Zucchini-puree looks like a simple processed-vegetable buy until you get hit by the two things that actually drive outcomes: (1) when processors choose to run campaigns and allocate line time, and (2) whether your format/pack/spec choices trap you in a single production lane. This guide shows how to spot the real leverage windows, avoid the common “quiet cost” mistakes, and build a dual-source posture that works in practice.

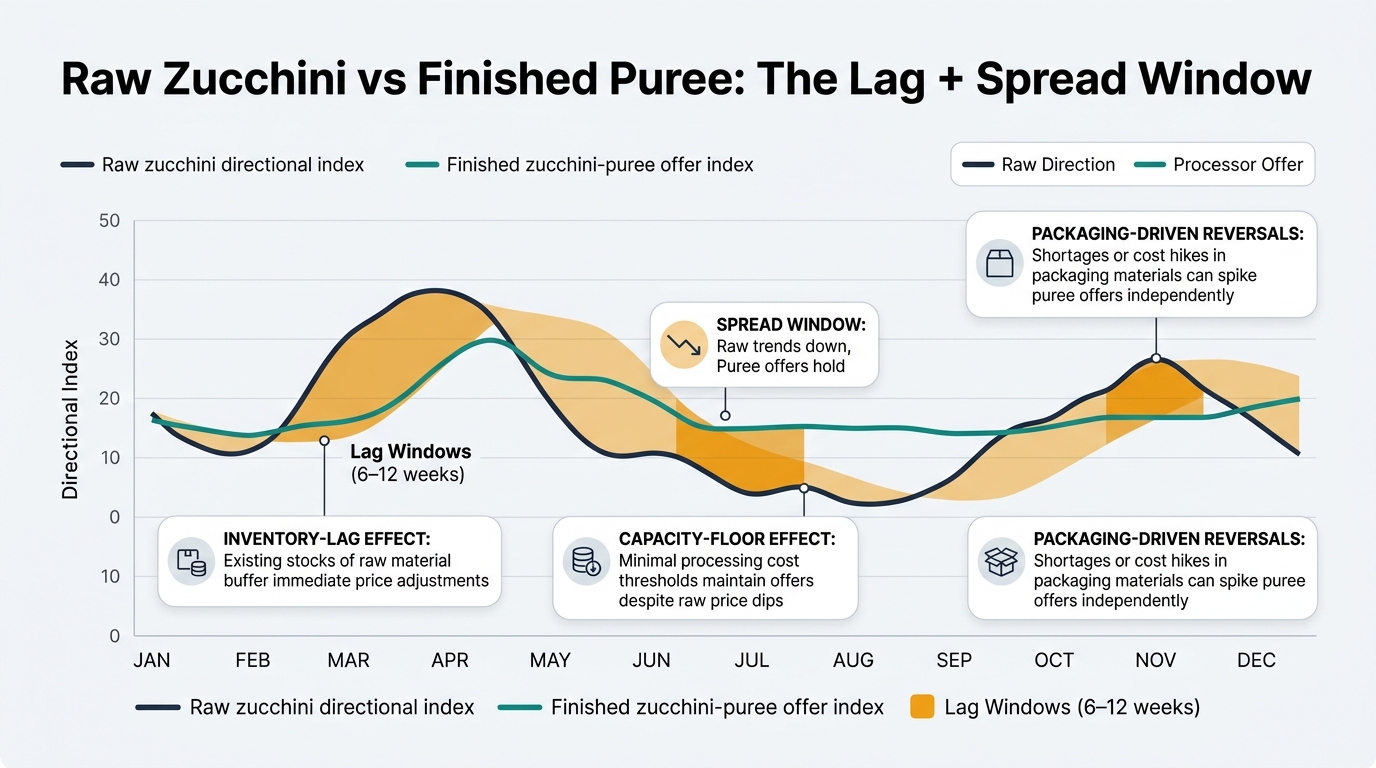

Zucchini-puree prices often don’t follow fresh zucchini prices in the same month—sometimes not even in the same quarter—because puree is priced off processing capacity, packaging availability, and inventory carry, not just farmgate.

