This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Procurement teams don’t “just buy seaweed” in this category—they buy functional performance, predictable yield, documentation readiness, and continuity from a supply chain that is fragmented upstream (smallholders) but often bottlenecked midstream (processors with alkali throughput and QA release discipline). This guide explains the real control points that determine total landed cost (TLC/TCO), why “cheaper PES” often becomes more expensive after receipt, and how to operationalize a sourcing approach that is defensible to QA, operations, and auditors.

(Analyzed at: Apr, 2026)

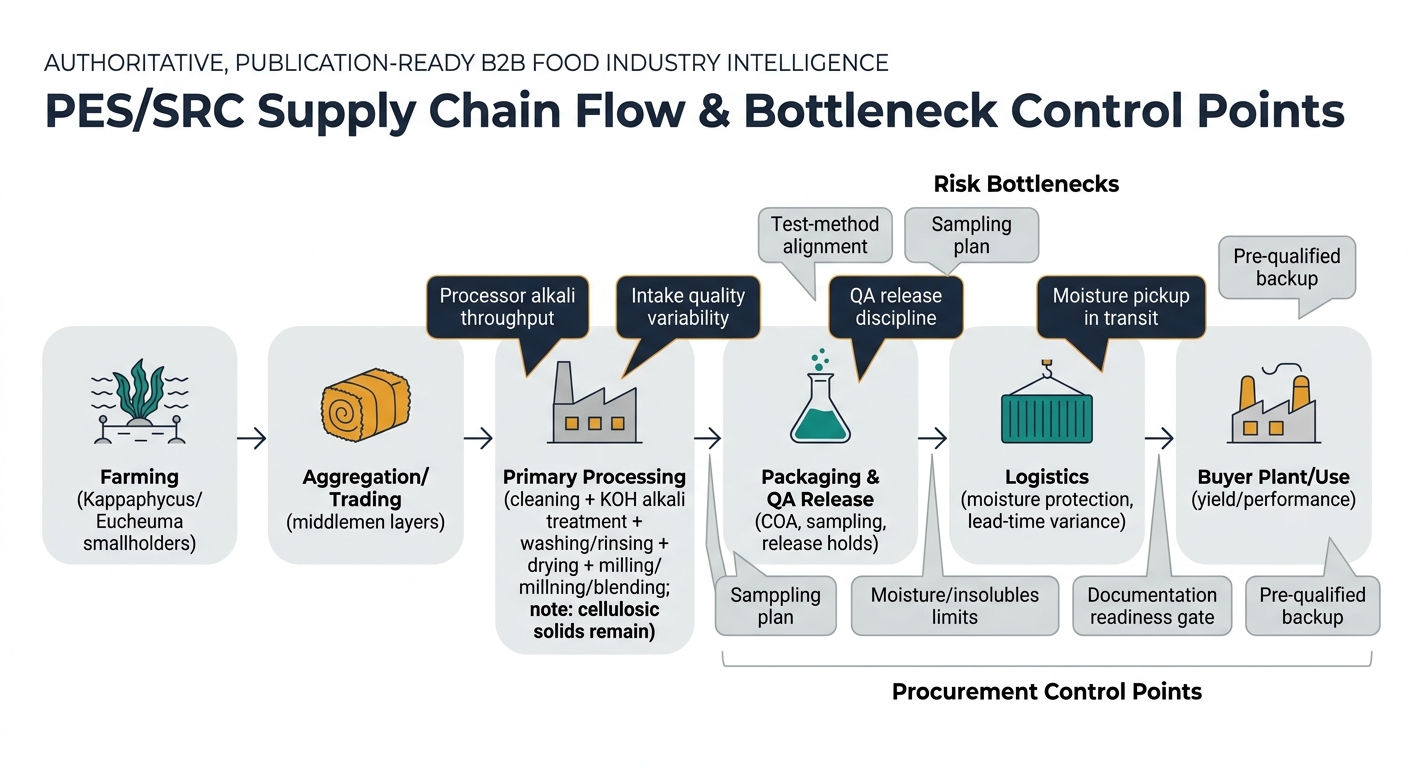

Processed Eucheuma Seaweed (PES) sits in the middle of a supply chain that starts as smallholder coastal aquaculture and ends as a functional hydrocolloid input (often into dairy/alt-dairy, processed meats, sauces, confectionery, and pet food). In practice, sourcing teams are rarely buying “seaweed” in a simple sense—they’re buying functional performance + documentation + continuity.

