This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

(Analyzed at: Apr, 2026)

Ready to act on these insights? Tridge Eye delivers the real-time market signals behind this analysis. Get my market intelligence →

Winged-bean flour behaves less like a traded commodity and more like a capacity-and-inventory priced specialty ingredient. The “alpha” comes from tracking the spread between (a) upstream seed availability and (b) downstream flour offers—then acting before that spread mean-reverts.

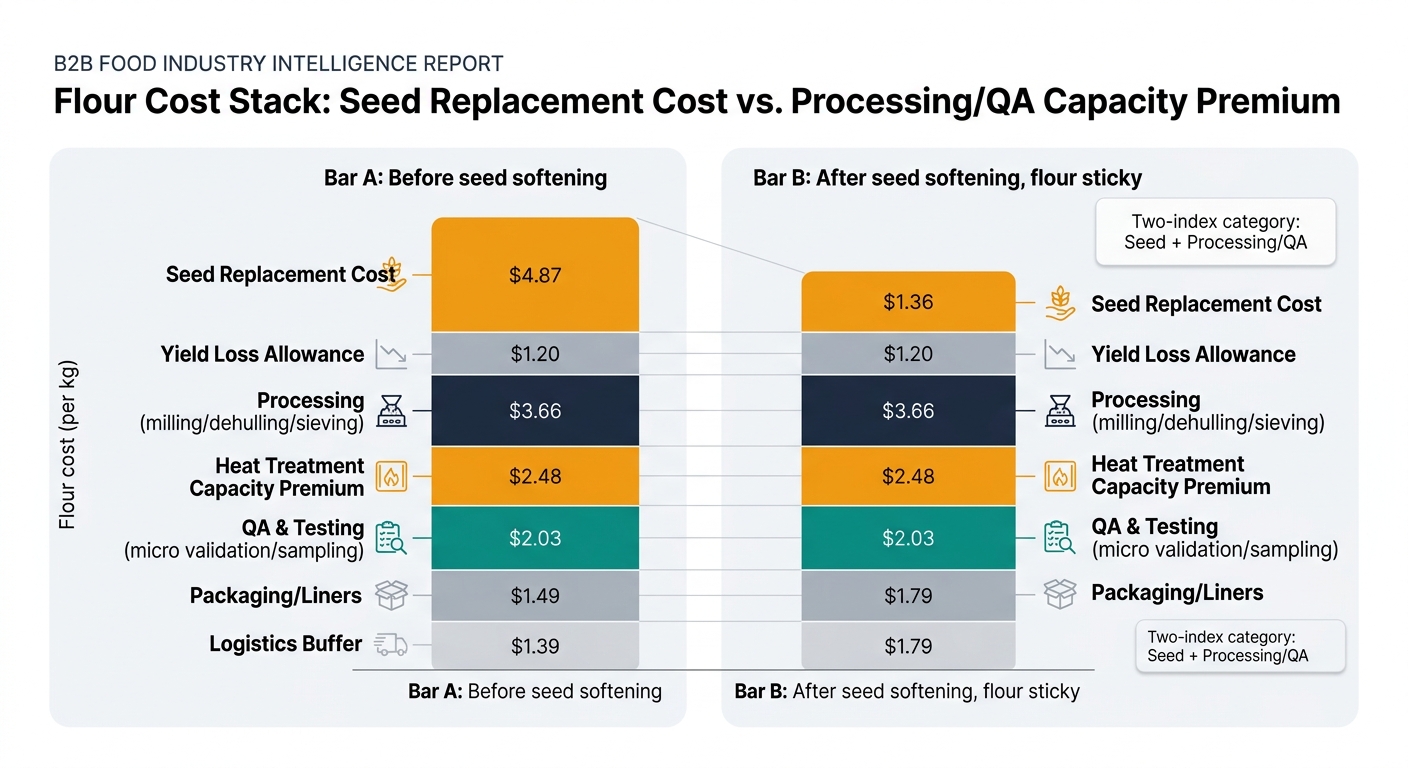

Treat winged-bean flour as a two-index category: (1) seed availability proxy + (2) processing/QA capacity proxy. When those diverge, you can renegotiate, re-time purchases, or trigger dual-sourcing before competitors do.

Insight: Winged-bean flour pricing often decouples from seed pricing because processing yield, capacity, and risk buffers dominate the last 30–60 days of the cost stack.

Quick win: For each supplier, document a Process-Equivalent Profile (dehulled/whole, heat-treated/untreated, target particle size, typical micro performance). Use that to define true alternates.

Insight: The measurable advantage comes from turning winged-bean flour into a governed, signal-based category—not a relationship-based specialty buy.

| Dimension | Traditional (quote-led) | Intelligence-driven (signal-led) | What improves |

|---|---|---|---|

| Price variance vs. market-clearing level | +6% to +15% on portions of spend | +2% to +6% | Better timing + leverage from alternates |

| Unplanned disruption events | 1–3/year | 0–1/year | Early triggers + qualification-ready bench |

| Qualification cycle time for alternates | 12–20 weeks | 6–12 weeks | Pre-built data pack + aligned spec ranges |

| Quality incidents (holds/claims) | Higher, sporadic | Lower, trend-managed | Lot history + process comparability |

Insight: If seed availability is improving but flour offers are sticky, you’re likely seeing inventory lag.

Insight: Moisture drift can be origin-seasonal, not supplier-specific.

Insight: Capacity capture shows up as longer lead times before price spikes.

Insight: Winged-bean flour is a template for other “thin market” plant ingredients where processing and QA dominate.

Similar disconnect patterns show up in:

Build a repeatable method: input proxy + processing proxy + qualification readiness.

Winged-bean flour exposes a common procurement trap: when markets are thin, your biggest savings and risk reduction come from timing and optionality, not from squeezing a single supplier.

If you can’t answer—quantitatively—(1) how much of today’s offer is seed vs. processing vs. logistics, (2) how long supplier inventory cycles are, and (3) which alternates are truly process-equivalent, you’ll keep paying “uncertainty premiums” during perfectly predictable spread events.

Logical next step framing: the hard problem isn’t negotiating; it’s maintaining a living view of spreads, capacity constraints, and qualification status so you can act before the market forces your hand.

Start Making These Sourcing Decisions with Live Signals

Tridge Eye — The strategy playbook above works — but only with current data feeding it. Real-time price movements, supplier risk scores, and origin alerts turn these frameworks into daily competitive advantages.