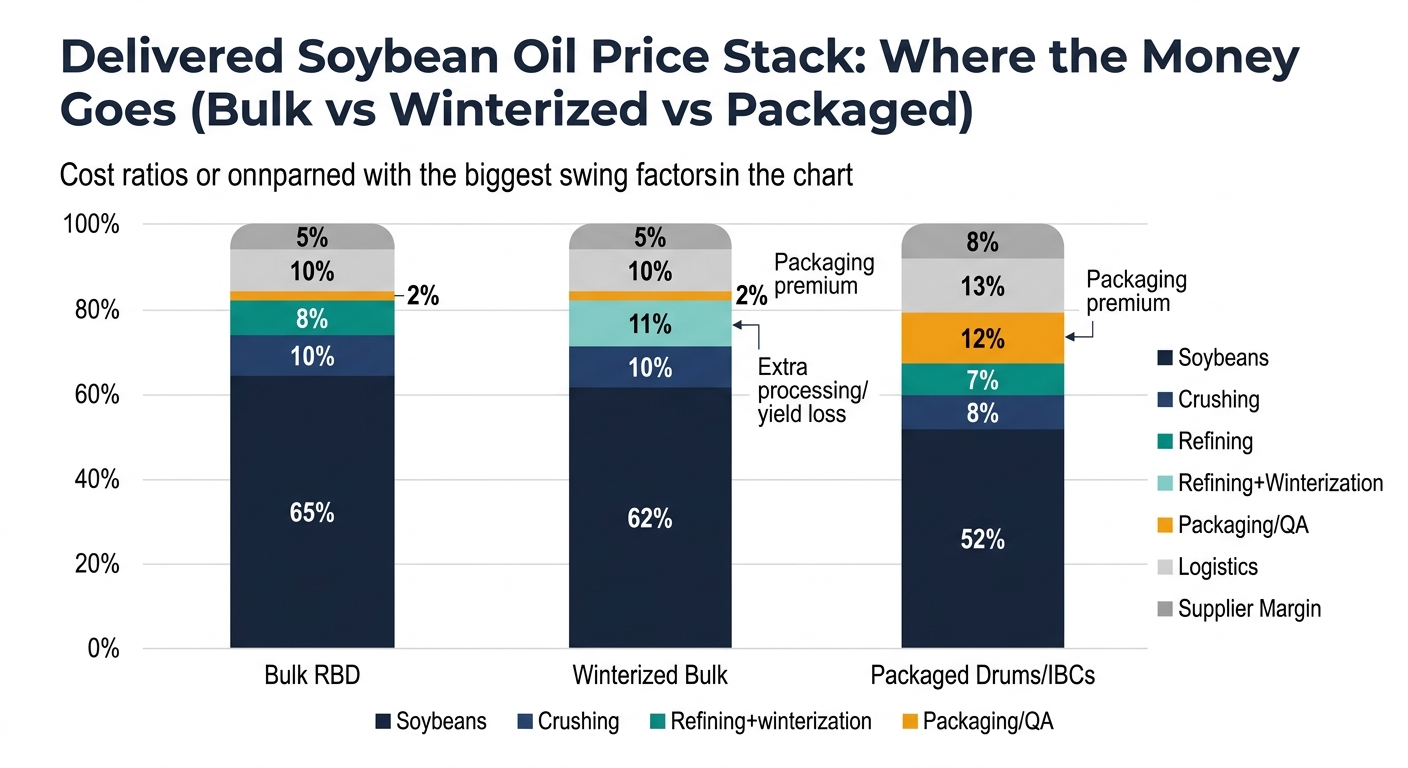

Modeled ratios to show where cost concentrates by product form. Actuals vary by region, contract terms, and tightness.

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Soybeans (raw material) | 65% | Futures + basis + yield risk |

| Crushing/extraction | 10% | Crush margin, energy, utilization |

| Refining (RBD) | 8% | Energy, yield loss, refining aids |

| Packaging & QA (bulk loading) | 2% | CoA/testing, loading controls |

| Logistics & distribution | 10% | Truck/rail, tank storage, demurrage |

| Distributor/supplier margin | 5% | Allocation behavior, service level |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Soybeans (raw material) | 62% | Same as above |

| Crushing/extraction | 10% | Same as above |

| Refining + winterization | 11% | Extra processing, yield loss, scheduling |

| Packaging & QA (bulk loading) | 2% | Extra QC parameters |

| Logistics & distribution | 10% | Cold-weather handling, heating |

| Distributor/supplier margin | 5% | Specialty availability |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Soybeans (raw material) | 52% | Bean price level |

| Crushing/extraction | 8% | Crush economics |

| Refining (RBD) | 7% | Energy, yield |

| Packaging & QA (drums/IBCs) | 12% | Packaging availability, labor |

| Logistics & distribution | 13% | LTL vs FTL, warehousing |

| Distributor/supplier margin | 8% | Service, inventory position |

Important structural fact: Soybean oil supply is structurally tied to (1) soymeal demand (animal feed) and (2) biofuel policy-driven demand (renewable diesel/biodiesel).

What this means in practice:

The critical insight: In soybean oil, price is not one number. Your delivered cost is a stack of spreads that can decouple:

Your negotiation leverage improves when you can separate:

This doesn’t predict the market; it improves decision timing and options.

Decision it changes: spot vs term, and where to use index-linking (where feasible) vs fixed pricing.

Decision it changes: supplier tiering (primary/secondary/tertiary) by spec + lane + packaging.

The same intelligence logic applies when the commodity is:

Common thread: the “headline market price” is only one layer; procurement performance depends on understanding the conversion bottlenecks, specifications, and logistics that turn markets into delivered supply.

Soybean oil is a powerful example because it combines:

For procurement leadership, that means intelligence is not “nice-to-have.” It is what turns soybean oil from a reactive, disruption-priced category into one where you can:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.