This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Peanut butter spread looks simple from the outside—“just peanuts.” For procurement leadership, it behaves more like a multi-constraint category where compliance (aflatoxin), capacity (roast/grind/fill), and packaging (jars/lids/labels) decide whether product ships on time and within spec. This guide translates those realities into management-grade decisions: where to dual-source, how to structure contracts, what to monitor, and which KPIs actually predict continuity.

Analyzed at: Apr, 2026

Most procurement teams think peanut butter spread is a single-ingredient category (peanuts) with a simple conversion cost. In practice, it’s a multi-constraint system where supply continuity is gated by:

Procurement implication: Your continuity risk is rarely “peanuts unavailable.” It’s more often “compliant peanuts + available line time + the right jar/lid + release testing capacity” all aligning in the same window.

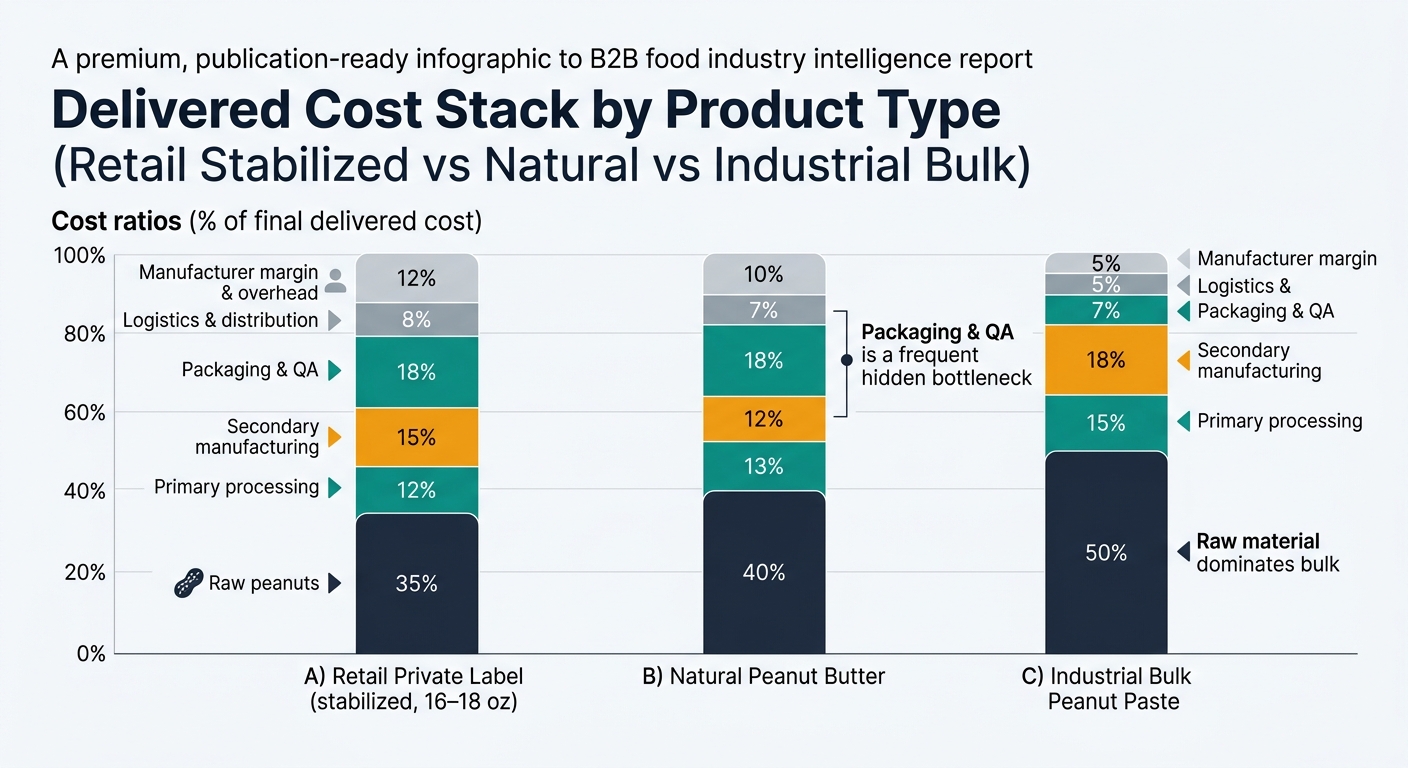

Below is a management-grade view of where cost and margin tend to stack—not as accounting truth, but as a practical map for negotiation posture and risk trade-offs.

