This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Peak-season hot chocolate sourcing fails in predictable ways: not because “cocoa disappears,” but because spec-locked cocoa powders, low-moisture food safety controls, and packaging/line capacity constraints collide with Q4 demand. This guide translates those upstream realities into procurement actions (dual-source readiness, spec-flex guardrails, trigger-based contracting) and the KPIs leaders actually manage: OTIF, time-to-switch, expedite spend, and price variance vs a defensible should-cost.

(Analyzed at: Apr, 2026)

Instant hot chocolate powder looks like a simple dry mix. In reality, it’s a multi-node, multi-risk system where the biggest disruptions rarely come from “no cocoa available” and more often come from:

Procurement implication: your “supplier” is usually managing a network of cocoa processors, dairy ingredient suppliers, film converters, and co-pack capacity. If you only manage the finished-goods PO, you’re managing the least informative part of the risk picture.

For instant hot chocolate powder, cocoa is the volatility engine, but pack format + quality gates often decide whether you can switch suppliers quickly without breaking service levels.

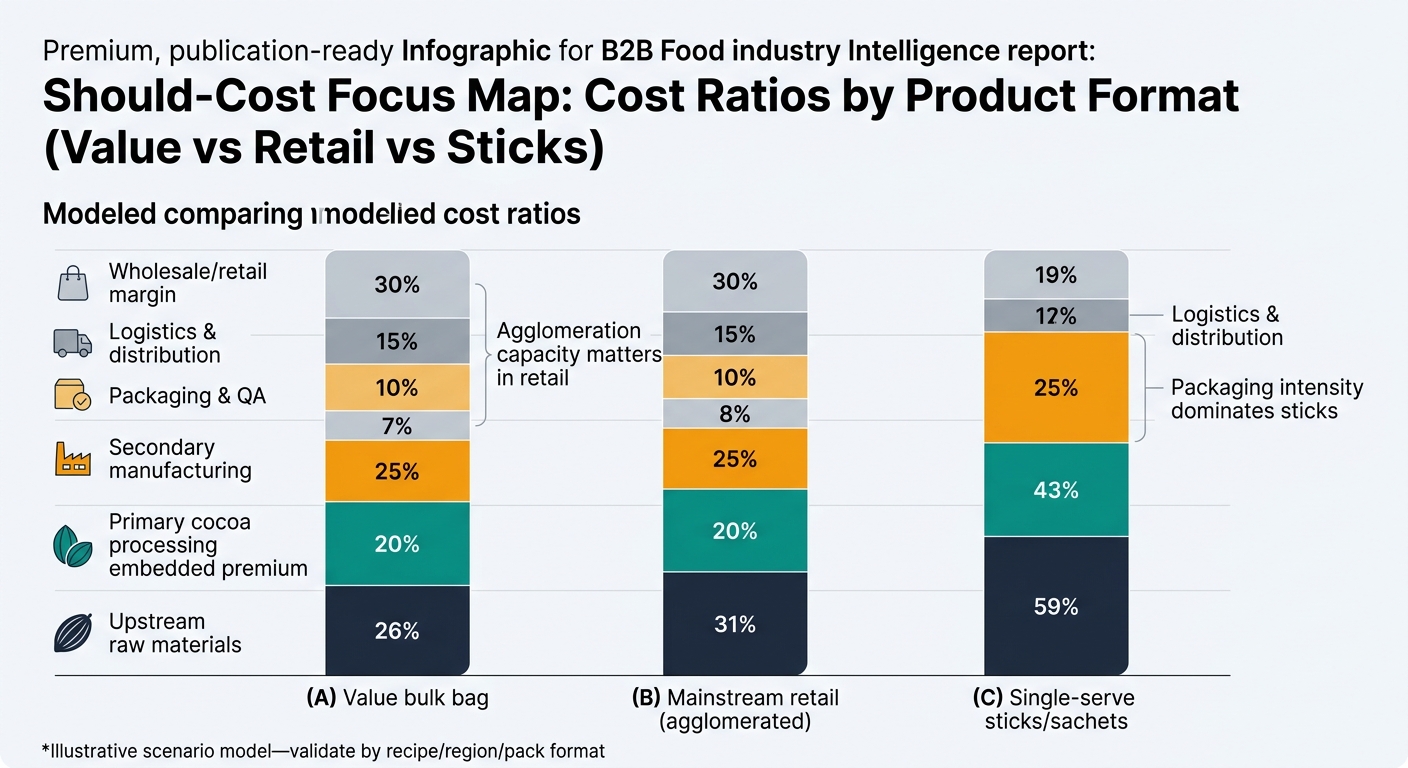

These are decision-model ratios to help procurement focus effort. Actual ratios vary by recipe (value vs premium), cocoa %, dairy inclusion, pack format, and region.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream raw materials | 55% | Sugar dominates weight; cocoa still drives volatility per kg. |

| Primary cocoa processing embedded premium | 10% | Cocoa powder spec premiums. |

| Secondary manufacturing | 12% | Blending + basic QA. |

| Packaging & QA | 6% | Bulk bags; lower print complexity. |

| Logistics & distribution | 7% | Regional freight + warehousing. |

| Wholesale/retail margin | 10% | Channel dependent. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream raw materials | 45% | Cocoa + dairy/creamer become more material. |

| Primary cocoa processing embedded premium | 12% | Alkalization/color consistency premiums. |

| Secondary manufacturing | 15% | Agglomeration/instantization capacity + yields. |

| Packaging & QA | 12% | Barrier packaging + labeling + more testing. |

| Logistics & distribution | 6% | Mostly regional; humidity controls matter. |

| Wholesale/retail margin | 10% | Retail margin + distributor. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream raw materials | 35% | Same ingredients, but diluted by pack cost. |

| Primary cocoa processing embedded premium | 10% | Cocoa spec still matters for taste/appearance. |

| Secondary manufacturing | 14% | Stick-pack line efficiency + changeovers. |

| Packaging & QA | 25% | Printed film, rollstock, scrap, coding, QA. |

| Logistics & distribution | 6% | Higher cube inefficiency. |

| Wholesale/retail margin | 10% | Channel dependent. |

Low-moisture foods don’t support pathogen growth well, but Salmonella can persist and outbreaks can still occur—often linked to environmental contamination and inadequate sanitation controls [5].

Procurement implication: supplier qualification must include low-moisture sanitation design, environmental monitoring maturity, and corrective-action discipline, not just “they have a GFSI certificate.”

Cocoa processing yields multiple co-products (butter and powder/press cake). As a result:

Practical sourcing takeaway: negotiate using a cost-driver decomposition (cocoa powder index proxy + sugar + dairy + packaging + freight + conversion), not last price paid.

You typically have three levers:

Here’s how intelligence changes those decisions:

The same “multi-node constraint + hidden risk + spec lock” pattern shows up in:

In all of these, teams win by:

Instant hot chocolate powder is a compact case study because it forces you to manage all three realities at once:

If your organization can run a disciplined, intelligence-led sourcing cycle here—dual-source readiness, spec-flex boundaries, and trigger-based contracting—you can replicate the same governance model across other dry, shelf-stable categories where the biggest risks are hidden upstream.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.