This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Procurement outcomes for magnesium carbonate rarely hinge on whether the powder exists in the market—they hinge on whether the right grade can be supplied with repeatable process capability and audit-ready documentation at an acceptable total landed cost. This guide translates the magnesium-carbonate supply chain into practical sourcing decisions: how to write specs that keep competition open, where cost volatility actually comes from (and where it doesn’t), and how to build a dual-source posture without overwhelming QA and operations.

(Analyzed at: Apr, 2026)

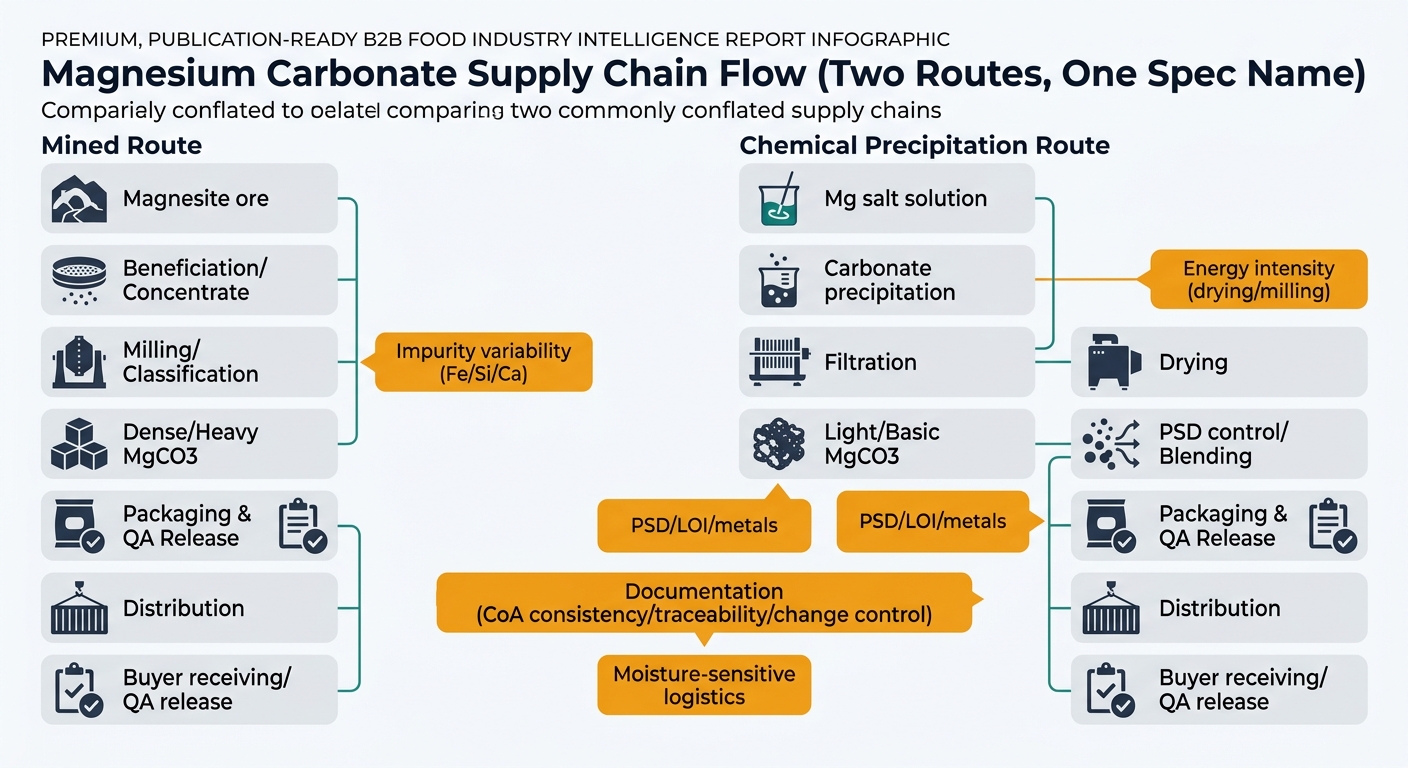

Magnesium carbonate looks like a simple white powder, but procurement outcomes are driven by which production route, which grade, and how tightly controlled the impurity/particle profile is.

