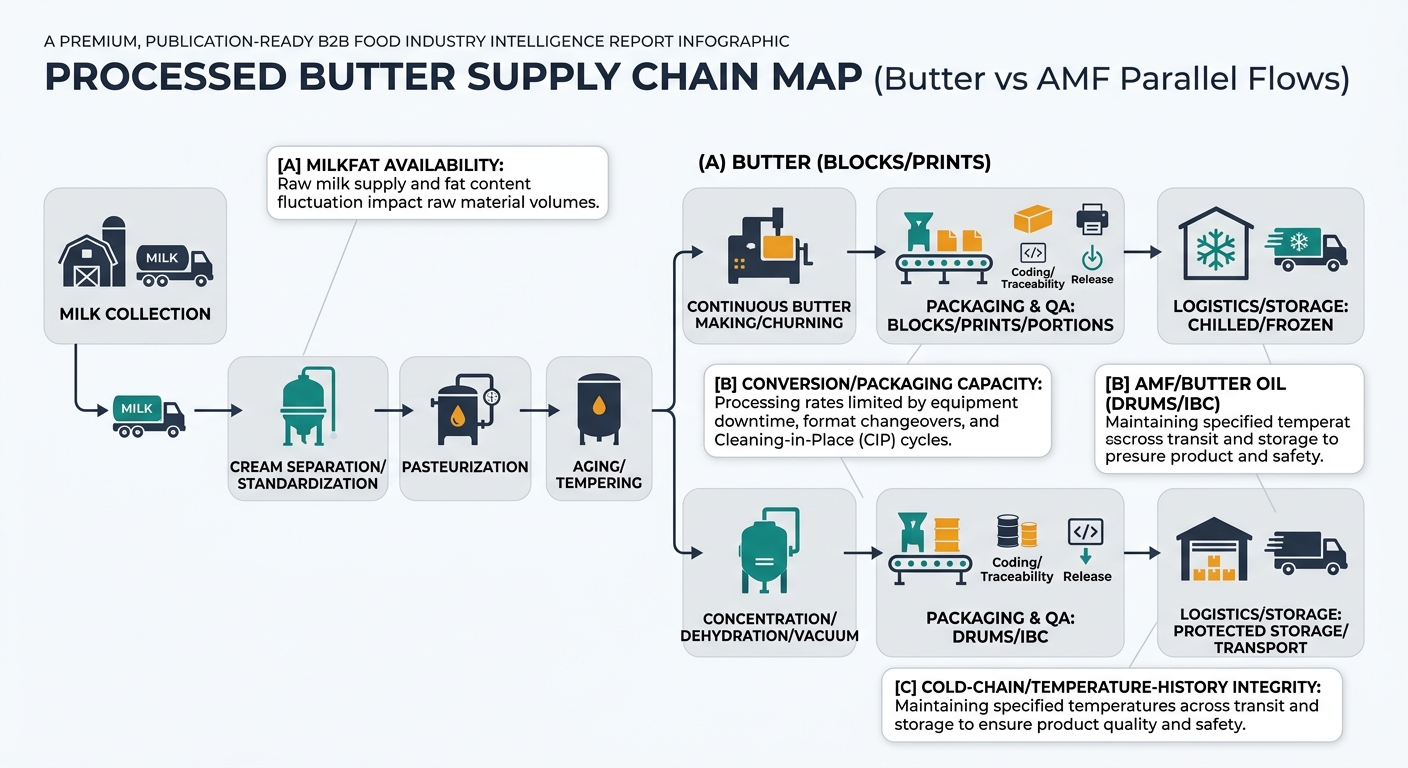

Processed butter looks like a “simple” ingredient, but procurement outcomes are mostly determined by a few physical realities: milkfat availability, conversion/packaging capacity, and cold-chain discipline. This guide maps the chain node-by-node, shows where costs get locked in, and translates those realities into contracting and supplier-management decisions.

