This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Orange Juice Concentrate (OJC) sourcing looks like a “commodity buy” until you live through a tight crop year: supply can be available but not accessible (allocation), price can move faster than contracts, and quality constraints can shrink usable supply overnight. This guide translates OJC supply-chain realities into procurement levers—so you can control landed cost volatility, reduce outage risk, and make decisions that are defensible with Finance, QA, Operations, and Legal.

Analyzed at: Mar, 2026

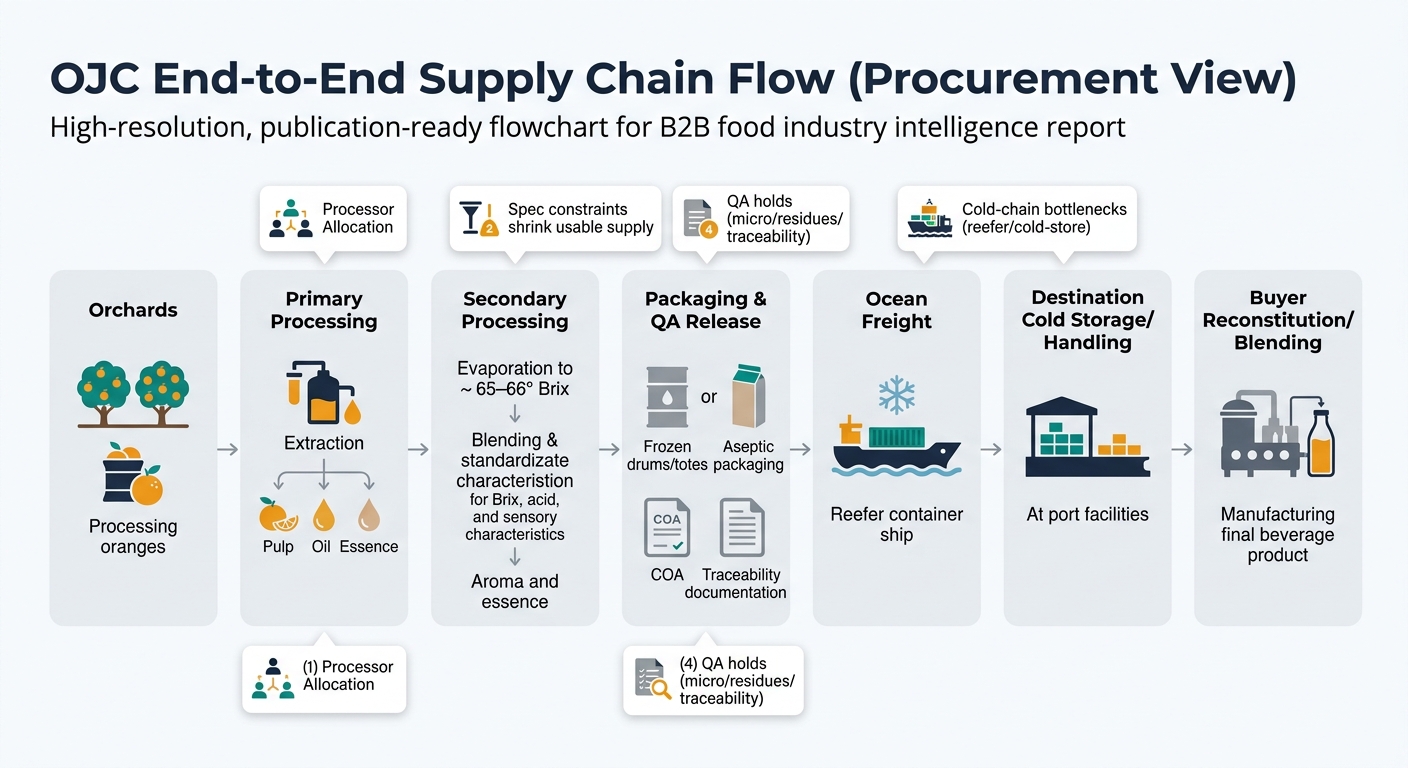

Orange Juice Concentrate (OJC)—especially FCOJ (frozen concentrated orange juice, typically ~65–66° Brix)—isn’t “just another fruit ingredient.” It’s a spec-driven, energy-intensive, cold-chain commodity whose availability is shaped by orchard biology, disease pressure, and a small number of highly integrated processors. [1]

Key insight: In OJC, your “price” is a stack of fruit economics + processing throughput + energy + cold-chain logistics + quality/compliance overhead. When supply is tight, the bottleneck shifts from “fruit availability” to allocation at processors and cold-chain capacity, changing who has pricing power.

Procurement implication: When fruit is structurally constrained, the “should-cost” anchor cannot be built from last year’s contract—use crop/production signals and origin diversification rules instead.

Procurement implication: During tight markets, suppliers may prioritize customers with stable offtake and operationally simple specs.

Procurement implication: If you demand narrow sensory or chemical tolerances without giving forecast stability, expect higher premiums and stricter allocation.

Procurement implication: Your total cost is sensitive to nonconformance risk (rejections, downgrades, reblends) more than many teams model.

Procurement implication: Incoterms and who controls cold-chain nodes can swing outcomes as much as unit price.

Procurement implication: “Cheaper” concentrate can be more expensive after line losses + QA interventions.

