This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Mozzarella string cheese procurement looks straightforward (“refrigerated dairy snack”), but award and contract outcomes are usually decided by a handful of operational constraints: milk components and yield, plant and packaging-line capacity, and cold-chain execution. This guide is written for procurement & sourcing managers who are strong buyers in other categories but want a decision-ready mental model for string cheese—what to ask suppliers, what signals to track, and how to document trade-offs across cost, continuity, quality, and governance.

(Analyzed at: Apr, 2026)

Mozzarella string cheese looks like a simple refrigerated snack, but procurement outcomes are driven by a few non-obvious realities:

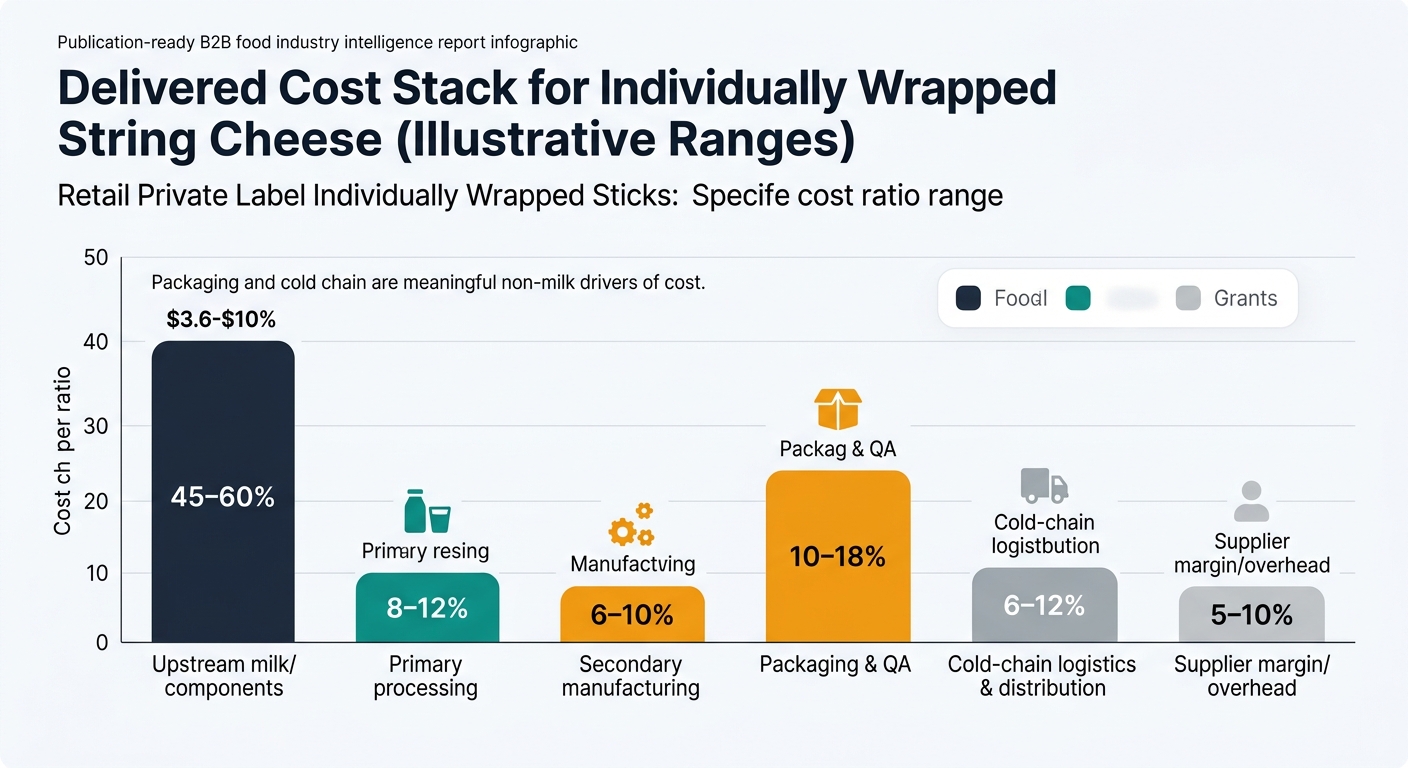

Below is the procurement-relevant cost and margin structure by node. Treat the percentages as illustrative ranges for North American sourcing; actual ratios move with milk markets, packaging resin, freight, and retailer program requirements.