The most common disconnect patterns procurement teams see:

If you negotiate zucchini-puree purely off “what zucchini is doing,” you’ll miss the real leverage windows. The exploitable edge is tracking the spread between (a) raw zucchini direction and (b) processor capacity + packaging constraints. When the spread widens, you either (1) push for a pass-through reset if you’re buying from inventory, or (2) shift volume/format/pack to where the bottleneck isn’t.

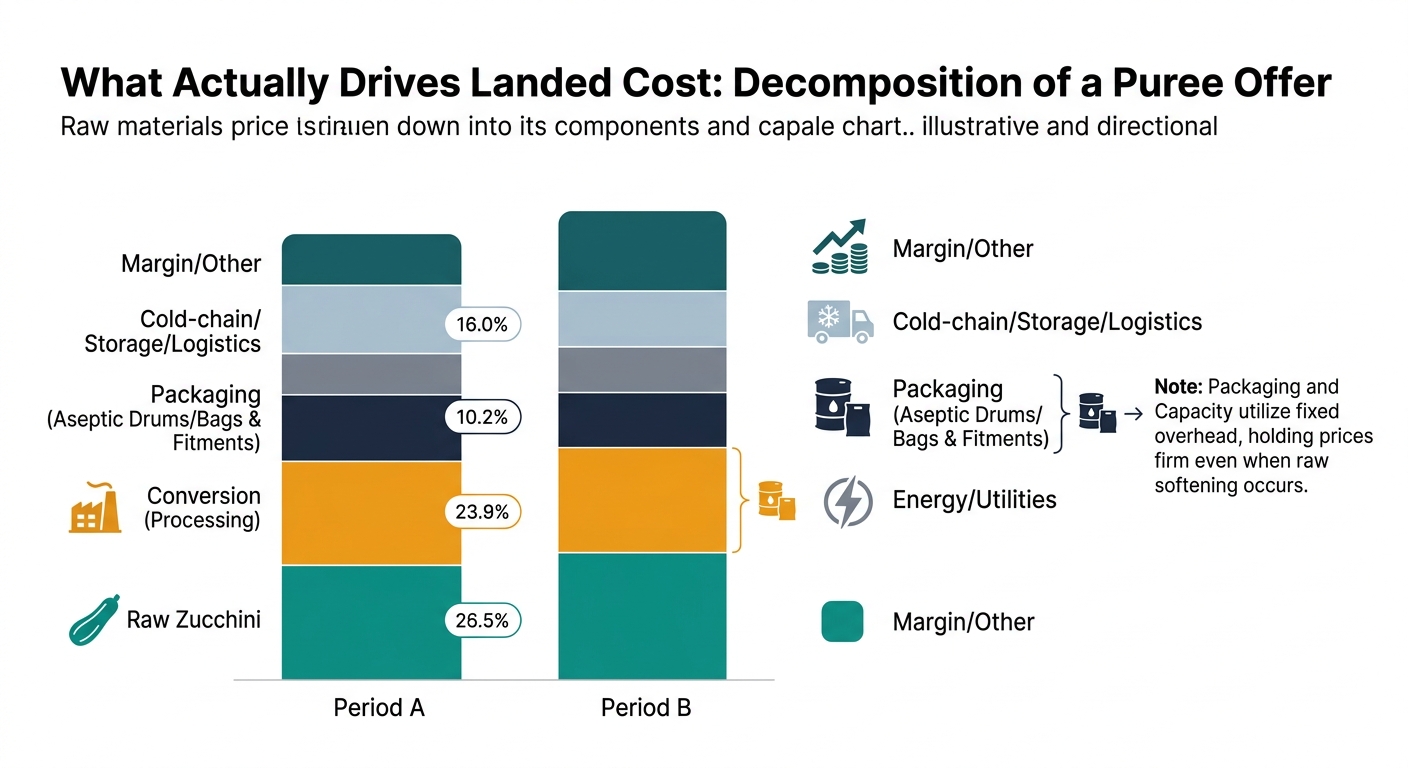

In your next supplier call, ask for a two-line decomposition: “What % of this move is raw zucchini vs packaging vs conversion?” If a supplier can’t explain the move, you’re negotiating blind.

