Grapefruit-juice-concentrate (GJC) looks like a simple ingredient line item until you try to compare two quotes and realize you’re really buying a bundle of yield, thermal handling, aroma management, and preservation discipline. This guide maps the real physical flow and pinpoints where cost and risk “lock in,” so procurement teams can negotiate and contract on comparable, auditable terms.

Grapefruit-juice-concentrate (GJC) is not a single-step commodity; it is a chain of short-lived fruit, energy-intensive concentration, and cold/sterile handling that locks in cost early and then protects value through storage and logistics. The “fixed” cost-drivers are structural: harvest timing, extraction yield, evaporation energy, packaging sterility, and cold-chain discipline.

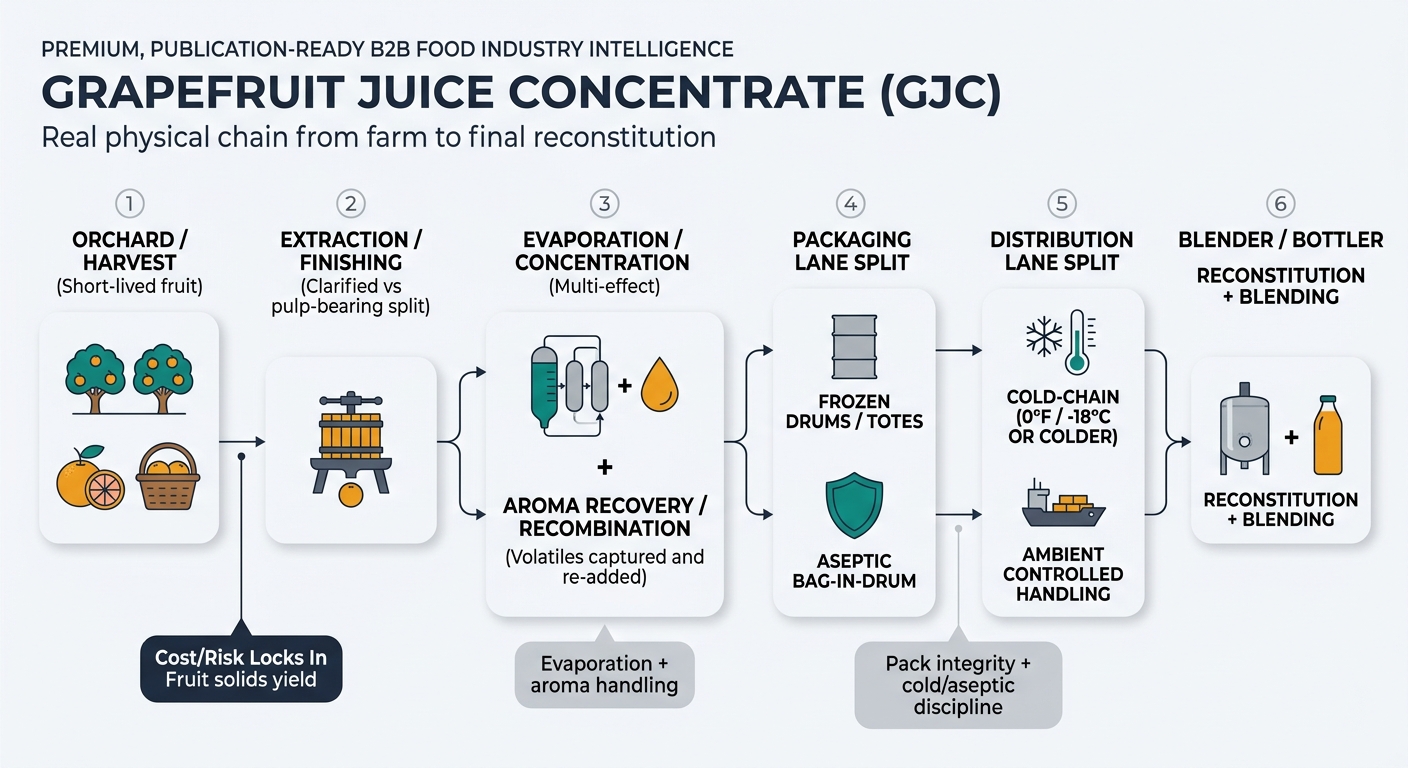

Insight: The product’s economic value is created by removing water (concentration) and preserving flavor/aroma while keeping microbiology under control.

Data (validated): Industrial grapefruit concentrate is commonly sold in a high-solids range (often ~58–65° Brix, depending on grade/spec and clarified vs pulp-bearing). Frozen programs commonly specify storage/transport around 0°F / -18°C (or colder) to protect quality [1][2].