Key insight: In peanut butter spreads, kernel cost volatility is often the biggest P&L driver, but the food-grade compliant premium can become the swing factor when aflatoxin risk rises (because rejects/diversion increase effective cost per compliant pound).

Key insight: This node is where food safety compliance becomes a cost function—sampling density, rejects, and rework can materially change effective yield.

Key insight: “Same peanut butter” is not the same operationally. Natural vs stabilized, crunchy vs smooth, and sugar/salt profiles change line rates, sanitation time, and rework risk.

Key insight: Packaging is often the constraint that turns a peanut event into a customer-service event. Even when ingredients are available, the wrong jar, lid, or label can stop shipments.

Packaging format changes are rarely 1:1 substitutes; tooling, line settings, performance, and consumer expectations create friction. In many programs, glass also carries longer and less flexible supply/transport dynamics than plastic—validate by your specific jar finish/closure and decoration method.

Key insight: Peanut butter is “ambient,” but not “risk-free.” Heat exposure accelerates oil separation and rancidity, which can turn into customer complaints and returns.

Key insight: Retail pricing often lags kernel cost moves due to inventory and promo calendars; procurement gets squeezed when input costs move faster than shelf price resets.

Percentages below are approximate shares of final delivered cost to the buyer (retail-ready or bulk-delivered). Actual ratios vary by origin, contract structure, pack format, and whether you’re buying branded, private label, or industrial.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw peanuts (kernels equivalent) | 35% | Dominant driver; quality/compliance premium can widen in aflatoxin years |

| Primary processing | 12% | Sorting/roasting energy + QA; yield loss matters |

| Secondary manufacturing | 15% | Mixing + changeovers + line efficiency |

| Packaging & QA | 18% | Jar/lid/label/corrugate + release testing |

| Logistics & distribution | 8% | Ambient freight + warehousing |

| Manufacturer margin + overhead | 12% | Co-man or plant overhead allocation |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw peanuts | 40% | Higher peanut content; tighter flavor consistency expectations |

| Primary processing | 13% | Roast profile consistency is critical |

| Secondary manufacturing | 12% | Fewer additives, but tighter process control to manage separation |

| Packaging & QA | 18% | Packaging still heavy; QA may include more sensory/texture checks |

| Logistics & distribution | 7% | Heat exposure risk increases complaints/returns |

| Manufacturer margin + overhead | 10% | Often offset by lower additive cost but higher quality risk |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw peanuts | 50% | Input dominates; buyers often index or benchmark tightly |

| Primary processing | 15% | Sorting/roasting/QA heavy |

| Secondary manufacturing | 18% | Grinding + viscosity/particle size control |

| Packaging & QA | 7% | Bulk packs cheaper per lb |

| Logistics & distribution | 5% | Typically pallet bulk |

| Manufacturer margin + overhead | 5% | More commoditized; margin pressure higher |

If you source globally (or sell into multiple regions), the same lot of peanuts can be acceptable in one market and rejected in another.

Procurement implication: “Aflatoxin compliant” is not a binary claim. You need:

Avoid stating “U.S. guidance allows a higher allowance for raw peanuts under certain programs” unless you can cite the exact program and limit you are using internally. In practice, procurement should treat 20 ppb as the widely used action level reference for food and build governance around destination market requirements and your brand/customer risk appetite.

Procurement teams expect a simple relationship: kernel price down → peanut butter cost down. In practice, the relationship breaks for four repeatable reasons:

Management takeaway: If you only track peanut kernel prices, you’ll miss the real drivers of variance: compliance premium, capacity premium, packaging premium, and contract lag.

A real-world reminder: the May 2022 Jif peanut butter Salmonella outbreak triggered a major recall and broad downstream disruption, illustrating how a single facility-level food safety issue becomes a supply continuity and reputational event.

This is how procurement intelligence changes outcomes in peanut butter spreads—by improving decision quality under real constraints.

Peanut butter spreads are a clean example of a broader procurement truth: the biggest risks sit at the intersections—compliance, capacity, and packaging—not just commodity price.

Examples procurement leaders commonly recognize:

Peanut butter spread is a procurement training ground because it forces four disciplines to operate together:

If your team can run peanut butter spreads with:

…you can apply the same operating model to a wide range of shelf-stable food categories with fewer surprises and fewer escalations.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.