Zucchini-puree is a deceptively “simple” ingredient: the raw vegetable is seasonal and weather-sensitive, but the puree price you get quoted is shaped just as much by processor pack windows, packaging availability, and cold-chain logistics. This guide translates those mechanics into negotiation moves and governance habits a procurement leader can operationalize—without needing to be a zucchini category specialist.

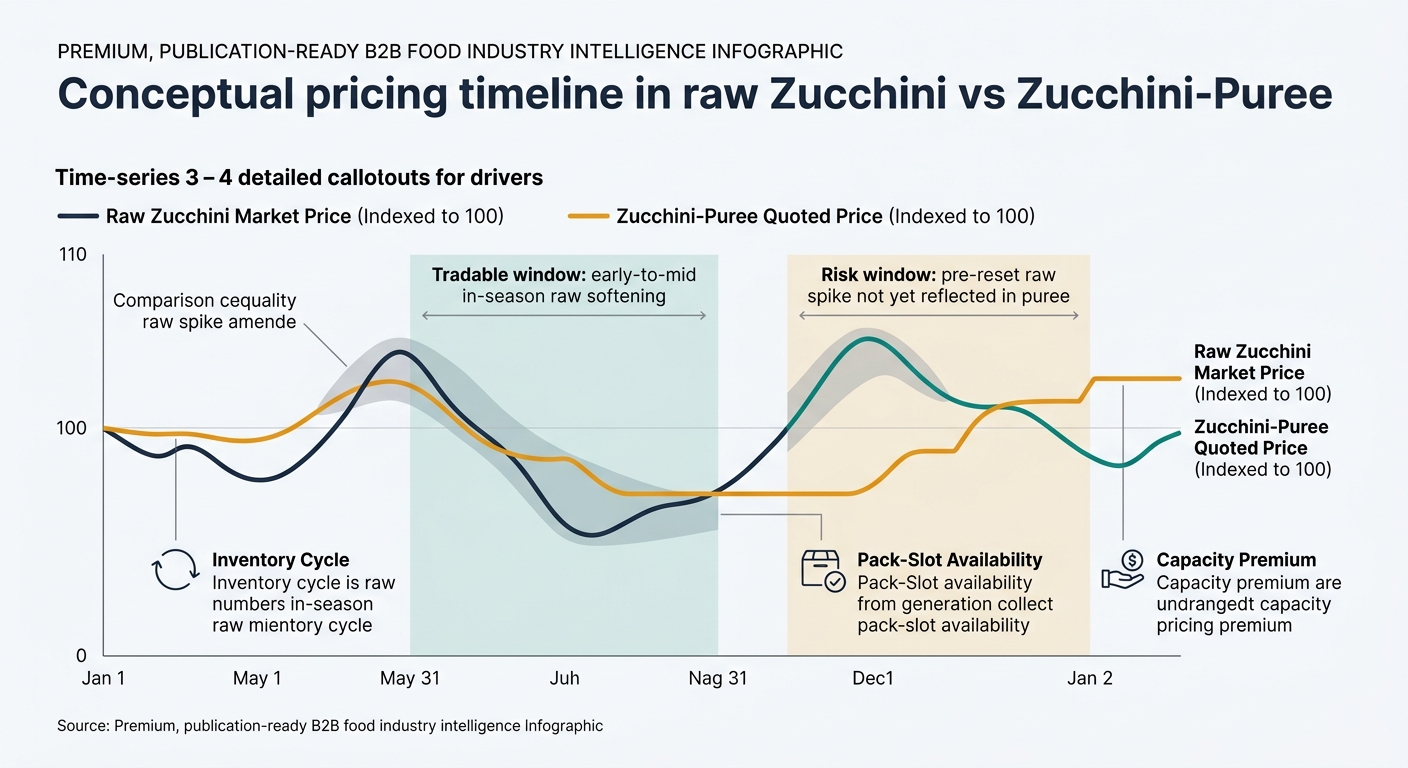

Zucchini-puree pricing often looks irrational to procurement teams because the raw input market and the processed-puree market don’t clear on the same clock. Your leverage comes from understanding when the processor’s cost base actually changes—and when they’re still selling yesterday’s cost in today’s market.

Quick Win: In your next supplier call, ask for a two-line cost narrative: “What changed in raw zucchini vs. what changed in conversion/packaging?” If they can’t articulate both, you’re negotiating in the dark.

Quick Win: Run a quarterly “switchability” test: can you move 20–30% volume to an alternate within 30–45 days without waivers? If not, you don’t have a backup—you have a hope.

