This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

Granola looks straightforward on the shelf, but procurement outcomes hinge on a multi-commodity bill of materials plus a surprisingly tight set of operational bottlenecks (co-man line time, allergen changeovers, and packaging lead times). This guide translates that reality into how a Procurement Manager should structure RFQs, dual-source plans, indexation, and supplier governance—so margin protection doesn’t accidentally create continuity or quality risk.

(Analyzed at: Mar, 2026)

Granola looks like a simple dry grocery item, but procurement outcomes are determined by a multi-commodity, multi-risk chain where a few nodes dominate cost and disruption risk.

Below is an analyst-style view of how cost stacks through the chain. The goal is not fake precision—it’s to show where procurement leverage and hidden costs live.

Key insight: Granola is a “portfolio” of commodities. The volatility you feel in finished goods pricing is often inclusions + oils + packaging, not just oats.

Low-moisture foods are not “low risk.” Pathogens can persist in low-moisture foods (LMFs), and nuts/dried fruits are repeatedly implicated in contamination and mycotoxin monitoring and border notifications. For procurement, that translates into supplier approval rigor + incoming controls (COAs, sampling plans, and traceability) as part of the commercial decision—not after the fact. [3]

Key insight: This node is where your written spec turns into manufacturing behavior (bake performance, cluster formation, shelf-life).

Switching a cheaper oat cut size or inclusion grade can create downstream losses:

Key insight: In granola, the “factory slot” is often as valuable as the ingredient price—especially during peak demand windows.

A low tolling rate can be offset by:

Key insight: Packaging is not just “materials”—it is shelf-life protection + retailer compliance.

Humidity ingress → loss of crunch → complaints/returns; heat exposure → oxidation/rancidity claims.

Key insight: Granola is bulky and crush-sensitive. You’re paying for volume (cube) and damage prevention, not refrigeration.

Key insight: For many procurement teams, the biggest “unplanned cost” is not the invoice—it’s chargebacks, expedites, and service recovery.

