This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Lavender oil sourcing looks straightforward until you run into (1) seasonal supply windows, (2) chemistry-driven specs that shrink your supplier pool, and (3) authenticity risk that turns “cheap” into TCO pain. This guide is written for Procurement & Sourcing Management teams who are experienced buyers but newer to lavender oil. It explains where cost and risk truly form in the chain, how supplier tiers (distiller vs blender vs distributor) change outcomes, and what measurable KPIs to use to keep supply stable without overpaying.

(Analyzed at: Apr, 2026)

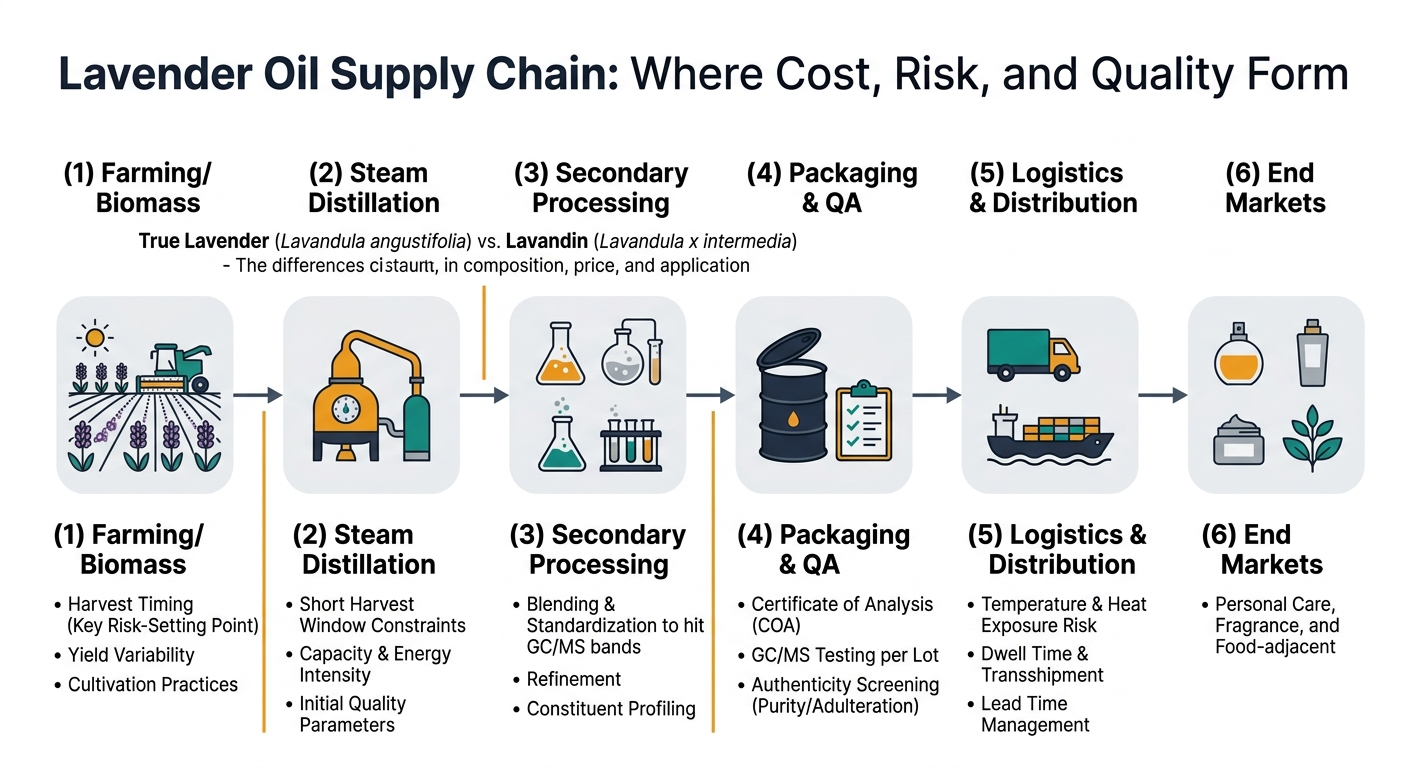

Lavender oil looks like a simple agricultural ingredient, but procurement outcomes are usually decided upstream—in the 2–6 weeks around harvest and distillation—and then “locked in” downstream through blending, documentation quality, and inventory strategy.

Ground-truth flow (typical B2B ingredient path):

Two procurement realities that matter immediately:

Below is how cost typically builds through the chain, and what procurement can actually influence.

Key insight: Lavender oil is a low-yield output of a bulky, time-sensitive input. When yields swing, unit costs swing—even if labor rates are stable.

Useful benchmark (directional, true lavender): Fresh lavender flowers are often cited around ~0.7%–1.4% volatile oil, which is why crop outcomes translate quickly into price signals. [1]

Key insight: Distillation is a capacity-constrained conversion step during a narrow window. If a region has biomass but not enough still time, oil availability tightens.