Key insight: Most volatility originates here, but it expresses downstream with a lag depending on contract reset cadence.

Yield reality (why specs change cost): Cheese yield is commonly discussed as pounds of cheese per 100 pounds of milk, and it varies with milk components (fat/protein) and target moisture/fat in finished cheese. Treat yield as a commercial variable tied to spec, not just a plant technicality.

Key insight: This is where “milk in” becomes “cheese out,” and where byproduct economics (whey) can change a plant’s margin needs.

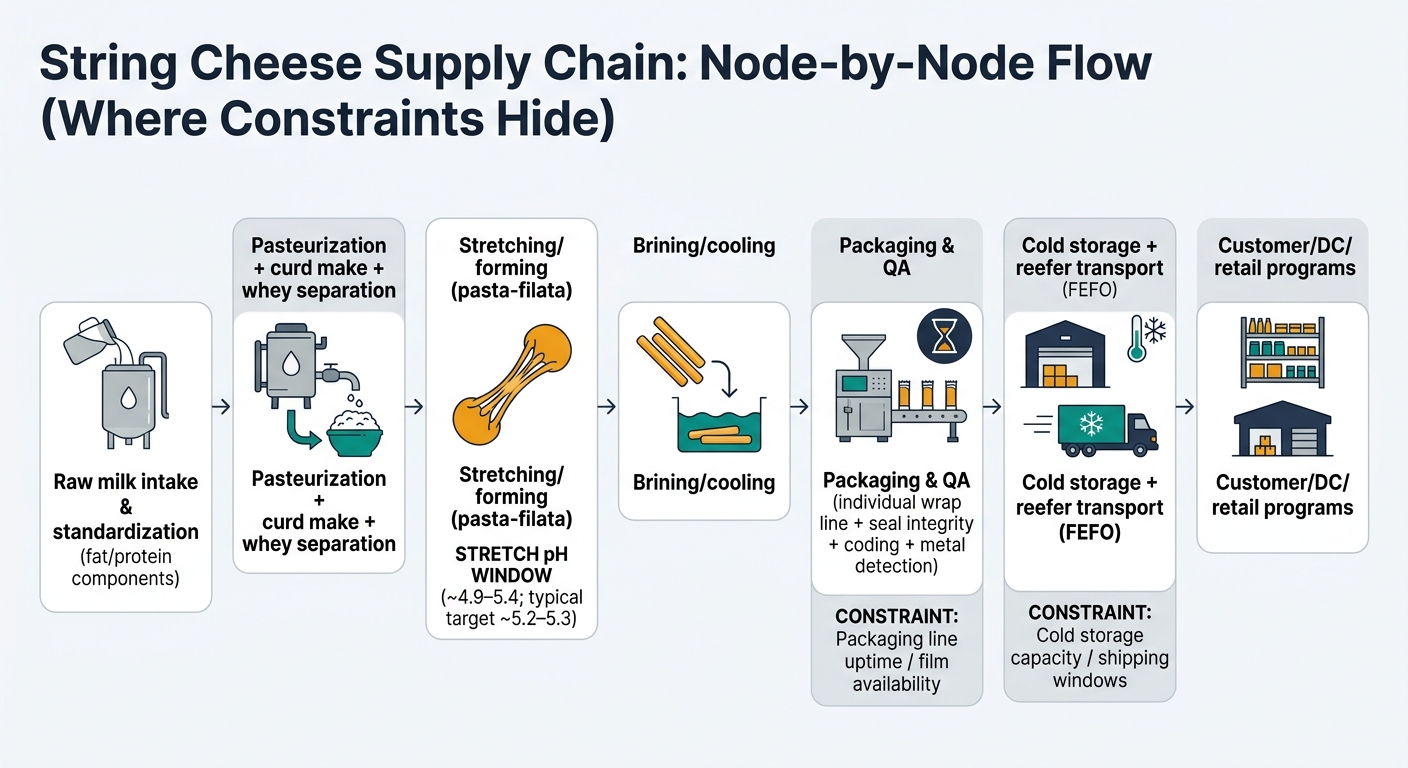

Key insight: String cheese is not “just mozzarella in a different shape.” Stringability depends on hitting a narrow process window.

Key insight: Individually wrapped sticks are packaging-intensive; packaging and QA can be the constraint even when bulk mozzarella is plentiful.

Key insight: Refrigerated logistics is a quality and shrink risk, not just a freight line item.

Key insight: Retail and foodservice programs turn small failures into big costs (chargebacks, delists, lost promos).

Modeled % of final delivered cost to your DC (not consumer shelf price). Ranges reflect typical variability across milk markets, packaging formats, and freight lanes.

| Supply Chain Node | Cost Ratio (% of final delivered cost) | Notes |

|---|---|---|

| Upstream milk/components | 45–60% | Main volatility driver; component yield matters. |

| Primary processing (curd make) | 8–12% | Efficiency + yield loss + sanitation. |

| Secondary manufacturing (stretch/form) | 6–10% | Energy + line performance; stringability window. |

| Packaging & QA | 10–18% | Individual wrap film + high-speed line + QA burden. |

| Cold-chain logistics & distribution | 6–12% | Reefer + cold storage + compliance. |

| Supplier margin/overhead | 5–10% | Varies by scale, utilization, and contract terms. |

| Supply Chain Node | Cost Ratio (% of final delivered cost) | Notes |

|---|---|---|

| Upstream milk/components | 50–65% | Higher sensitivity to milk markets. |

| Primary processing | 8–12% | Similar conversion economics. |

| Secondary manufacturing | 6–10% | Similar process control needs. |

