This guide is a procurement-first map of how organic cashews physically move from farm to your dock, where cost and risk “lock in,” and which specs matter most when you’re trying to stabilize landed cost without compromising organic integrity. It’s written for sourcing leaders who know procurement well but don’t live in the cashew category day to day.

Organic cashew kernels are a two-step global chain: seasonal raw cashew nuts in shell (RCN) are harvested and dried near farms, then most value is created in processing hubs that convert RCN into graded kernels under tight moisture and segregation controls. The fixed cost-drivers are concentrated in (1) farm-level drying and aggregation (quality + organic integrity), (2) primary processing yield and breakage (whole-kernel recovery), and (3) packaging/handling that protects kernels from oxygen and humidity through long ocean transits.

Orchard harvest → nut separation from apple → drying to safe moisture → bagged RCN aggregation → conditioning (steam/thermal) → shelling → kernel drying → peeling (testa removal) → grading (whole/splits/pieces; white vs scorched) → bulk vacuum/N2 pack → container export → import QA + documentation check → optional roasting/flavoring/milling → retail/industrial pack.

Insight: Organic cashew cost builds in layers: upstream compliance + handling protects organic integrity, but the largest “irreversible” cost is created when processors convert RCN into a grade mix.

Data (validated concept): The processor’s realized value is a weighted average of grades produced (e.g., W320 vs pieces), meaning breakage rate and defect removal drive both cost and margin.

Procurement Impact: Even without discussing buying strategy, you can map which node is responsible for which cost driver—yield loss, labor intensity, energy, packaging barrier performance, and logistics risk.

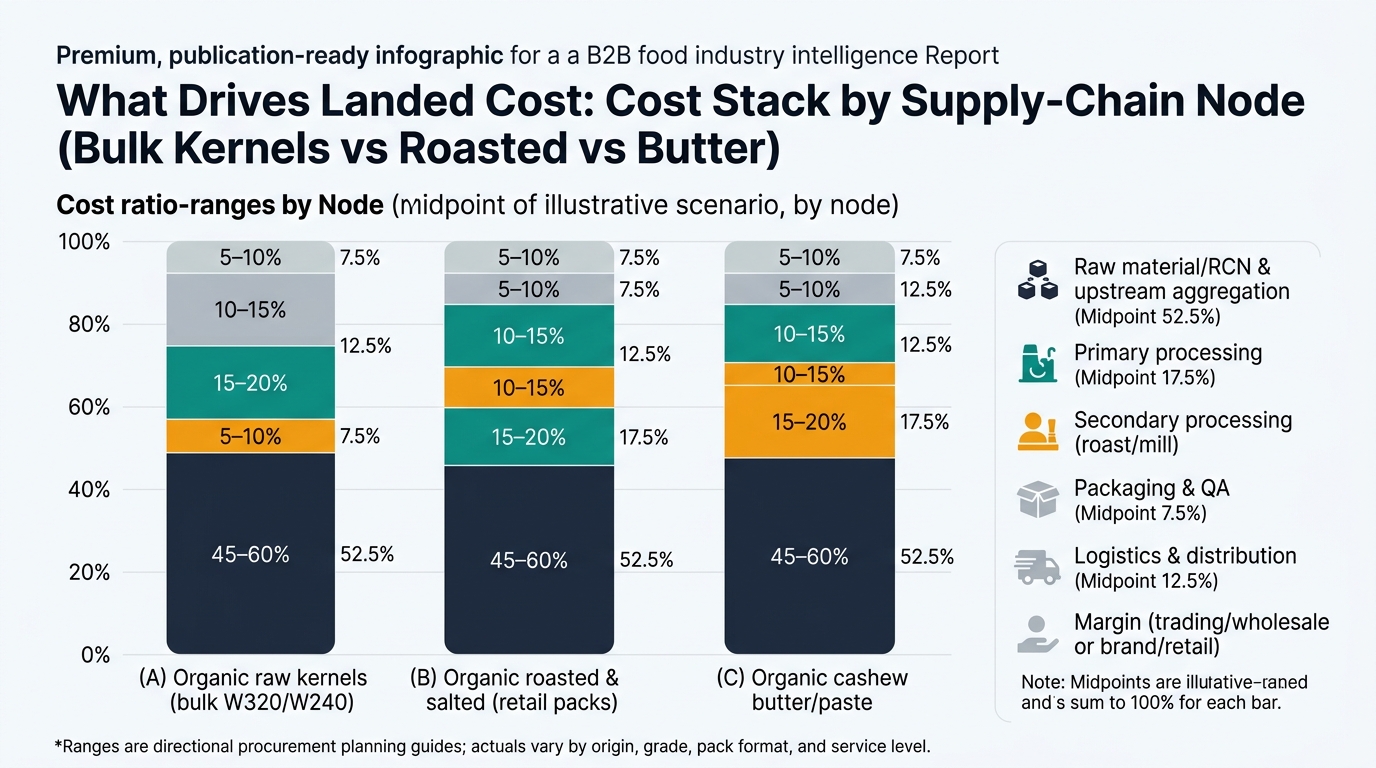

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw Material (RCN + farm/aggregation) | 45–60% | Dominated by RCN input economics and certified volume availability. |

| Primary Processing | 18–28% | Labor + energy + yield loss + grade outcome (wholes vs pieces). |

| Packaging & QA | 4–8% | Barrier bags, vacuum/N2, lab tests, organic document checks. |

| Logistics & Distribution | 6–12% | Freight + port/handling + inland + insurance; delays add working-capital drag. |

| Trading/Wholesale Margin | 6–12% | Varies by service level, financing, and consolidation role. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw Kernels Input | 30–45% | Kernel grade and defect profile determine usable yield in roasting. |

| Secondary Processing | 10–18% | Roasting energy, seasoning, labor, allergen/sanitation overhead. |

| Packaging & QA | 12–20% | Retail film/jars, gas flush, coding, higher QA and shelf-life validation. |

| Logistics & Distribution | 8–14% | Finished goods distribution is frequent and less dense than bulk. |

| Brand/Retail Margin | 15–30% | Retail category economics and promo intensity drive the spread. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw Kernels Input | 28–42% | Pieces can be economical, but oxidation control becomes more critical. |

| Secondary Processing (milling) | 12–22% | Milling, heat management, particle size control, sanitation. |

| Packaging & QA | 14–24% | Oxygen barrier and headspace control are key; jars/tubs add cost. |

| Logistics & Distribution | 7–13% | Heavier packs; temperature excursions can affect texture/oil separation. |

| Brand/Channel Margin | 12–25% | Depends on private label vs branded and channel mix. |

Quick Win: Treat moisture/oxygen control and lot traceability as cost drivers—because they determine reject/downgrade rates and how much inventory stays saleable.

(Analyzed at: Apr, 2026)

Right now the cashew market is broadly described as stable-to-range-bound, but with meaningful logistics upside risk (routing disruptions and freight premiums can quickly erase any origin-side softness). [5] In that context, the most defensible contract move is to tie price to grade yield and documentation performance, not just a flat $/lb: require (1) a moisture spec aligned to trade standards (≤5% and a target packing range), (2) defined pack-out (vacuum/N2 high-barrier) and container humidity controls, and (3) “no-hold” organic paperwork readiness (including the NOP Import Certificate for U.S. arrivals). [2] When those controls are weak, the cost shows up as avoidable downgrades, production reschedules, and inventory holds—often a low-single-digit percentage of landed cost that feels small until it repeats across multiple containers and peak-demand weeks.