This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Quail eggs can look like a “small, specialty” subcategory, but the buying dynamics are not small: supply is often fragmented, quality losses are highly nonlinear (breakage/yield), and the governance burden changes materially once you move from shell eggs into processed egg products. This guide translates those realities into procurement decisions—how to qualify suppliers, normalize quotes, set the right contract cadence, and run governance with metrics that actually predict cost and service outcomes.

(Analyzed at: Apr, 2026)

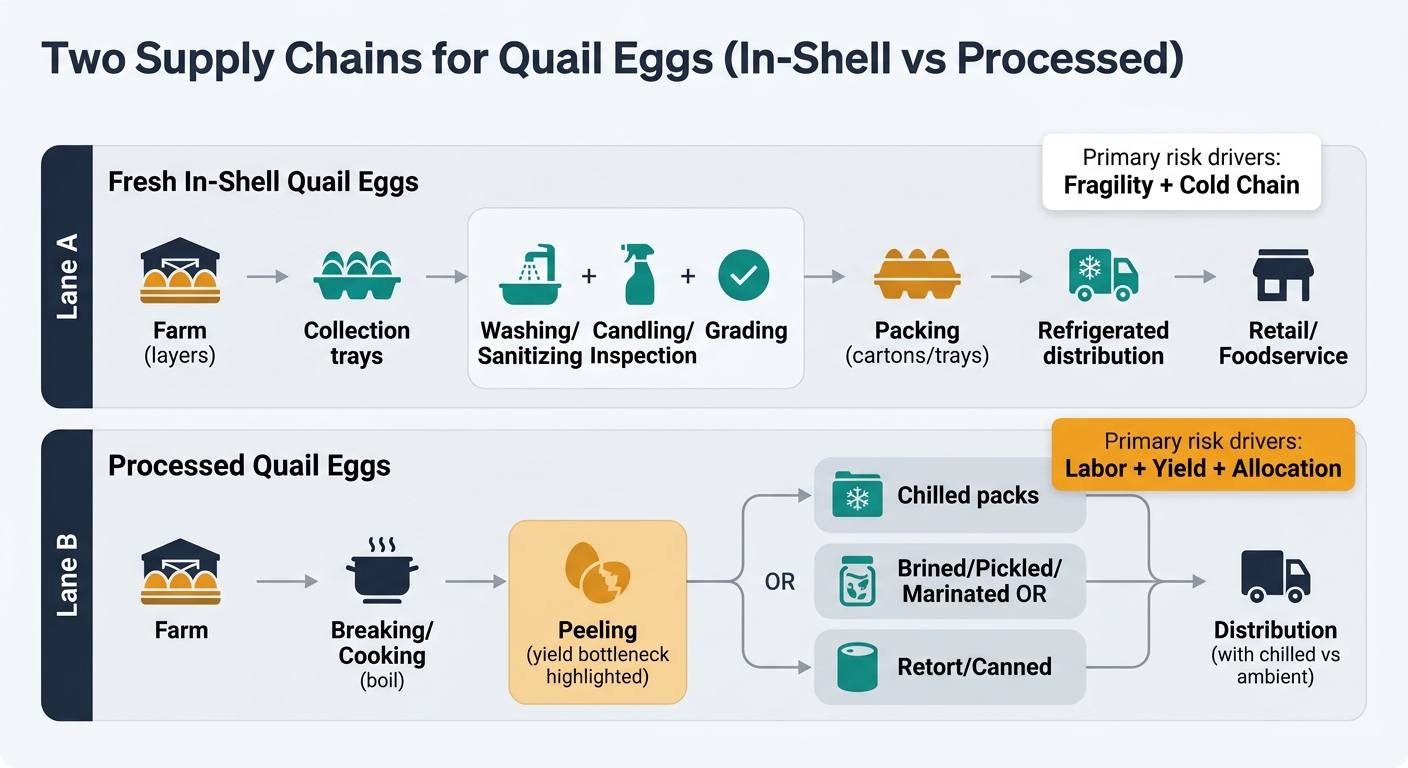

Quail eggs look like a simple commodity, but procurement outcomes are driven by two very different supply chains:

Fresh in-shell quail eggs (local/regional, fragile, cold-chain sensitive)

Processed quail eggs (more tradable, processing-bottlenecked)

Procurement implication: you are not buying “quail eggs.” You are buying a fragility profile (in-shell) or a processing-yield profile (peeled/value-added)—and each one has different cost drivers, risks, and governance controls.

In quail eggs, procurement teams often over-index on farmgate/unit price. But the major cost swings typically come from:

Below is a practical, procurement-oriented node-by-node view.