Two different supply chains often get lumped together in one spec name:

Why this matters for procurement leadership:

Regulatory anchors that shape the buying spec (not optional in audits):

Practical implication: you’re sourcing a regulated input with a mineral upstream. That combination creates a predictable pattern: quality + documentation are the gating factors, while energy and freight are the volatility multipliers.

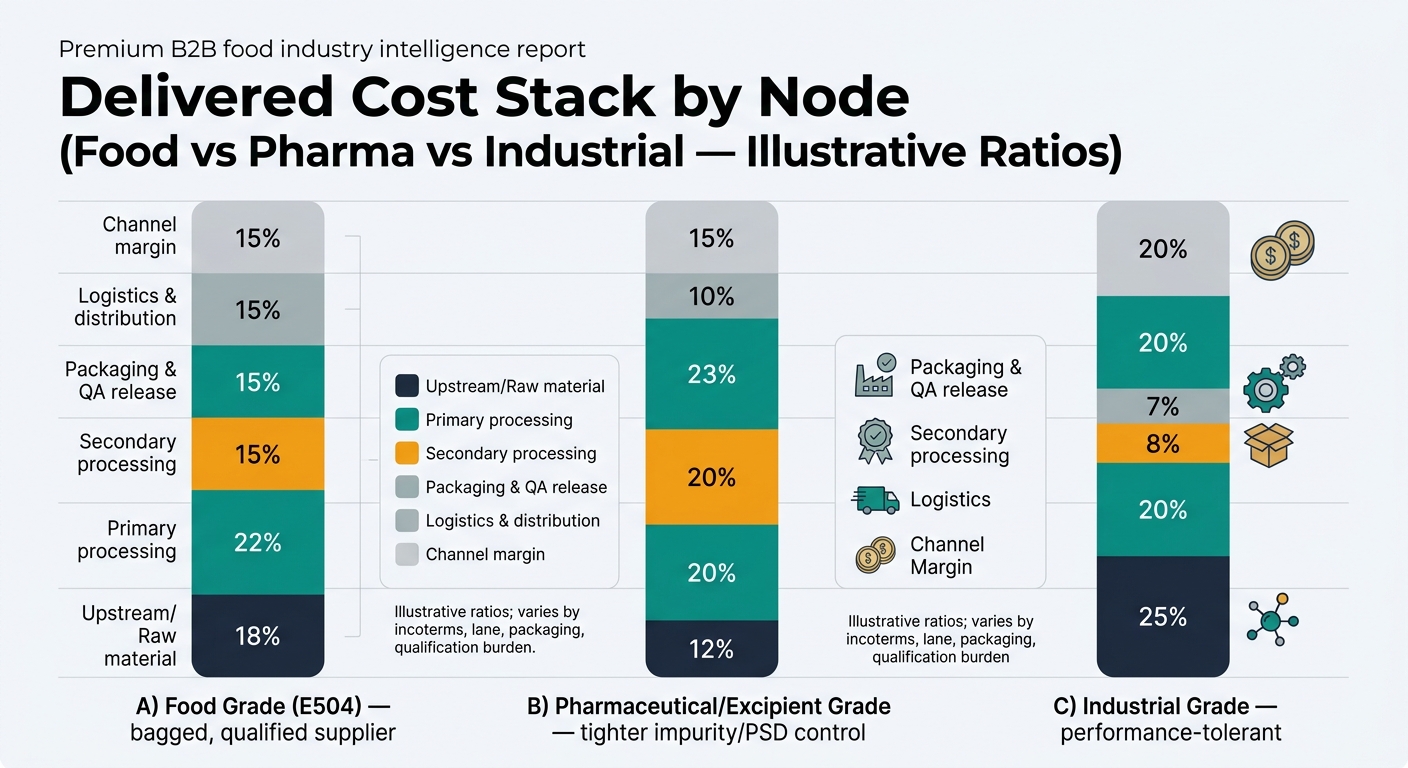

Below is a procurement-oriented view of cost accumulation. The key is not “which node is biggest in theory,” but which node is most likely to spike, fail qualification, or create hidden landed cost.