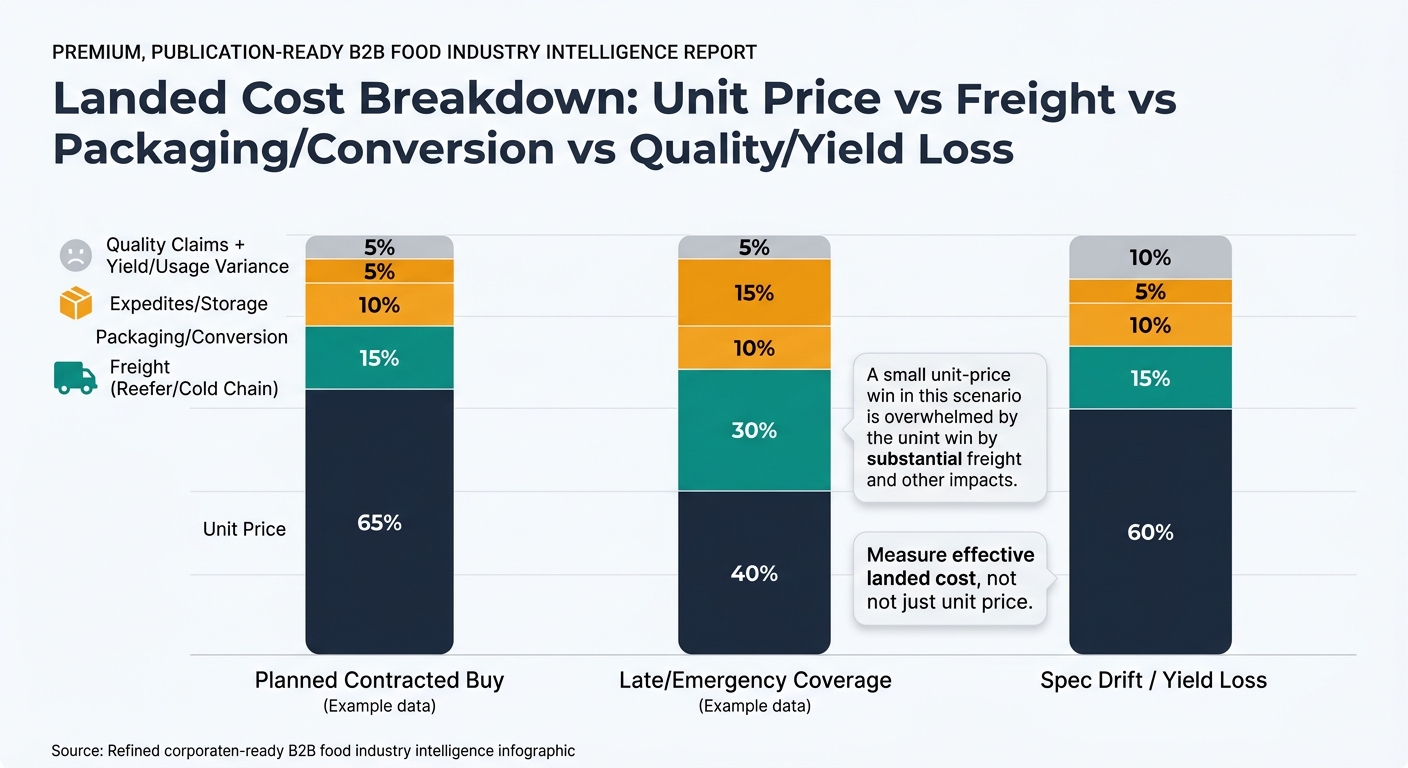

Quick Win: Stop measuring success as “unit price vs last year.” Measure effective landed cost: unit price + freight + quality claims + usage/yield variance + expediting.

Quick Win: Pre-align Ops/QA on one “contingency format” that can be activated without a full reformulation cycle.

Quick Win: Use one template for (1) reset mechanics, (2) lead time/MOQ benchmarks, and (3) contingency supplier qualification across all processed-veg ingredients.

Quick Win: If you can’t defend why a price moved in one sentence (raw vs conversion vs capacity), you’re not ready to lock volume.

In your next negotiation cycle, push for a short-reset, symmetric pricing mechanism (step-ups and step-downs) and explicitly model freight as a first-class cost driver—not an afterthought. (Analyzed at: Apr, 2026) 2026 refrigerated freight has shown a firmer floor than 2025, which increases the penalty for “wait-and-see” buying and emergency coverage. [1] Pair that with the predictable lag between raw-market tightness (often weather-driven in key supply regions) and processor repricing, and you have a narrow window to lock coverage before resets hit. [2] If you move late, the cost shows up less as a dramatic unit-price increase and more as an all-in landed-cost hit—expedites, storage, and avoidable yield loss that can easily erase a low-single-digit “negotiated” gain.