This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

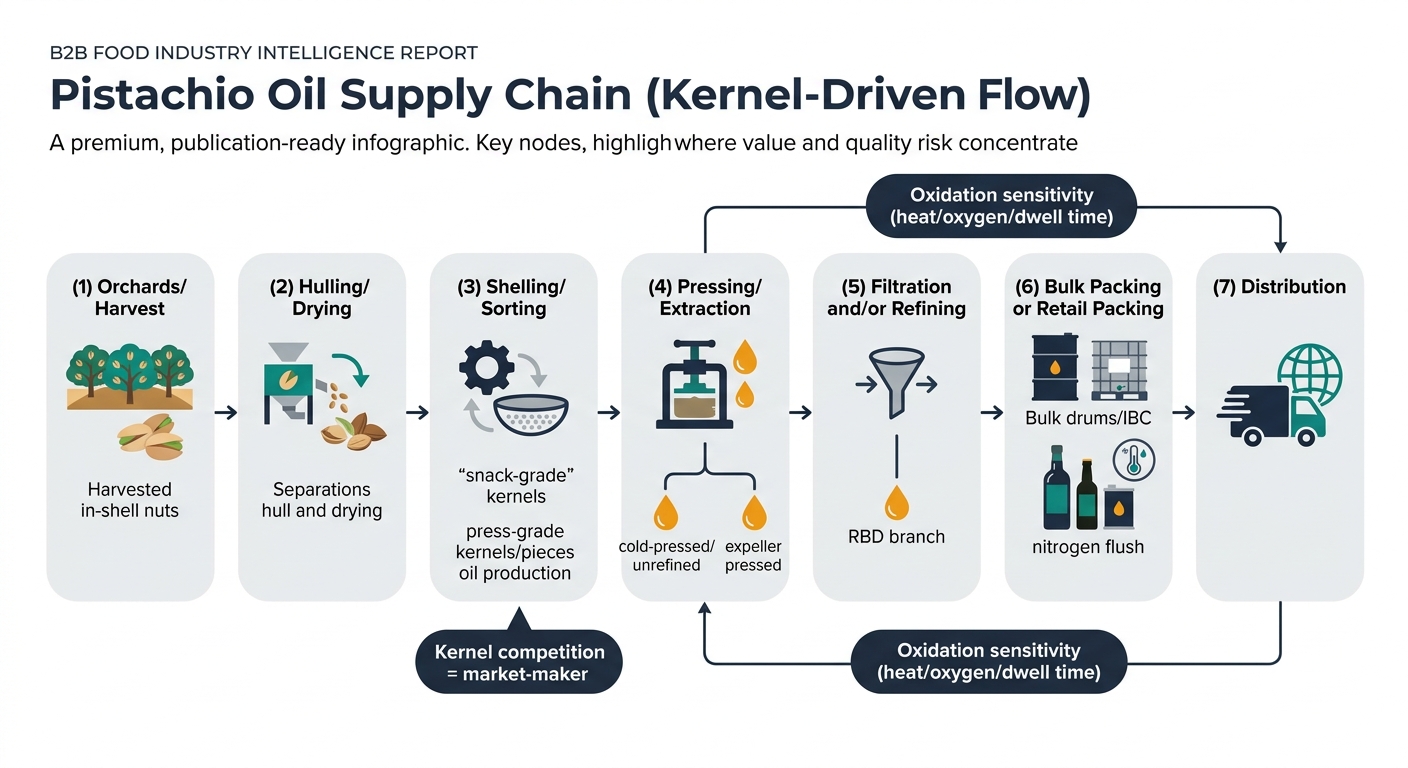

Pistachio oil is not a “commodity oil” supply chain where crushing capacity sets the market (like soybean). It is a kernel-driven specialty oil where the economics and availability are dominated by pistachio nut supply, quality rejects, and the ability to protect freshness through processing and logistics.