Processed butter is a milkfat concentration business: you start with raw milk, separate and standardize cream, then convert that fat into a water-in-oil emulsion (butter) or an almost water-free fat (AMF). The physical chain is short, but it is capital- and cold-chain-dependent—so conversion capacity, refrigeration, and packaging lines often matter as much as the farm.

Insight: Butter cost structure is “built” upstream (milkfat availability) and “realized” downstream (conversion yield, cold-chain handling, and pack format complexity).

Data: Codex-aligned references commonly define butter as a water-in-oil emulsion with ≥80% milkfat and ≤16% water; industry standards for anhydrous milk fat (AMF) commonly reference ≥99.8% milkfat with ≤0.1% moisture, reflecting very different processing and logistics requirements [1].

Procurement Impact: Even before commercial strategy, your physical constraints (spec, pack format, storage temperature, and lane length) determine which suppliers are feasible and which cost nodes will dominate your landed cost.

Insight: Butter has fewer supply-chain steps than many ingredients, but each node has a high fixed-cost base (plant utilization, energy, sanitation/CIP, and refrigeration). Margins are often earned by controlling yield loss, moisture compliance, oxidation defects, and pack-format efficiency—not by “mystery markups.”

Data: Butter and AMF must meet compositional limits (fat/water/SNF) and sensory/defect expectations; AMF’s very low moisture is a stability requirement for storage and long-haul distribution [1].

Procurement Impact: Your total cost is most sensitive to (1) milkfat-to-butter yield economics, (2) conversion capacity and downtime risk, and (3) cold-chain and packaging choices that change handling loss and shelf-life risk.