Procurement Impact: Your cost base is physically anchored at three choke points—fruit solids yield, evaporation/aroma recovery, and pack + cold/aseptic integrity—so any comparison of suppliers or quotes only makes sense once these nodes are understood.

Insight: Costs accumulate less from “trading” and more from physics: yield losses, heat transfer, sterility, and temperature control.

Data (validated): Multi-effect evaporation is a common industrial approach for concentrating juice; during evaporation, volatile aroma compounds can transfer to the vapor phase and typically require recovery and re-addition to avoid flavor impairment [3].

Procurement Impact: Even without discussing buying strategy, a buyer can predict where suppliers will differ structurally: (1) orchard solids, (2) plant technology/energy, (3) packaging format and cold-chain/aseptic capability.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw Material Cost (fruit) | 45% | Driven by fruit price and juice-solids yield; highest structural lever. |

| Primary Processing | 10% | Extraction/finishing, filtration aids (as applicable), waste handling. |

| Secondary Processing | 18% | Evaporation energy + aroma recovery/recombination capability. |

| Packaging & QA | 7% | Frozen drums/totes, sampling, micro/chem testing, documentation. |

| Logistics & Distribution | 12% | Reefer transport + cold storage + port handling; sensitive to delays. |

| Processor/Distributor Margin | 8% | Varies by integration level and services (blending, documentation). |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Raw Material Cost (fruit) | 45% | Similar fruit economics; may differ by target spec and solids. |

| Primary Processing | 10% | Clarification/pulp management choices affect downstream usability. |

| Secondary Processing | 16% | Concentration + aroma management; thermal damage avoidance matters. |

| Packaging & QA | 10% | Sterile barrier bags/drums, aseptic filling controls, higher barrier materials [4]. |

| Logistics & Distribution | 11% | Less cold-chain burden than frozen, but still needs controlled handling. |

| Processor/Distributor Margin | 8% | Often includes documentation, traceability, and lot management. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Concentrate Input (as purchased) | 55% | Concentrate dominates; performance depends on reconstitution yield/targets. |

| Reconstitution & Blending | 12% | Water treatment, mixing, filtration, flavor adjustment, in-plant losses. |

| Packaging & QA | 10% | Finished-pack packaging (varies widely by channel). |

| Logistics & Distribution | 13% | Ambient vs chilled distribution economics dominate here. |

| Brand/Channel Margin | 10% | Varies by route-to-market; not a processing physics driver. |

Insight: The biggest “surprises” in GJC are usually not price moves—they are physical constraints that show up as quality failures, delays, or spec disputes.

Data (validated): USDA standards and specifications operationalize quality beyond solids (e.g., Brix/acid ratio and defect/sensory frameworks), reinforcing that acceptance is multi-parameter, not just °Brix [6].

Procurement Impact: If you don’t align internal stakeholders on which physical parameters are critical-to-quality, you will see avoidable rejects, rework, and inconsistent finished flavor.

Insight: Grapefruit juice concentrate is a solids + aroma + preservation system, not a generic liquid ingredient.

Data (validated): Concentration inherently risks aroma stripping; sources describe aroma recovery and recombination as common approaches to protect sensory quality, while industrial packaging frequently relies on either frozen storage expectations or aseptic barrier systems [3][4].

Procurement Impact: When internal teams see variability, the root cause usually traces to one of three physical levers: (1) fruit solids/yield, (2) evaporation/aroma handling, or (3) temperature/sterility discipline from pack-out to receiving.

Key Takeaways: Raw fruit economics dominate the cost base; evaporation/aroma systems differentiate sensory performance; packaging and logistics protect (or destroy) the value you already paid for.

(Analyzed at: Apr, 2026)

Lock your next GJC award around a two-lane spec and governance structure: one lane for frozen at 0°F / -18°C (or colder) with explicit ship/receive temperature evidence, and one lane for aseptic bag-in-drum with defined drum/bag format and post-opening handling rules—then require lot-level COAs that include °Brix and Brix/acid ratio plus a defined sensory reference.

This works because the biggest avoidable cost isn’t the headline $/kg; it’s the downstream spend from aroma drift, bitterness imbalance, and cold-chain/aseptic failures that show up as reblends, holds, and claims. In a 2026 environment where citrus supply remains structurally pressured by disease and weather impacts, teams that pre-qualify an alternate lane (even for 20–30% of volume) typically buy down the risk of emergency spot buys and line disruptions that can easily cost low-to-mid single-digit percentages of annual ingredient spend [2].