How the flow typically works (and where procurement pain shows up):

Farming (Kappaphycus/Eucheuma “eucheumoids”)

Aggregation & Primary Handling (village consolidators → traders)

Primary Processing (Cleaned/Graded Dried Seaweed; and/or PES/SRC)

Secondary Processing (Refined carrageenan or blended systems)

Packaging & QA release

Logistics & Distribution

Origin reality (concentration):

Key insight: In PES/SRC, the “price per kg” is often a misleading procurement anchor because moisture, insolubles/foreign matter, and functional performance variability drive hidden cost via yield loss, rework, and plant disruptions. The biggest value-add (and margin capture) tends to sit in cleaning/drying discipline + alkali processing throughput + QA release capability, not in farming alone.

What matters operationally

Cost drivers

Procurement “tell”

What matters operationally

Cost drivers

Procurement “tell”

What matters operationally

Cost drivers

Procurement “tell”

What matters operationally

Cost drivers

What matters operationally

Cost drivers

What matters operationally

Cost drivers

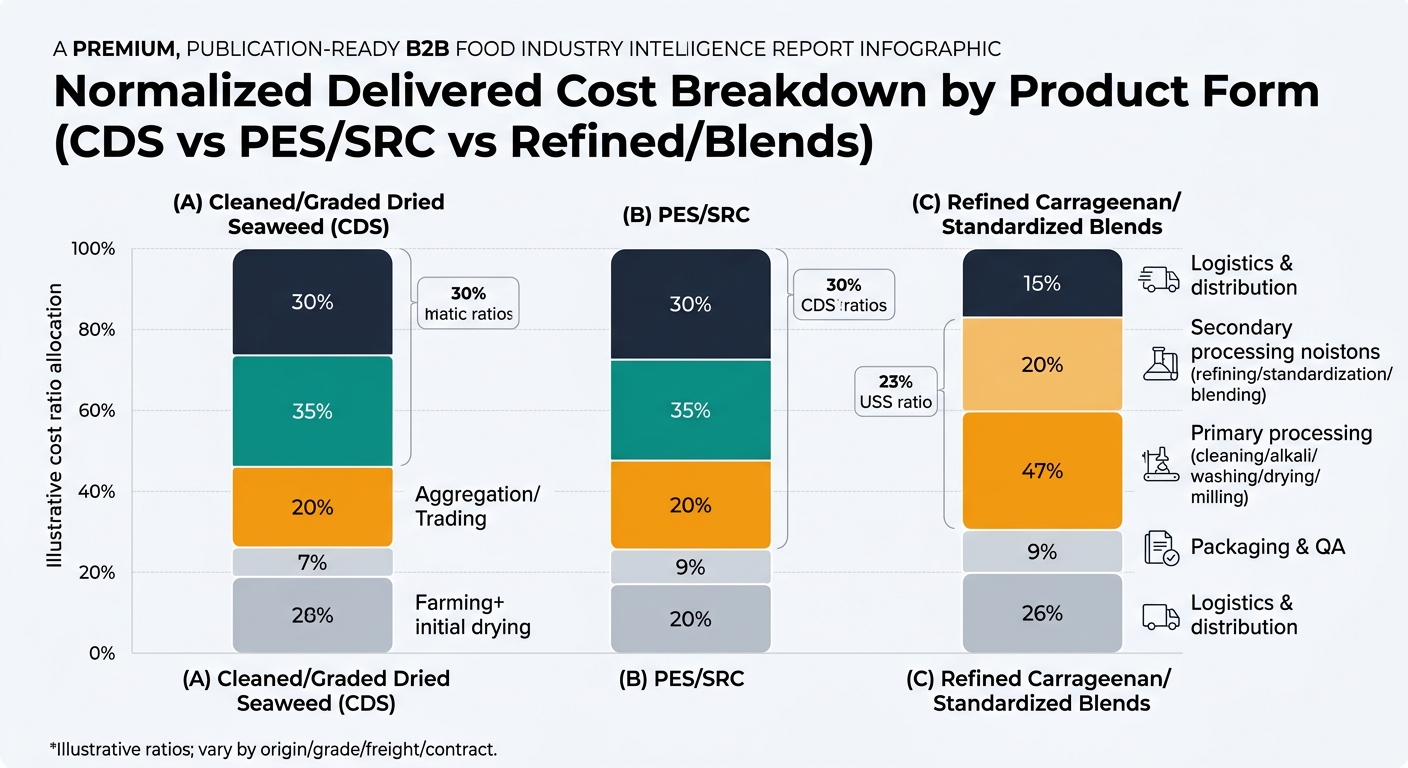

These are modeled ratios to show where cost concentrates by product form. Actual ratios vary by origin, grade, contract structure, and freight market. Use them as a sanity-check framework, not as a quoting tool.

| Supply chain node | Cost ratio (% of final delivered cost) | What moves the needle |

|---|---|---|

| Farming + initial drying | 45% | Weather-driven yield, labor availability |

| Aggregation/trading | 15% | Sorting losses, mixed lots, working capital |

| Primary processing (cleaning/grading) | 20% | Labor + drying control |

| Packaging & QA | 5% | Sampling/testing discipline |

| Logistics & distribution | 15% | Inter-island + ocean freight volatility |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves the needle |

|---|---|---|

| Farming + initial drying | 30% | Raw material tightness after disruption |

| Aggregation/trading | 10% | Intake variability, traceability loss |

| Primary processing (alkali + washing + drying + milling) | 35% | Energy/chemicals, throughput, rework rate [3] |

| Packaging & QA | 8% | Test failures → holds/rework |

| Logistics & distribution | 17% | Freight + inventory buffers |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves the needle |

|---|---|---|

