This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

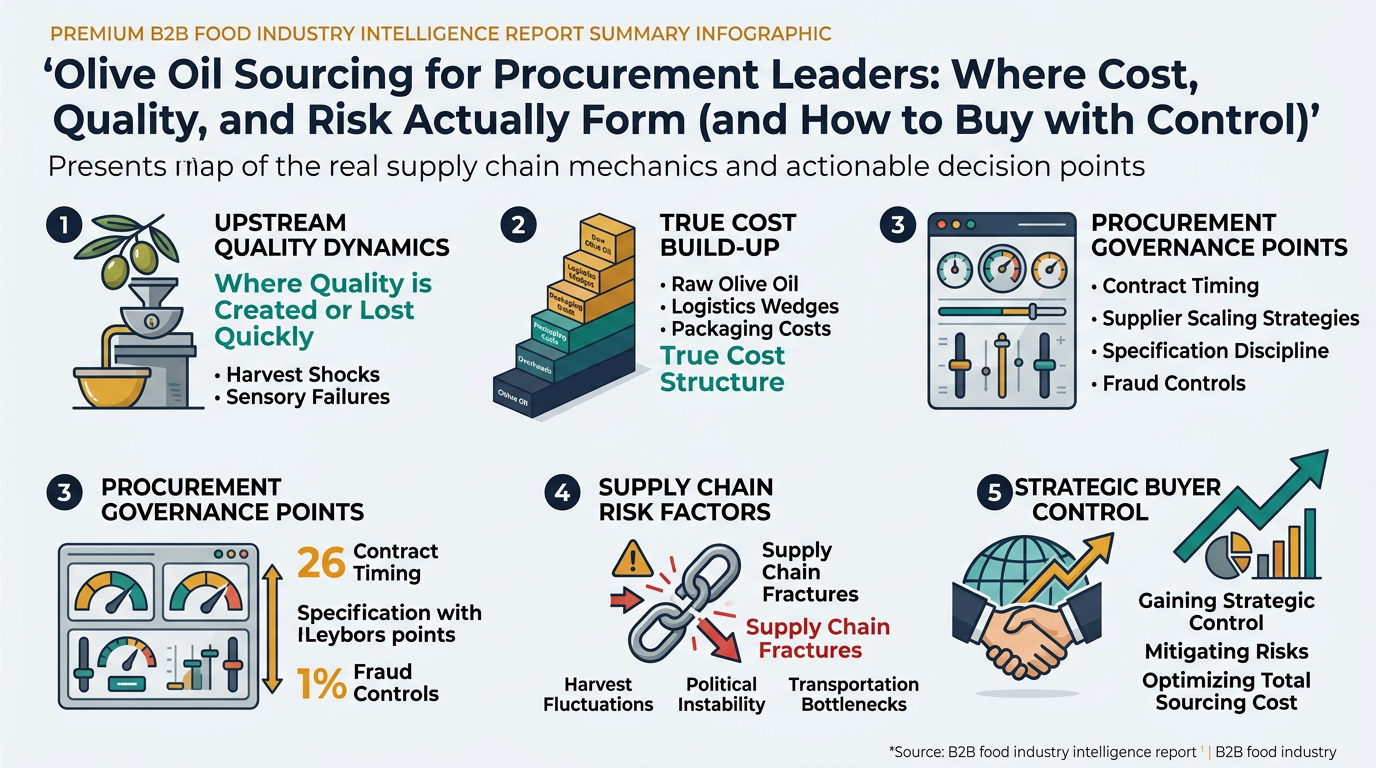

Olive oil is often treated like a commodity line item—until a harvest shock, a sensory failure, or an “unusually cheap” offer forces a fire-drill. This guide maps the real supply chain mechanics (where quality is created and lost), the true cost build-up (including packaging and logistics wedges), and the decision points procurement leaders can govern: contract timing, supplier scaling, spec discipline, and fraud controls.

(Analyzed at: Mar, 2026)

Olive oil procurement looks like a simple commodity buy until you map how value (and risk) is created.

A practical way to think about the flow is that olive oil has two different “centers of gravity”:

Key insight: Olive oil cost is driven by a combination of agricultural yield (kg oil per kg olives), grade outcomes (EVOO vs virgin vs lampante), and downstream standardization (refining/blending/packing). Procurement teams often over-focus on “per kg price” and under-model downgrade risk, storage losses, and packaging/logistics cost share.

What’s distinctive here

Primary cost drivers

What’s distinctive here

Primary cost drivers

What’s distinctive here

Primary cost drivers

What’s distinctive here

Primary cost drivers

What’s distinctive here

Primary cost drivers

What’s distinctive here

Primary cost drivers

These ratios are directional to show where cost concentrates by product form. Actual splits vary by origin, pack, lane, and market conditions.

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most |

|---|---|---|

| Groves & harvest | 50% | Yield, labor, drought/heat |

| Milling & early storage | 15% | Throughput constraints, downgrade risk |

| Refining/blending | 5% | Usually minimal for true EVOO lots |

| Packaging & QA | 5% | Chemistry + sensory release (where required) |

| Logistics & distribution | 15% | Freight, insurance, inventory time |

| Importer/broker margin | 10% | Market tightness, service level |

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most |

|---|---|---|

| Groves & harvest | 35% | Farmgate price, yield |

| Milling & early storage | 10% | Quality sorting, storage discipline |

| Refining/blending | 5% | Blending to profile (if multi-origin) |

| Packaging & QA | 20% | Glass, closures, labels, QA |

| Logistics & distribution | 15% | Packaged freight + warehousing |

| Wholesale/retail margin stack | 15% | Channel power, promo intensity |

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most |

|---|---|---|

| Groves & harvest | 25% | Lampante availability, harvest size |

| Milling & early storage | 10% | Feedstock quality |

| Refining/blending | 20% | Refining costs, blend ratios |

| Packaging & QA | 10% | Large-format packaging |

| Logistics & distribution | 15% | Weight/volume efficiency |

| Wholesale margin | 20% | Service, credit terms |

Olive oil is priced like an annual crop but consumed like a continuous input.

That mismatch creates predictable dynamics:

Recent years highlighted this: drought-driven shortfalls pushed prices to record levels, with Spain frequently acting as a reference market for global pricing. [4]

Procurement teams frequently expect a clean pass-through from “origin price” to delivered cost. In olive oil, several wedges break that assumption:

These are common errors when a team is strong in procurement but newer to olive oil:

Below is how procurement decisions improve when intelligence is tied to governance and operational triggers.

What changes with intelligence

Operational output

What changes with intelligence

Operational output

What changes with intelligence

Operational output

Olive oil is a clear example of a broader pattern: when quality is graded and supply is seasonal, “price-only sourcing” creates hidden cost.

Comparable categories procurement teams often manage:

The transferable lesson: decision intelligence is most valuable where your biggest losses come from uncertainty—quality failures, allocation, and poorly timed contracting—not from negotiation mechanics alone.

Olive oil forces clarity on three procurement fundamentals:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.