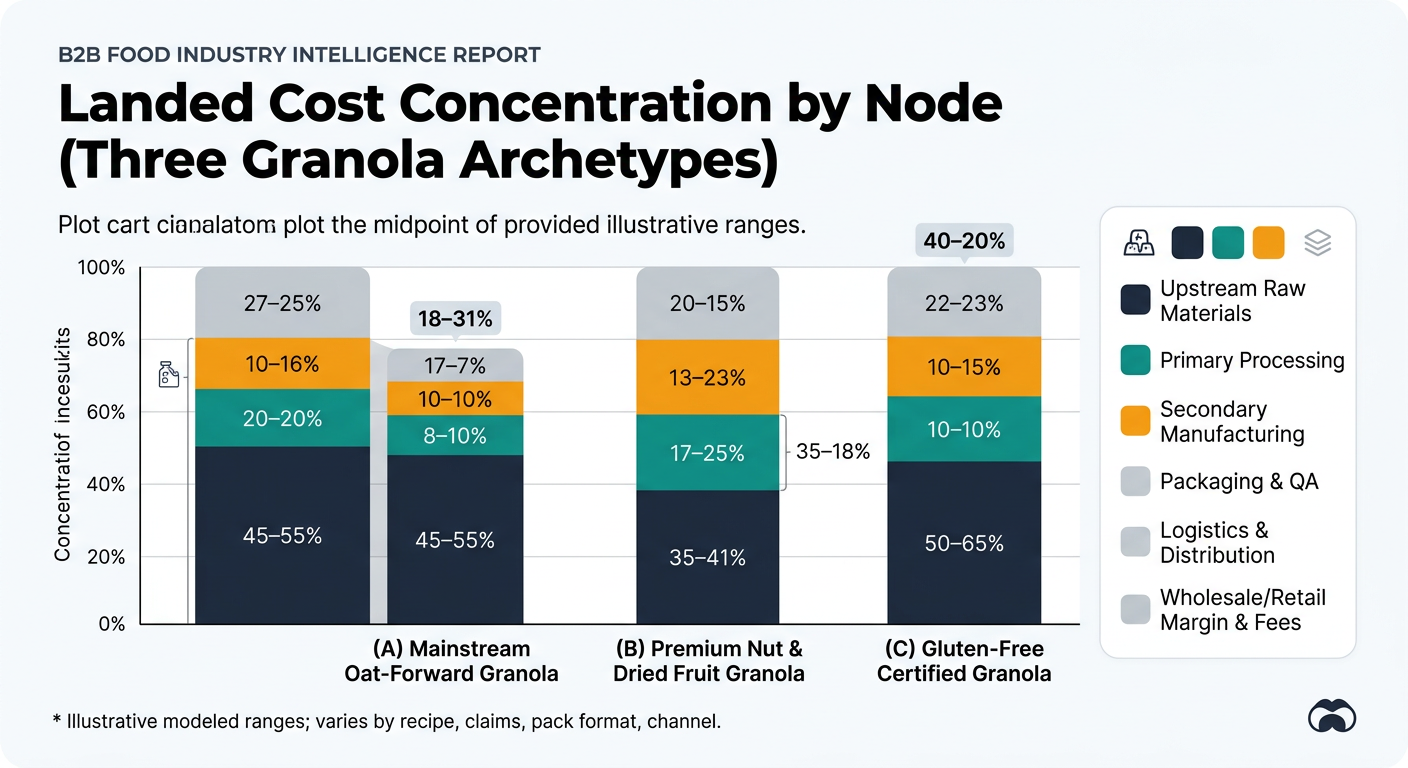

These are modeled ranges to show cost concentration by node. Actual ratios vary by recipe, claims (organic/GF), pack format, and channel.

| Supply Chain Node | Cost Ratio (% of Final Landed Cost) | What moves it most |

|---|---|---|

| Upstream raw materials | 45–55% | oats + sweeteners + oil |

| Primary processing | 6–10% | oat rolling + sorting losses |

| Secondary manufacturing | 12–18% | throughput, changeovers |

| Packaging & QA | 10–16% | film structure, print, testing |

| Logistics & distribution | 6–12% | cube, lanes, damage |

| Wholesale/retail margin & fees | 8–15% | channel terms, chargebacks |

| Supply Chain Node | Cost Ratio (% of Final Landed Cost) | What moves it most |

|---|---|---|

| Upstream raw materials | 55–70% | nuts/dried fruit/chocolate |

| Primary processing | 7–12% | grading rejects, foreign material removal |

| Secondary manufacturing | 10–16% | allergen changeovers, scrap |

| Packaging & QA | 8–14% | barrier + allergen governance |

| Logistics & distribution | 5–10% | inbound complexity + outbound cube |

| Wholesale/retail margin & fees | 5–12% | channel mix |

| Supply Chain Node | Cost Ratio (% of Final Landed Cost) | What moves it most |

|---|---|---|

| Upstream raw materials | 50–65% | GF oats premium + controlled inclusions |

| Primary processing | 8–14% | segregation + testing overhead |

| Secondary manufacturing | 10–18% | dedicated lines, longer changeovers |

| Packaging & QA | 10–16% | additional verification/testing |

| Logistics & distribution | 5–10% | similar to mainstream |

| Wholesale/retail margin & fees | 5–12% | channel mix |

Global oats are tradable, but your granola operation is not.

Procurement implication: You need a dual strategy:

Procurement teams often expect a clean pass-through: “oats down → granola down.” In practice, granola quotes disconnect because:

These are predictable failure modes when a skilled procurement manager is new to granola:

Problem: Margin pressure + volatile inputs + service penalties.

Periodic RFQs and aggressive negotiation on price.

The same “commodity + capacity + governance” pattern repeats in other procurement portfolios:

Takeaway: intelligence-led sourcing is less about “finding cheaper suppliers” and more about preventing predictable margin leakage from volatility, quality holds, and service penalties.

Granola is a strong test case because it forces a service to prove it can support decisions across four outcomes simultaneously:

If you share (a) your top 3 SKUs by margin exposure and (b) whether you run in-house or co-man, the analysis can be tightened into a category strategy that’s specific enough to execute (RFQs, dual-source plan, and contract/indexation structure).

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.