Most zucchini-puree “overpay” isn’t a bad negotiation—it’s a portfolio and specification problem that forces you into the supplier’s least flexible production lane.

These are the repeatable failure modes.

These mistakes convert a negotiable category into a take-it-or-leave-it buy. Fixing them usually delivers more savings than another round of “3 quotes and a squeeze,” because it restores optionality.

For each supplier, document one sentence: “What exact lane are we buying?” (format + pack + production window). If you can’t write it, you don’t have leverage.

Intelligence-driven procurement doesn’t mean more data; it means fewer surprises and tighter control of the 2–3 variables that actually move your outcome: capacity access, format optionality, and spec-fit risk.

A realistic before/after for a mid-sized North American buyer (mixed prepared foods + foodservice) is less about “perfect price calls” and more about reducing the frequency and severity of bad outcomes.

The biggest gain is governance: you can explain why you awarded volume, what triggers a reallocation, and how you’ll protect service levels when the market tightens.

Add one KPI to your quarterly review: “% of volume that can switch suppliers within 30 days without spec change.” If it’s under ~30–40%, you’re effectively single-sourced.

Zucchini-puree problems are usually timing problems disguised as price problems.

Use these scenario playbooks.

Put a “format switch” option into the contract (e.g., drums ↔ bag-in-box) with pre-priced conversion adder/deduct. That single clause can protect supply when one packaging lane tightens.

Zucchini-puree is a clean example of a broader truth: processed produce pricing is often a function of conversion constraints and packaging, not just farmgate.

Similar dynamics show up in:

If you build a repeatable “spread + bottleneck” method here, you can port it across your processed vegetable basket and stop re-learning the same lesson category by category.

Standardize a one-page template across vegetable ingredients: raw signal, conversion constraint, packaging constraint, and inventory lag. Use it as the agenda for every supplier review.

The real advantage isn’t predicting the market perfectly—it’s making your decisions defensible, earlier, and less dependent on one supplier’s narrative.

In zucchini-puree, the “truth” sits in three places procurement rarely triangulates in one view: (1) raw zucchini direction, (2) processing-slot tightness, and (3) packaging lane availability. When you only see one, you mis-time renewals, over-index on spot quotes, and confuse short-term supply tightness with long-term structural shortage.

A sourcing review that explicitly separates those drivers produces faster alignment with QA/Ops/Finance: you can justify when to lock, when to stay short, and when to pay for resilience—without arguing from anecdotes.

In your next QBR, require suppliers to answer one question: “If raw zucchini drops 10% next month, what would prevent you from passing it through?” Their answer reveals your real constraints.

Treat today’s raw-to-puree spread as your negotiation clock: when raw signals have softened but puree offers haven’t, you have a short window to reset pricing or re-structure terms before the next campaign reprices the market.

In spread windows, the achievable outcome is usually not a dramatic list-price cut—it’s a better deal structure: shorter fixed periods, step-down triggers, and format/pack flexibility that expands your supplier bench.

Teams that act during the spread window typically capture 2–5% better total landed cost and avoid the spot-buy penalty that shows up when capacity tightens and packaging lanes become the real constraint.

(Analyzed at: Apr, 2026)

If you’re renewing zucchini-puree in the next 60–120 days, treat format optionality as the fastest, most bankable de-risk lever in 2026—not because zucchini is “rare,” but because processors still price and allocate around line time and packaging lanes, while cold-chain costs can re-tighten quickly in seasonal peaks. California zucchini availability typically runs late spring through early fall with summer peak, so the buyers who secure campaign allocation now—and add a pre-priced drums↔bag-in-box (or frozen↔aseptic) switch—tend to avoid the expensive failure mode: shorted deliveries that force spot coverage. In practice, that’s often the difference between a manageable 2–5% landed-cost improvement versus giving it back through expedites and disruption-driven buys.