This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

This guide is written for procurement and sourcing leaders who are strong category managers but don’t live in citrus every day. The goal is to translate how the orange-juice-concentrate market actually works (origins, processors, inventories, specs, cold chain) into decisions you can defend: what to buy, from whom, when, under what terms, and with what contingency.

(Analyzed at: Mar, 2026)

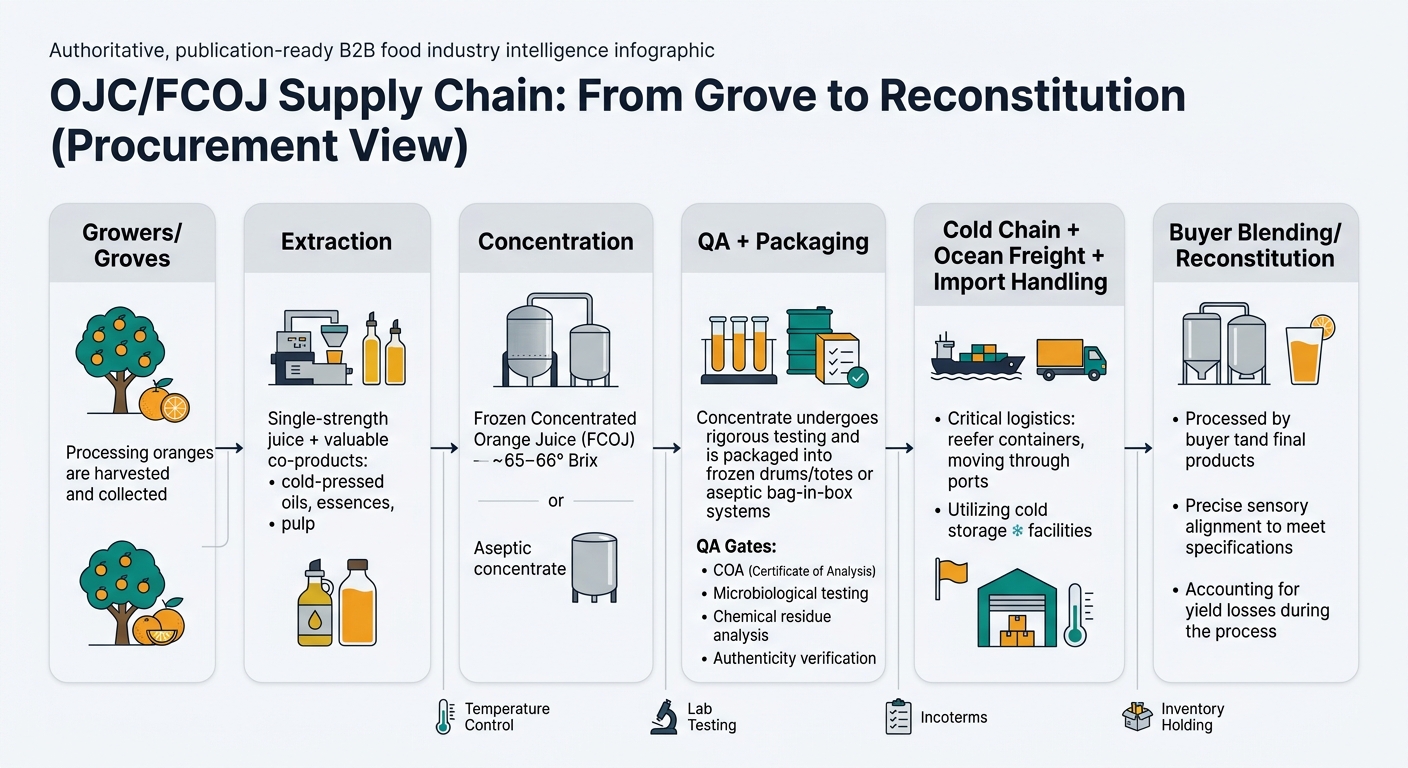

Orange-juice-concentrate (OJC/FCOJ) looks like a “simple” ingredient on a BOM. In reality, it is a scale-driven agro-industrial system where a few origins and a few processors set the tone for global availability, lead times, and pricing.

Below is the procurement-relevant cost logic: which levers move cost at each node, and what you can (and cannot) influence.