| Farming + initial drying | 20% | Raw seaweed price cycles |

| Aggregation/trading | 8% | Traceability and lot segregation |

| Primary processing to semi-refined input | 20% | Conversion yield |

| Secondary processing (refining/standardization/blending) | 32% | Energy/water, filtration, QA intensity |

| Packaging & QA | 10% | Compliance + tighter release specs |

| Logistics & distribution | 10% | Value density reduces freight share |

PES/SRC is a “processed commodity,” but the supply chain behaves like a hybrid of commodity + specialty ingredient:

This is why supplier risk is not only “country risk.” It’s processor bottleneck risk (capacity, intake controls, QA release discipline) layered on top of origin exposure.

The most common price-performance disconnect comes from unpriced variability:

Moisture and insolubles behave like a hidden tax

“Same grade” is not the same product unless test methods match

Processing discipline determines functional consistency

Disruption signals hit upstream first, but your cost impact hits later

Real-world risk pattern (disease/environment):

Awarding on lowest quote without spec normalization

Treating origin diversification as sufficient risk management

Running qualification only after a disruption

Selected capabilities (only what changes decisions):

Decision you control: “Are these quotes comparable enough to award?”

Action pattern

Outcome

What we cannot conclude without your inputs (explicit limits)

Decision you control: “Do we have qualified backups per critical spec—and how fast can we switch?”

Action pattern

Outcome

Quote-to-award governance that prevents false savings

Supplier segmentation for allocation rules

Risk register designed for this category (not generic)

Performance governance cadence

The same “processed commodity with hidden variability” pattern shows up in:

The procurement lesson is consistent: normalize specs, measure performance drift, and pre-qualify alternates before the market forces you to.

Processed Eucheuma Seaweed is a high-leverage category because it forces clarity on the procurement fundamentals that auditors, QA, and operations care about:

In short: PES/SRC sourcing is where procurement maturity shows—because the market will punish any gap between price and delivered performance.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.