Key insight: Many buyers assume lavender oil is a single-origin, single-lot commodity. In practice, meeting a tight GC/MS window often requires blending across lots.

Spec anchor (true lavender): ISO 3515:2002 is commonly referenced for Lavandula angustifolia oil; many procurement specs use linalool/linalyl acetate/camphor bands as practical anchors (exact ranges can vary by standard and interpretation, and some ISO standards define multiple characteristics beyond just these three). [3]

Lavandin contrast (more defensible numeric benchmark): ISO 8902:2009 (lavandin, Grosso French type) is commonly summarized with camphor around 6.0%–8.5% (and linalool and linalyl acetate in the mid-20s to 30s). This is why lavandin can be acceptable for detergents/industrial perfumery but problematic for “fine lavender” expectations. [2]

Key insight: Lavender oil has persistent authenticity/adulteration exposure; the procurement lever is not “trust,” it’s test design + documentation completeness.

Industry literature describes using composition patterns and diagnostic markers to flag inauthentic oils against ISO/pharmacopoeia expectations. [1]

Key insight: Logistics cost is not just freight—it’s quality preservation + lead-time reliability.

Many essential oils are shipped under “extracts” classifications in dangerous goods frameworks depending on flash point and composition; industry guidance notes consolidation around UN1197 with a transition period where UN1169/UN1197 were both used (timing depends on regulation edition and mode). Treat this as mode- and lane-specific and confirm with your SDS and forwarder. [4]

Key insight: Downstream margins often price in inventory risk, QA burden, and claims risk, not just handling.

Modeled % allocations to show where costs concentrate. Actual ratios vary by origin, supplier tier (distiller vs blender vs distributor), contract structure, and testing requirements.

| Supply Chain Node | Cost Ratio (% of Final Delivered Cost) | What typically drives variance |

|---|---|---|

| Farming / biomass | 30% | Yield swings, harvest labor, replant cycles |

| Primary processing (distillation) | 22% | Energy, still capacity, harvest congestion |

| Secondary processing (blending/standardization) | 15% | Tight GC/MS targets, blending losses, working capital |

| Packaging & QA | 12% | GC/MS per lot, authenticity screening, drum/liner quality |

| Logistics & distribution | 11% | Freight + dwell time + carrier constraints |

| Supplier/distributor margin | 10% | Inventory risk transfer, service level, credit terms |

| Supply Chain Node | Cost Ratio (% of Final Delivered Cost) | What typically drives variance |

|---|---|---|

| Farming / biomass | 25% | Higher yield potential reduces relative share |

| Primary processing (distillation) | 20% | Energy and throughput |

| Secondary processing (blending/standardization) | 10% | Broader spec = less blending constraint |

| Packaging & QA | 8% | Lighter testing burden in some channels |

| Logistics & distribution | 12% | Similar handling needs |

| Supplier/distributor margin | 25% | Trading/blending channels often dominate value capture |

| Supply Chain Node | Cost Ratio (% of Final Delivered Cost) | What typically drives variance |

|---|---|---|

| Farming / biomass | 20% | Multi-origin flexibility dampens shocks |

| Primary processing (distillation) | 18% | Origin mix changes cost base |

| Secondary processing (blending/standardization) | 22% | The product is the blending capability |

| Packaging & QA | 15% | Trend monitoring across inputs |

| Logistics & distribution | 10% | Inventory positioning |

| Supplier/distributor margin | 15% | Formulation and reliability premium |

These ratios are plausible as a teaching tool, but they are not “industry averages.” Use them to guide which levers to interrogate in an RFQ (yield/energy/blending/testing/inventory), not as a should-cost model.

Lavender oil is produced in a seasonal window (often late spring/summer depending on origin), but consumption is steady. That creates a structural pattern:

Procurement takeaway: your contracting and inventory decisions must be synchronized to pre-harvest, harvest, and post-harvest phases—not just quarterly budgeting.

When procurement sees two quotes that don’t move together, it’s usually not supplier opportunism—it’s a mismatch in what’s being priced.

Four common disconnect mechanisms:

From a Procurement & Sourcing Management perspective, these are the repeat failure modes:

KPIs that expose these problems early:

This is not about “finding suppliers.” It’s about reducing avoidable surprises by aligning market reality, supplier capability, and your spec.

Instead of a flat supplier list, segment the market into:

Compare suppliers on procurement-relevant signals:

Track price drivers that actually move lavender oil economics:

A “real” dual-source plan includes:

Measurable outcomes:

Make trade-offs explicit:

KPI targets: fewer escalations; fewer reformulation-driven expedites

If you source lavender oil, you likely source other ingredients with the same structural dynamics:

The transferable lesson: procurement performance improves when you manage spec + supplier tier + seasonality + authenticity risk as one system.

Lavender oil is an unusually clear case where:

If you can build a sourcing strategy that holds cost, OTIF, and nonconformance stable in lavender oil, you can replicate the same governance model across a broader botanical and natural-ingredient portfolio.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.