Key insight: Fruit cost is the largest single cost driver, but it’s not just “farmgate price.” It’s yield and survivability under disease pressure.

Florida’s structural decline is widely linked to citrus greening and repeated weather events; USDA reporting continues to show extremely low output levels versus historical norms. [4]

Key insight: Extraction economics are partially subsidized by co-products (orange oil/essences/pulp). When co-product values weaken, processors often need a higher netback from juice.

Key insight: Concentration is energy- and equipment-intensive. Tight years create a double hit: fruit scarcity + higher unit processing cost due to suboptimal utilization.

Key insight: QA is not overhead; it is a market-access gate. Residues, authenticity, and micro failures can turn “lowest price” into a write-off.

USDA/AMS provides grade/standard references for orange juice from concentrate that can anchor specification conversations (but it does not replace your product spec and lab validation). [5]

Key insight: For frozen concentrate, logistics is a quality-preservation system, not just a cost line.

Key insight: Many buyers under-budget the internal cost of “making concentrate usable”: blending, sensory alignment, and yield losses.

Modeled % of final delivered cost to your facility. Actual ratios vary by origin, contract terms, energy/freight, format, and spec strictness.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Fruit / grove economics | 45% | Yield + disease pressure are decisive. |

| Extraction & primary processing | 10% | Throughput and co-product credits matter. |

| Concentration (evaporation/freezing) | 15% | Energy + utilization + shrink. |

| Packaging & QA | 7% | Drums/totes + lab/testing + documentation. |

| Cold chain + freight + storage | 13% | Reefer premiums, cold storage, demurrage. |

| Supplier/Trader + import/distribution margin | 10% | Depends on route-to-market and credit terms. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Fruit / grove economics | 45% | Similar fruit exposure. |

| Extraction & primary processing | 10% | Similar. |

| Concentration + aseptic processing | 17% | More packaging/sterilization complexity. |

| Packaging & QA | 9% | Aseptic materials + validation. |

| Freight + storage (reduced cold-chain) | 9% | Typically less cold-chain dependence. |

| Supplier/Trader + import/distribution margin | 10% | Commercial structure dependent. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Fruit / grove economics | 55% | Higher fruit intensity per unit solids. |

| Extraction & stabilization | 15% | More sensitive to quality and handling. |

| Packaging & QA | 8% | Often tighter sensory/handling requirements. |

| Cold chain + freight + storage | 12% | Product-dependent. |

| Supplier/Trader + import/distribution margin | 10% | Market dependent. |

A common misunderstanding: “If the world produces a lot of oranges, juice supply is fine.”

The structural fact:Internationally tradable juice is constrained by (a) where industrial processing capacity is concentrated and (b) which origins export versus consume domestically.

Procurement implication: Your risk is less “global oranges” and more Brazil crop + Brazil processing + export logistics + inventory drawdowns.

CitrusBR’s audited inventory releases are one of the clearest public signals on Brazilian orange juice stocks (reported in FCOJ-equivalent at 66° Brix). CitrusBR reported 146.3k metric tons as of June 30, 2025 for member-held global inventories (FCOJ-equivalent). [3]

In OJC, procurement teams often expect: higher risk → higher price; lower risk → lower price. Reality is messier.

Procurement implication: You need a governance model that separates:

This is where procurement intelligence helps—not by predicting prices perfectly, but by making decisions earlier, with clearer trade-offs and audit-ready rationale.

Management decision: How much volume to lock for the next 3–9 months, and under what pricing structure.

Metrics to report: budget variance, contract coverage %, emergency spot buys.

Management decision: Which alternates to qualify now (even if not cheapest) to reduce time-to-switch.

Metrics to report: time-to-switch (days), supplier/origin concentration %, service level.

Management decision: Which suppliers are strategic vs leverage vs bottleneck.

Metrics to report: OTIF, claims rate, corrective action closure rate.

OJC is an extreme example of origin concentration + biological risk + processing bottlenecks—but the same decision logic applies to other procurement categories common in beverage/food portfolios:

The transferable lesson: price intelligence alone is insufficient. You need a combined view of physical availability, quality/compliance gates, and supplier/origin concentration.

If your governance model works in OJC, it usually works everywhere else—because OJC forces clarity on the hard parts of procurement:

In short, OJC rewards teams that treat sourcing as a managed risk-and-coverage portfolio, not a sequence of spot negotiations.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.