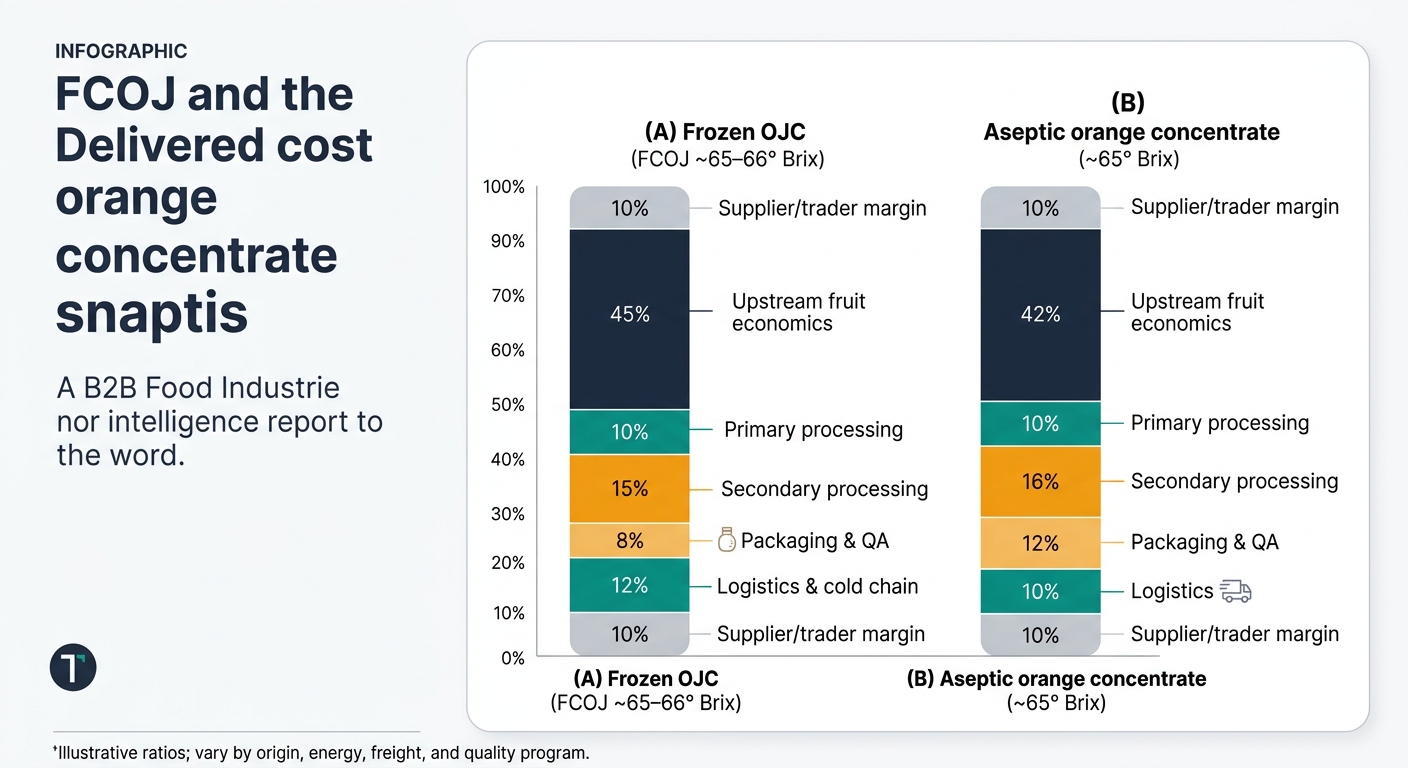

Modeled shares as % of final delivered cost to a U.S. beverage plant. These ratios vary by origin, contract tightness, energy/freight, and quality program.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream fruit economics | 45% | Dominant driver in most cycles; disease/weather amplify structural floor |

| Primary processing | 10% | Extraction yield + plant uptime |

| Secondary processing | 15% | Evaporation energy + standardization/blending |

| Packaging & QA | 8% | Drums/liners + COA release holds |

| Logistics & cold chain | 12% | Reefer + destination cold storage + handling |

| Supplier/trader margin | 10% | Widens in tight allocation markets |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream fruit economics | 42% | Similar fruit exposure |

| Primary processing | 10% | Comparable extraction economics |

| Secondary processing | 16% | Similar energy + tighter micro control |

| Packaging & QA | 12% | Aseptic packaging premium + handling controls |

| Logistics (less cold chain) | 10% | Lower cold-store dependence but still ocean + inland |

| Supplier/trader margin | 10% | Depends on availability and program stability |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream fruit economics | 40% | Blending flexibility can reduce fruit-grade penalties |

| Primary processing | 10% | |

| Secondary processing | 18% | More blending, rework risk, aroma/essence management |

| Packaging & QA | 10% | More frequent testing, tighter release criteria |

| Logistics & cold chain | 12% | Similar to frozen if FCOJ |

| Supplier/trader margin | 10% | Premium for consistency and service |

Key structural fact: The global OJC market is exposed to correlated shocks (weather + disease) and concentrated processing/export control.

What that means for a procurement manager:

In OJC, price and availability can move independently in ways that surprise non-specialists.

Procurement takeaway: A sourcing strategy that optimizes only unit price is fragile. You need a risk-adjusted landed-cost view that values service continuity.

This is not about “more data.” It’s about changing the decision process so you can act earlier and document why.

OJC is a clean example of a broader procurement truth: when supply is biologically constrained and geographically concentrated, intelligence beats negotiation tactics.

Comparable categories where the same playbook applies:

In each case, teams win by:

Orange juice concentrate forces clarity because it exposes the limits of “three quotes and a negotiation.”

For procurement and sourcing management, OJC becomes a repeatable template: build a fact base, define triggers, diversify intelligently, and make decisions that are defensible under stress.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.