This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Rice is often treated like a “simple staple,” but for inventory and warehouse-led buyers it behaves like a policy- and logistics-sensitive ingredient: lead times swing, specs are not always substitutable, and landed cost can move for reasons that don’t show up in the commodity headline.

This guide translates rice supply-chain realities into actions Purchase roles can actually take—reorder timing, safety stock, inbound scheduling, and alternate sourcing—while being clear about what market intelligence can and cannot infer.

Analyzed at: Mar, 2026

Rice looks like a “simple staple,” but the supply chain behaves more like a policy- and logistics-sensitive manufactured ingredient than a stable grain.

Key insight: In rice, farmgate paddy price is the anchor, but usable supply depends heavily on post-harvest handling speed (drying) and weather/policy shocks.

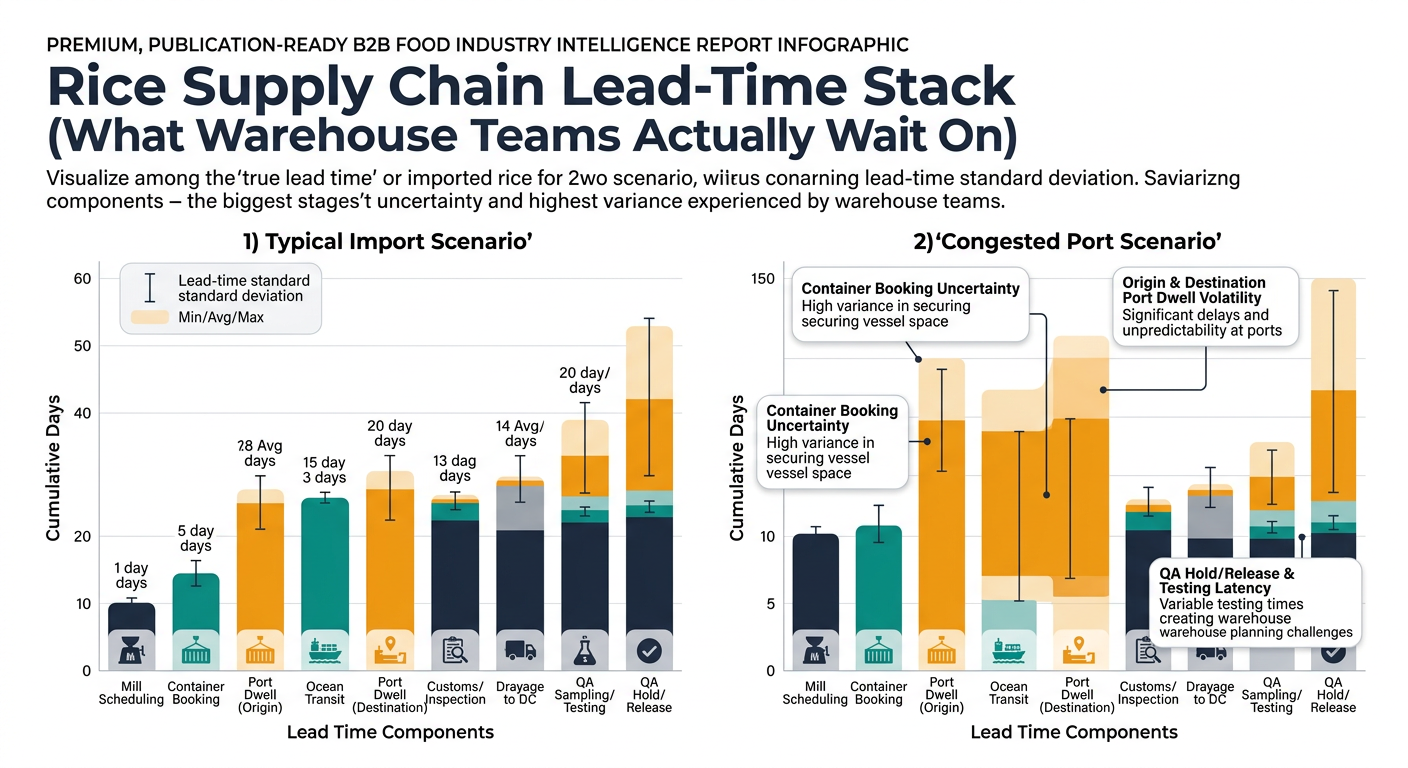

Key insight: Drying and storage are where quality loss becomes “hidden cost.” If moisture is not controlled, the warehouse later pays via rejects, downgrades, and infestation risk.

Key insight: Milling economics are yield economics. Your delivered spec (broken %, chalkiness, foreign matter, moisture) is not free—mills “pay” for it in sorting losses and lower outturn.

Key insight: Packaging format decisions create MOQ and handling constraints that directly affect reorder points and dock scheduling.

Key insight: Rice is frequently containerized; when container markets tighten, freight becomes a first-order cost driver and a lead-time variance driver.

Key insight: The tighter the end-customer spec (aroma, varietal purity, broken%, cooking performance), the fewer true alternates you have—so your inventory buffer requirement increases unless you dual-source.

These are illustrative ratios to show where costs tend to concentrate. Actual splits vary by origin, crop year, contract terms, packaging, and freight.

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most | Warehouse implication |

|---|---|---|---|

| Upstream (paddy) | 45% | farmgate + policy floors | price shifts can be fast in tight markets |

| Primary processing (dry/store) | 7% | drying energy, loss rates | poor handling shows up later as rejects |

| Secondary processing (milling/grading) | 12% | outturn, broken% spec | tighter spec = higher effective cost |

| Packaging & QA | 6% | bag/label, QA holds | longer “available” lead time |

