This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Seed potatoes look like “just another ag input” until you try to switch suppliers late, move lots across borders, or plant into a tight window. This guide translates seed-potato category realities (certification, lot identity, storage biology, and timing) into procurement decisions you can govern: how to compare suppliers like-for-like, how to avoid spec drift disguised as “market pricing,” and how to build optionality before allocation or disruption hits.

Analyzed at: Mar, 2026

Seed potato is not a commodity input in the way fertilizer or packaging is. It is regulated planting stock with:

Procurement reality: your decision is rarely “who is cheapest?” It is:

Key insight: seed-potato cost accumulates at control points (health status, certification, storage, grading, documentation, cold chain). The “seed price” is often a proxy for risk and constraints, not just production cost.

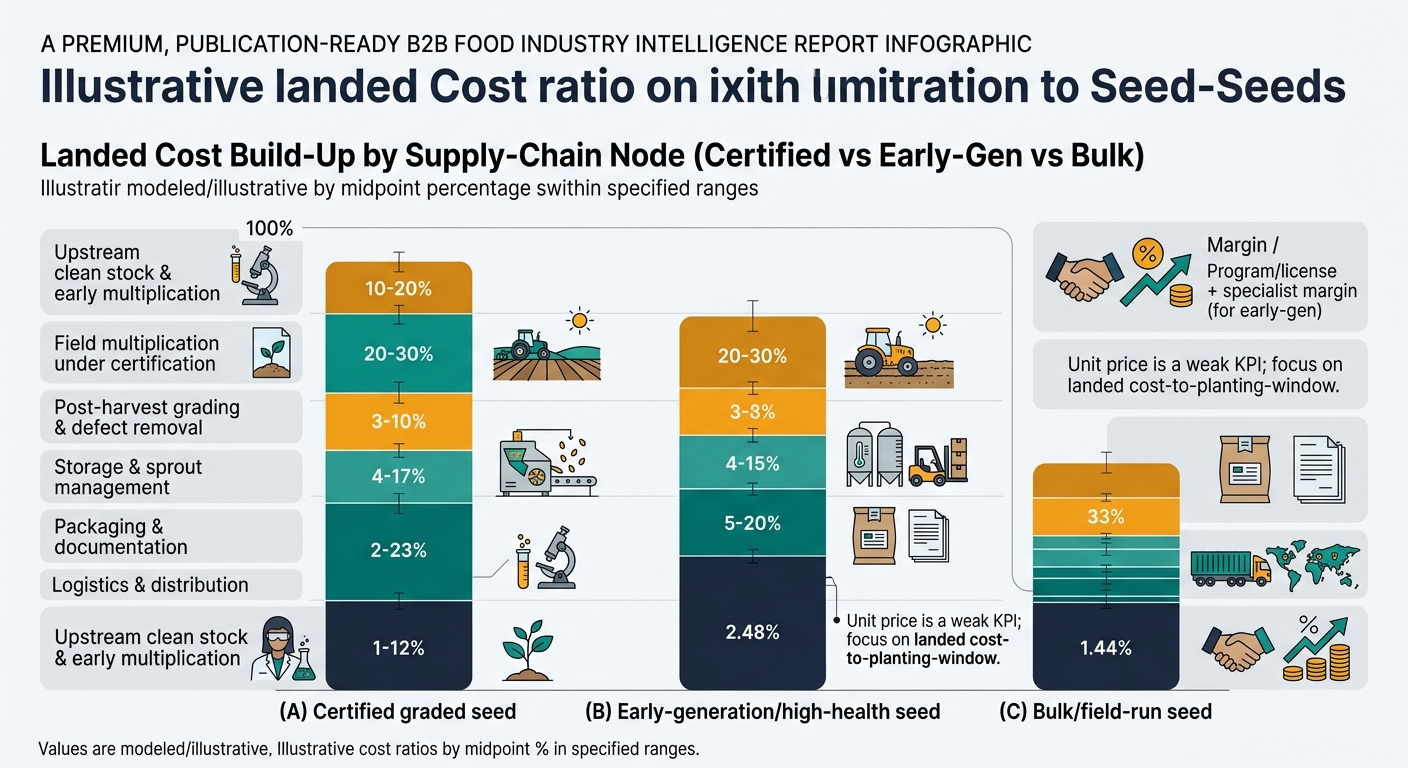

Below is a practical, procurement-friendly breakdown by supply-chain node.

These are modeled ranges to show where cost concentrates by product form; actual ratios vary by origin, variety, class, season tightness, and lane. The tables below are internally consistent (each sums to 100%) and intended for procurement scenario modeling—not as industry “averages.”

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Upstream clean stock & early multiplication | 8–15% | Variety access, early-gen scarcity |

| Field multiplication under certification | 30–45% | Crop outturn, downgrades, inspections |

| Post-harvest grading & defect removal | 10–18% | Size profile, rejects, throughput |

| Storage & sprout management | 10–18% | Energy, storage losses, dormancy control |

| Packaging & documentation | 4–8% | Labeling, testing, traceability |

| Logistics & distribution | 10–20% | Reefer need, distance, border timing |

| Packer/exporter/importer margin | 8–15% | Allocation power, service reliability |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Upstream clean stock & early multiplication | 15–30% | Lab/greenhouse intensity, discard rates |

| Field multiplication under certification | 25–40% | Tight tolerances, inspection outcomes |

| Post-harvest grading & defect removal | 8–15% | Outturn + defect pressure |

| Storage & sprout management | 8–15% | Longer holding periods, vigor risk |

| Packaging & documentation | 5–10% | Higher documentation burden |

| Logistics & distribution | 8–18% | Lane complexity, inspection timing |

| Program/variety license + specialist margin | 10–20% | IP, scarcity, program reputation |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Upstream clean stock & early multiplication | 5–10% | Less embedded early-gen value |

| Field multiplication under certification | 35–55% | Yield + health status |

| Post-harvest grading & defect removal | 3–8% | Minimal grading intensity |

| Storage & sprout management | 8–15% | Storage losses dominate |

| Packaging & documentation | 2–5% | Lower packaging cost |

| Logistics & distribution | 12–25% | Bulk handling, lane distance |

| Margin | 5–12% | Service level lower, risk higher |

Key insight: seed-potato supply tightness is often locked in seasons ahead because:

Procurement implication: optional capacity must be built before the shock, not after.

Key insight: seed and ware potatoes share biology, but their economics diverge because seed price is driven by:

Failure mode: procurement benchmarks against “potato market price” and then treats seed quotes as inflated—missing that the seed market is pricing risk, compliance, and timing.

Key insight: the service changes decisions when it makes spec-comparable, risk-ranked options visible early enough to act.

What procurement can do differently:

Decision impact: management gets a defensible rationale for paying a premium when the premium buys lower probability of a missed planting window.

What procurement can do differently:

Decision impact: fewer “panic buys,” fewer emergency freight premiums, and fewer internal escalations.

Key insight: seed potatoes are an extreme example of a broader procurement pattern— biological/regulated inputs where “equivalence” is hard and timing is everything.

Comparable categories where intelligence-based sourcing prevents expensive mistakes:

The transferable lesson: when the input is spec-sensitive + time-sensitive + compliance-sensitive, procurement needs a system that makes comparisons defensible and risks visible early.

Seed potatoes force clarity on what “good procurement” means:

In other words: seed-potato sourcing rewards teams that manage specs, time, and risk as first-class procurement variables—not afterthoughts.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.