Key insight: Pistachio oil cost is structurally concentrated upstream in kernels, with downstream processing/packaging amplifying variance depending on whether you buy bulk ingredient oil or premium retail oil.

Below, I break cost and margin logic by node, then model illustrative cost ratios for common pistachio-oil product forms.

Aflatoxin control is a real economic lever: under EU maximum levels for almonds/pistachios/apricot kernels placed on the market for the final consumer or as an ingredient, the limits are 8.0 µg/kg for aflatoxin B1 and 10.0 µg/kg for total aflatoxins (B1+B2+G1+G2). [3]

These are illustrative ratios to show where cost concentrates. Actual ratios vary by origin, crop year, grade/spec, pack size, incoterms, and whether you buy spot vs contract.

| Supply Chain Node | Cost Ratio (% of Delivered Cost) | What procurement should watch |

|---|---|---|

| Kernels / upstream raw material | 55% | Kernel market tightness, crop outlook, allocation risk |

| Shelling/sorting & primary handling | 10% | Reject rates, aflatoxin controls, segregation |

| Pressing/extraction | 8% | Yield, batch size, filtration discipline |

| Refining (RBD) | 7% | Energy cost, yield loss, spec consistency |

| Packaging & QA | 5% | Drum/IBC quality, COA completeness |

| Logistics & distribution | 7% | Transit heat exposure, dwell time |

| Supplier + channel margin | 8% | Payment terms, volume commitments |

| Supply Chain Node | Cost Ratio (% of Delivered Cost) | What procurement should watch |

|---|---|---|

| Kernels / upstream raw material | 50% | Freshness of kernels, storage conditions |

| Shelling/sorting & primary handling | 10% | Oxidation screening, aflatoxin controls |

| Pressing/extraction | 12% | Temperature control, filtration, oxygen exposure |

| Refining | 0% | N/A |

| Packaging & QA | 8% | More testing (PV/FFA/sensory), oxygen management |

| Logistics & distribution | 8% | Summer lanes, storage temperature |

| Supplier + channel margin | 12% | Premium for sensory + smaller lots |

| Supply Chain Node | Cost Ratio (% of Delivered Cost) | What procurement should watch |

|---|---|---|

| Kernels / upstream raw material | 35% | Kernel price still matters, but diluted by downstream costs |

| Shelling/sorting & primary handling | 7% | Quality rejects |

| Pressing/extraction | 10% | Batch control + sensory consistency |

| Packaging & QA | 18% | Glass/tin, nitrogen flush, labeling, coding |

| Logistics & distribution | 10% | Damage, temperature, retail warehousing |

| Wholesale/retail margin | 20% | Channel economics dominate |

Key insight: For pistachio oil, the “crush spread” logic is weak. The upstream kernel market drives availability and pricing.

Procurement teams often expect a clean pass-through: kernels up → oil up immediately. In practice, pistachio oil pricing shows lags and discontinuities.

Your negotiation should separate:

Below is how a procurement intelligence service changes outcomes in pistachio oil—mapped to the management decisions you actually own.

Standardize a pistachio-oil approval gate (what must be true before first PO):

The same intelligence-based sourcing discipline applies to other “premium, authenticity-exposed, origin-concentrated” ingredients:

Once you build repeatable motions (spec equivalency, dual-source readiness, risk triggers), you can reuse them across premium oils and nut-derived ingredients.

Pistachio oil forces best-practice procurement because it combines:

If your team can run pistachio oil with controlled specs, qualified alternates, and clear risk triggers, you can apply the same model to a wider set of specialty ingredients—improving:

This guide is written for procurement and sourcing managers who already know how to run competitive events and manage supplier performance—but may not have deep pistachio-oil category context. The goal is to translate pistachio-oil “category truths” (kernel-driven economics, harvest timing, oxidation fragility, and food-safety governance) into repeatable buying motions: how to set specs that make quotes comparable, when to contract, how to dual-source without QA gridlock, and which disruption triggers should force action.

(Analyzed at: Apr, 2026)

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.