| Logistics & distribution | 18% | ocean + port + inland | biggest landed-cost swing factor |

| Trading/wholesale margin | 12% | allocation power, financing | allocation risk in tight supply |

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most | Warehouse implication |

|---|---|---|---|

| Upstream (paddy) | 40% | paddy price | similar exposure as white rice |

| Primary processing (dry/store) | 7% | drying capacity | peak-season bottlenecks |

| Secondary processing (parboil + mill) | 18% | steam/energy, drying time | longer production lead time |

| Packaging & QA | 6% | bag/COA | QA holds still apply |

| Logistics & distribution | 17% | freight/port | same corridor risks |

| Trading/wholesale margin | 12% | allocation | supply can tighten if parboil capacity is constrained |

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most | Warehouse implication |

|---|---|---|---|

| Upstream (varietal paddy) | 50% | crop quality + varietal purity | fewer acceptable substitutes |

| Primary processing (dry/store) | 6% | quality preservation | higher downgrade risk |

| Secondary processing (milling/grading) | 12% | head rice recovery | tighter broken% drives cost |

| Packaging & QA | 8% | testing, traceability | longer release time likely |

| Logistics & distribution | 14% | freight | still meaningful but less dominant |

| Trading/wholesale margin | 10% | brand/grade premiums | allocation risk higher in short crop |

Structural fact: A meaningful share of globally traded rice is exposed to government export actions, and when a major exporter changes rules, the effect is immediate for importers.

Inventory buyers often expect: export benchmark down ⇒ my delivered cost down. In rice, the pass-through is frequently broken by four disconnects:

The goal is not “predict prices.” It’s to make replenishment and buffering decisions that survive volatility.

The same decision discipline applies wherever policy, yield, and logistics variance dominate outcomes:

In each case, intelligence is most valuable when it changes reorder timing, buffers, and supplier mix—not when it just describes the market.

Rice is a strong “proof category” because:

For Purchase roles managing inventory and warehouse stability, the win is straightforward to validate: fewer stockouts and expedites, smoother inbound flow, and more defensible buffer decisions—without pretending anyone can perfectly forecast the next shock.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.