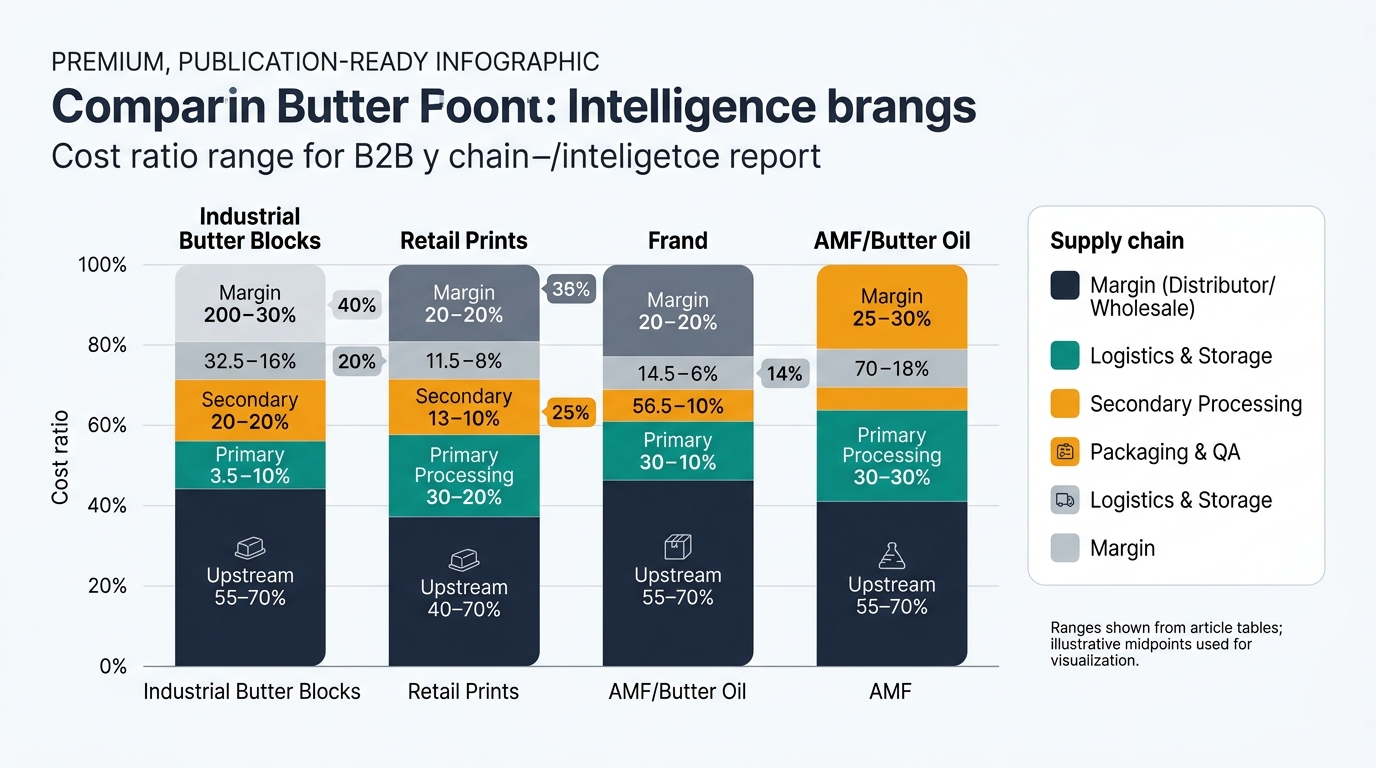

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream / Raw Material (milk → cream) | 55–70% | Milkfat value dominates; yield and quality set the baseline. |

| Primary Processing (pasteurize/temper) | 4–7% | Energy + refrigeration + QA throughput. |

| Secondary Processing (butter making) | 6–10% | Conversion labor, CIP, utilization, moisture control losses. |

| Packaging & QA | 4–8% | Blocks are efficient but still sensitive to coding/traceability holds. |

| Cold-chain logistics & storage | 6–12% | Reefer freight + cold storage + shrink/claims risk. |

| Distributor/wholesale margin | 5–12% | Varies by channel and service requirements. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream / Raw Material (milk → cream) | 40–60% | Still dominant, but packaging and retail margin rise sharply. |

| Primary Processing (pasteurize/temper) | 3–6% | Similar physics; tighter sensory expectations often increase QA. |

| Secondary Processing (butter making) | 5–9% | Conversion cost similar, but smaller runs can hurt utilization. |

| Packaging & QA | 10–18% | Wraps/cartons, frequent changeovers, higher inspection intensity. |

| Cold-chain logistics & storage | 6–12% | More handling points increase temperature-excursion exposure. |

| Retail/brand margin | 10–25% | Marketing, slotting, and retailer markup dominate. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream / Raw Material (milk → cream/butter feedstock) | 70–85% | Nearly pure fat product; raw fat economics dominate. |

| Primary Processing (pasteurize/condition) | 2–5% | Conditioning before concentration; energy and QA. |

| Secondary Processing (concentration/dehydration) | 5–10% | Must achieve very low moisture (≤0.1%) for typical AMF specs [4]. |

| Packaging & QA | 2–5% | Drums/liners; oxygen/light control matters for flavor stability. |

| Logistics & storage | 3–8% | Better freight per unit of fat than butter, but heat exposure still a risk. |

| Distributor/wholesale margin | 3–8% | Often lower than retail butter channels. |

Insight: Butter supply chains are structurally constrained by biology (milk seasonality), concentrated conversion assets (plants), and cold-chain physics (temperature history). These realities don’t disappear in “normal” markets.

Key Takeaways: Moisture compliance is both a quality requirement and a yield driver; packaging format can rival conversion cost in retail; and cold-chain failures often masquerade as “supplier quality” issues.

(Analyzed at: Apr, 2026)

Lock in a two-part commercial structure: (1) an index-linked price component tied to a transparent butter/butterfat reference, and (2) a separately negotiated capacity-and-service addendum that hard-codes pack-format line time, changeover expectations, and cold-chain controls (temp logging, max dock dwell, claim rules). This works because 2026 pricing has shown meaningful volatility while operational constraints (eligible inventory dynamics, cold storage tightness, and packaging/logistics bottlenecks) can still create “allocation outcomes” even when the headline price looks favorable. Teams that separate commodity value from cost-to-serve typically protect on the order of ~1–3% of landed cost through fewer holds, fewer shorts, and fewer temperature-history claims—without pretending they can outsmart the market [2].