| Packaging & QA | 6–12% | Less individual wrap can reduce cost and bottlenecks. |

| Cold-chain logistics & distribution | 6–12% | Similar reefer exposure. |

| Supplier margin/overhead | 4–8% | Often thinner margins in bid-heavy channels. |

| Supply Chain Node | Cost Ratio (% of final delivered cost) | Notes |

|---|---|---|

| Upstream milk/components | 45–60% | Still dominant. |

| Primary processing | 8–12% | Conversion + sanitation. |

| Secondary manufacturing | 6–10% | Texture targets may be tighter. |

| Packaging & QA | 8–16% | Format-specific; may require special packaging. |

| Cold-chain logistics & distribution | 6–12% | Often stricter shelf-life on receipt. |

| Supplier margin/overhead | 5–10% | Depends on customization and service requirements. |

In string cheese, capacity is not just “tons of mozzarella.” It’s:

So a market can look “well supplied” in bulk cheese while sticks are tight because wrapper film, labor, or line uptime is the constraint.

Procurement teams often use bulk cheese or general “dairy” signals to explain stick quotes. That’s directionally helpful, but incomplete.

treat price as three layers:

For market context, USDA AMS publishes regular Dairy Market News reports and price indicators (e.g., cheese blocks/barrels) that are widely used as directional signals, but they are not a direct proxy for packaged string cheese pricing.

Below is how procurement & sourcing management can use intelligence outputs to make better decisions—without pretending we can “guarantee” plant capacity.

What intelligence changes:

Confidence framing:

What intelligence changes:

What intelligence changes:

What intelligence changes:

If you source string cheese, you likely also source other categories where input markets + plant constraints + packaging/cold chain create “price vs availability” surprises:

The transferable lesson: procurement wins when you manage node-specific constraints, not just commodity indices.

Mozzarella string cheese is a high-signal category because it forces disciplined procurement thinking:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.