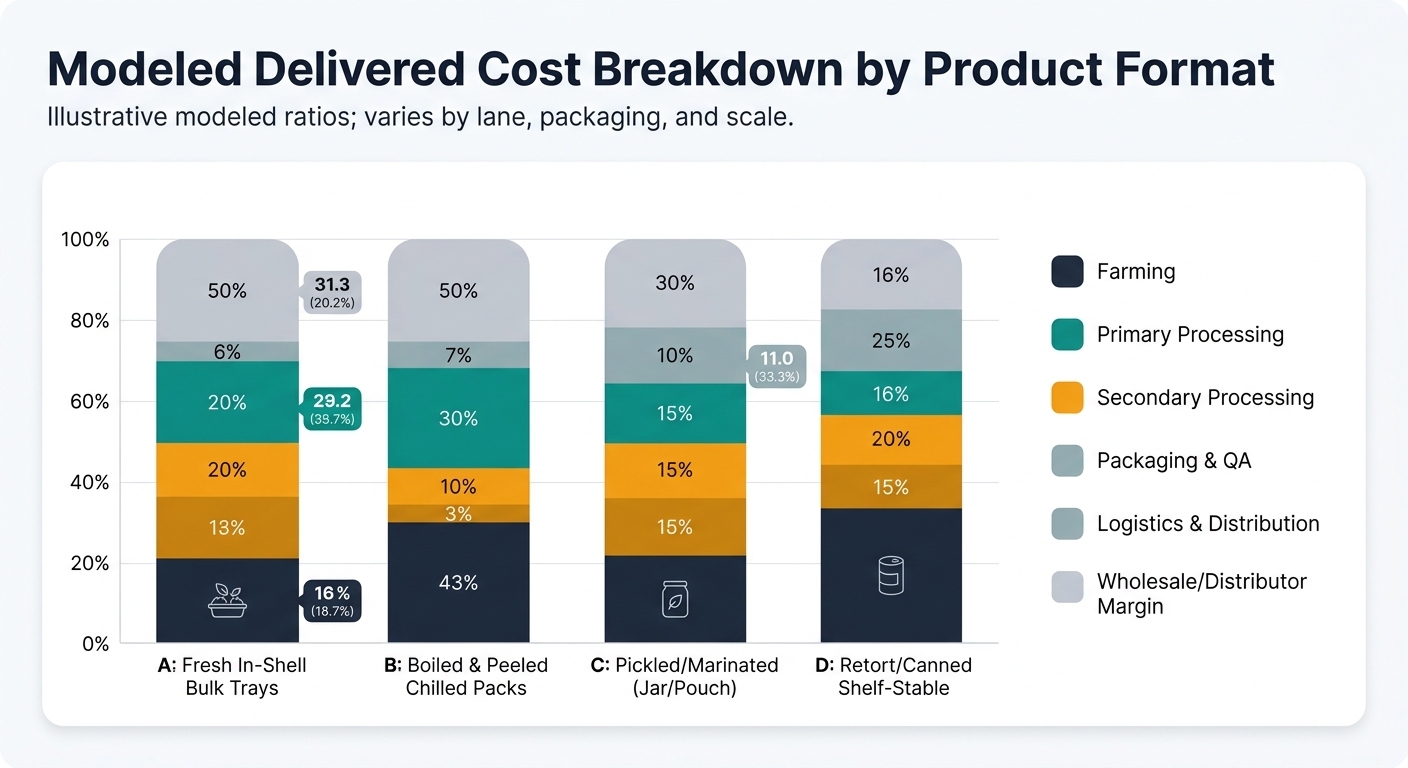

Values below are modeled % of final delivered cost to a mid-size U.S. buyer. Actual ratios vary by region, packaging, lane length, and supplier scale. Use these as a should-cost discussion scaffold, not as a pricing “truth.”

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Farming (egg production) | 45% | Feed + flock performance dominate. |

| Primary processing (wash/grade/pack) | 15% | Labor + grading yield + trays/cartons. |

| Secondary processing | 0% | N/A |

| Packaging & QA | 8% | Tray spec and inspection discipline reduce breakage. |

| Logistics & distribution | 17% | Refrigerated freight + damage/shrink is material. |

| Wholesale/distributor margin | 15% | Varies by channel concentration. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Farming (egg production) | 30% | Still important, but downstream dominates. |

| Primary processing | 10% | Pre-sort and routing to cook line. |

| Secondary processing (boil/peel/inspect) | 28% | Labor + yield loss is the swing factor. |

| Packaging & QA | 12% | Pack integrity + micro testing expectations. |

| Logistics & distribution | 10% | Chilled chain, shorter shelf-life. |

| Wholesale/distributor margin | 10% | Often negotiated via volume commitments. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Farming (egg production) | 22% | Raw egg share diluted by packaging and processing. |

| Primary processing | 8% | Sorting + pre-cook handling. |

| Secondary processing (cook + formulation + fill) | 20% | Ingredients + line efficiency. |

| Packaging & QA | 25% | Glass/metal/pouch + coding + QA. |

| Logistics & distribution | 10% | Ambient lowers freight volatility. |

| Wholesale/distributor margin | 15% | Brand and channel power matter. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Farming (egg production) | 18% | Lower share; processors capture more value. |

| Primary processing | 7% | Pre-processing and grading. |

| Secondary processing (retort/can) | 18% | Energy + process controls + throughput. |

| Packaging & QA | 32% | Can/jar + retort validation + QA overhead. |

| Logistics & distribution | 10% | Typically dry freight; longer lead times. |

| Wholesale/distributor margin | 15% | Long shelf-life supports inventory programs. |

Procurement teams often assume a linear relationship: farm price up → delivered price up.

In quail eggs, the relationship frequently breaks because:

Practical takeaway: treat quail eggs as a landed-cost system (unit + shrink + freight + compliance + service failure cost), not a unit-price line item.

This is not about “more data.” It’s about changing the specific procurement decisions that drive cost, continuity, and governance.

Quail eggs are a clean example of a broader procurement truth: unit price is rarely the largest lever once you include yield, logistics, and governance.

Similar patterns show up in:

For procurement leadership, the transferable capability is the same:

Quail eggs force cross-functional alignment because the trade-offs are visible and measurable:

When those metrics are in place, quail eggs stop being a “specialty item problem” and become a repeatable procurement playbook for any fragile, yield-sensitive, compliance-exposed food category.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.