Key insight: Upstream cost is not just mining; it’s the impurity profile you inherit. Higher Fe/Si/Ca means more beneficiation, more yield loss, and higher probability of off-spec downstream.

What drives cost and risk here

Procurement watch-outs

Key insight: This node is where energy and process yield become the major levers.

Two cost structures depending on route

Procurement watch-outs

Key insight: This is where “commodity powder” becomes “qualified ingredient.” The cost is not only processing; it’s QA capability and the ability to hold tight distributions.

Cost drivers

Procurement watch-outs

Key insight: For food/pharma, packaging and QA release are not overhead; they are qualification enablers.

Cost drivers

Procurement watch-outs

Key insight: MgCO3 is typically non-hazardous, but it is low density and moisture-sensitive, making packaging integrity, container utilization, and warehouse humidity meaningful.

Cost drivers

Key insight: Many buyers pay for “availability and paperwork” via distributors. That’s not wrong—but it must be explicit in your category strategy.

Margin drivers

Modeled % of final delivered cost to a U.S. food manufacturer site. Actuals vary by incoterms, lane, packaging, and qualification burden.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream / Raw material | 18% | Ore or Mg-salt feedstock cost; impurity profile matters more than headline ore price. |

| Primary processing | 22% | Beneficiation or precipitation + drying energy; yield losses. |

| Secondary processing | 15% | PSD control, whiteness, blending/standardization. |

| Packaging & QA release | 15% | Testing + compliant packaging + documentation overhead. |

| Logistics & distribution | 15% | Powder shipping, handling, warehousing, moisture control. |

| Channel margin (importer/distributor) | 15% | Service level + MOQ flexibility + working capital. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream / Raw material | 12% | Feedstock is screened; supplier pays for consistency earlier. |

| Primary processing | 20% | Process control and yield discipline matter. |

| Secondary processing | 20% | Tight PSD/bulk density; higher reject risk. |

| Packaging & QA release | 23% | Higher test burden + batch release discipline + documentation. |

| Logistics & distribution | 10% | More controlled packaging; often higher value density. |

| Channel margin (specialty distributor) | 15% | Qualification support + smaller lots + continuity service. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream / Raw material | 25% | More commodity-like; ore economics show through. |

| Primary processing | 20% | Grinding/classification; energy still matters. |

| Secondary processing | 8% | Less tight PSD/impurity control. |

| Packaging & QA release | 7% | Lower documentation burden. |

| Logistics & distribution | 20% | Low value density makes freight a larger share. |

| Channel margin | 20% | Distribution and availability drive deal structure. |

“Magnesium carbonate” is not one market. It’s a family of grades where qualification friction creates price stickiness.

What this means in practice:

Why that’s structurally true:

Procurement teams often try to time purchases based on upstream mineral or freight headlines. For magnesium carbonate, the delivered price can disconnect for four reasons:

Decision implication: the best timing decisions are usually made using a blend of cost-driver intelligence (energy/freight), supplier capacity signals, and lead-time distributions, not ore price alone.

Outcome: savings erased by:

This section maps procurement decisions to intelligence capabilities—without pretending intelligence guarantees supply or pricing.

Use: Supplier discovery & longlist building

Use: Supplier benchmarking & qualification support

Use: Price intelligence & trend analysis

Use: Supply chain risk monitoring & early warning

Use: Procurement performance & governance analytics

Owner: Category manager + QA lead

Cadence: Quarterly

Steps:

Outcomes + trade-offs:

Owner: Procurement + Finance

Cadence: Monthly driver review; semiannual contracting

Steps:

Outcomes + trade-offs:

Owner: Supplier quality + procurement operations

Cadence: Monthly scorecard; quarterly business review

Steps:

Outcomes + trade-offs:

Magnesium carbonate is a clean example of a broader procurement pattern: mineral/chemical inputs where qualification friction dominates the commercial outcome.

Comparable categories procurement teams often manage:

In all of these, intelligence improves results by:

This category is powerful because it combines:

For procurement leadership, that means improvements are measurable in four KPI families:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.