This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

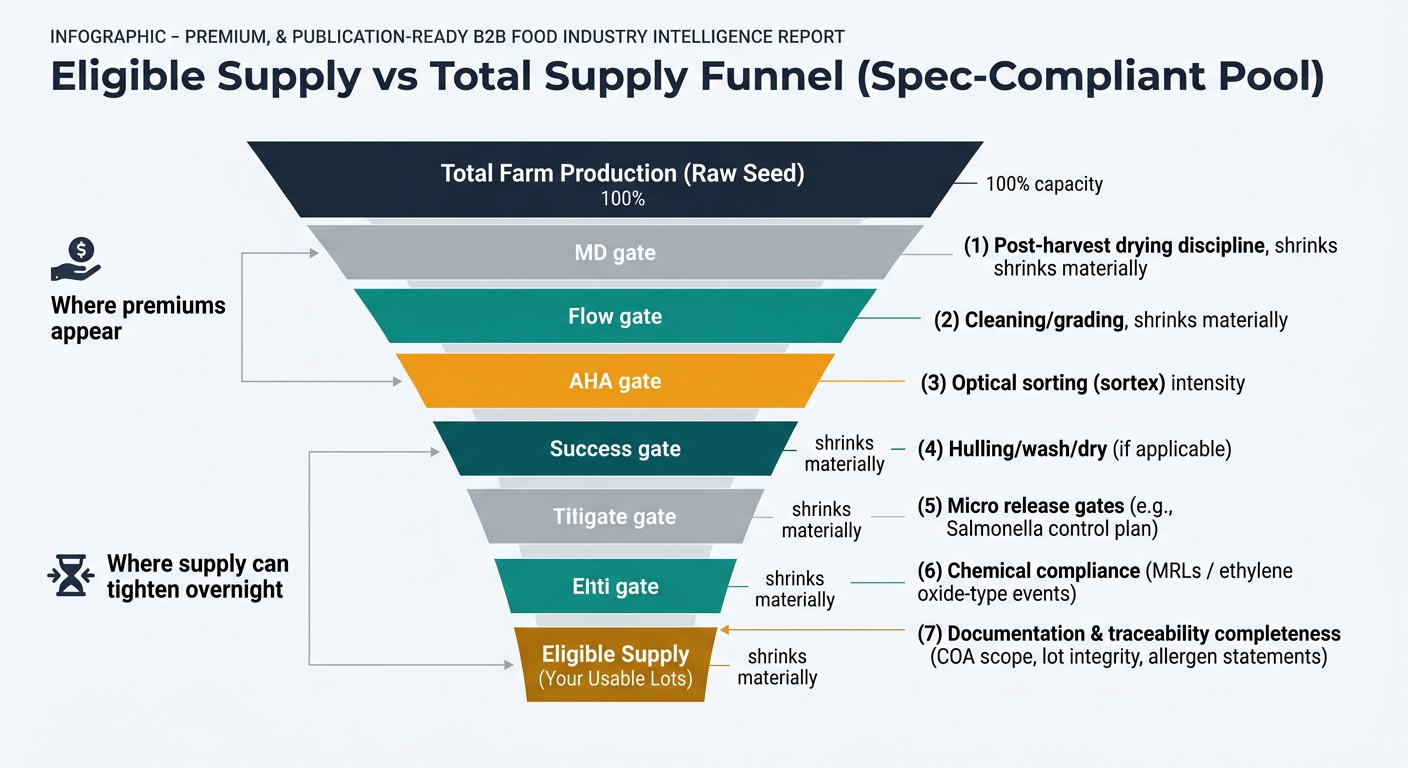

This guide is written for procurement and sourcing managers who are strong in buying fundamentals but newer to sesame. The core message is simple: sesame is not “one commodity.” Your outcomes (price, continuity, and audit readiness) are determined by the eligible supply pool—lots that meet your exact spec, food safety plan, and documentation gates—not by total farm production. Use this playbook to translate market signals (crop, logistics, compliance) into concrete sourcing actions: tighter RFQs, better benchmarks, and pre-qualified alternatives.

(Analyzed at: Mar, 2026)

Sesame looks like a simple “seed” line item, but procurement outcomes are driven by where value is created (cleaning, sorting, hulling) and where risk is introduced (post-harvest drying, storage, cross-contamination, export corridors).

Below is the practical procurement lens: at each node, what cost drivers create price moves—and what that implies for RFQs, supplier selection, and contract structure.

Key insight: A large portion of downstream claims (odor, moisture, mold risk, foreign matter) are “baked in” before the exporter ever touches the seed.

Key insight: Cleaning/sortex is the first major step where yield loss becomes cost (removing stones, dust, broken seed) and where suppliers differentiate.

Key insight: Hulling and roasting aren’t just “processing fees.” They change yield, shelf stability, and microbial risk profile—and they concentrate supplier power when capacity is limited.

Key insight: A single documentation gap (traceability, allergen statement, MRL test scope) can convert a shipment into inventory-on-hold.

Key insight: For several origins, inland trucking to port, border procedures, and port dwell time create bigger lead-time variance than sea freight.

Key insight: Importers earn margin for holding inventory, blending lots, and absorbing compliance risk—especially when buyers want short lead times.

Modeled to show where cost concentrates by product form. Actual ratios vary by origin, crop year, spec strictness, and whether you buy direct from origin or via an importer.

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Farm & aggregation | 55% | harvest campaign price, local demand |

| Cleaning / grading / sortex | 12% | yield loss, sortex intensity |

| Secondary processing | 0% | N/A |

| Packaging & QA | 6% | testing scope, lot segregation |

| Logistics (inland + ocean + port) | 15% | inland bottlenecks, dwell time |

| Importer/wholesale margin | 12% | inventory coverage, service level |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Farm & aggregation | 40% | raw seed cost baseline |

| Cleaning / grading / sortex | 12% | pre-hull cleanliness needed |

| Hulling + wash + dry | 18% | yield loss, energy, rework |

| Packaging & QA | 8% | micro plan, COA requirements |

| Logistics (inland + ocean + port) | 12% | moisture protection, timing |

| Importer/wholesale margin | 10% | short lead-time expectations |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Farm & aggregation | 28% | seed input cost |

| Cleaning / grading / sortex | 8% | seed eligibility |

| Roast + grind + formulation | 26% | energy, yield, throughput |

| Packaging & QA | 12% | jars/drums, micro release |

| Logistics (inland + ocean + port) | 10% | weight/pack format |

| Importer/wholesale margin | 16% | brand/quality assurance, claims |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Farm & aggregation | 25% | seed input |

| Cleaning / grading | 5% | basic cleanliness |

| Crushing + refining | 35% | energy, refining loss, capacity |

| Packaging & QA | 10% | bottles/drums, labeling |

| Logistics | 10% | weight, handling |

| Importer/wholesale margin | 15% | inventory + channel margin |

Procurement teams often expect sesame to behave like a single commodity curve. In practice, sesame behaves like two coupled markets:

The spread between A and B widens when any of these tighten:

This is the playbook that most reliably improves resilience for sesame without inflating cost: Pre-qualify alternatives before disruption hits.

Sesame is a clean example of a broader procurement truth: the tightest constraint is often “eligible supply,” not total supply.

The procurement muscle you build in sesame—spec passports, bench depth, trigger-based actions, and governance cadence—transfers directly.

Sesame is a high-signal category because:

If you can run sesame like a portfolio (cost + continuity + compliance), you can usually run the rest of your ingredient basket with fewer surprises.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.