This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Frozen whole chicken is often treated like a simple commodity buy, but sourcing outcomes are usually decided by three constraints procurement teams can’t “negotiate away”: (1) biological production lead times, (2) vertically integrated capacity allocation, and (3) cold-chain and SPS/documentation execution risk. This guide translates those realities into practical sourcing actions—how to time events, structure specs, build backup supply, and govern performance—without overpromising what any single data source or supplier claim can guarantee.

(Analyzed at: Mar, 2026)

Frozen whole chicken looks like a simple commodity, but procurement outcomes are driven by biology + vertical integration + cold-chain physics + SPS compliance.

Key insight: Frozen whole chicken is a feed-and-energy dominated category with a biological production cycle. Price movements often reflect lagged feed economics, plus sudden discontinuities from avian influenza (HPAI) and trade/SPS actions.

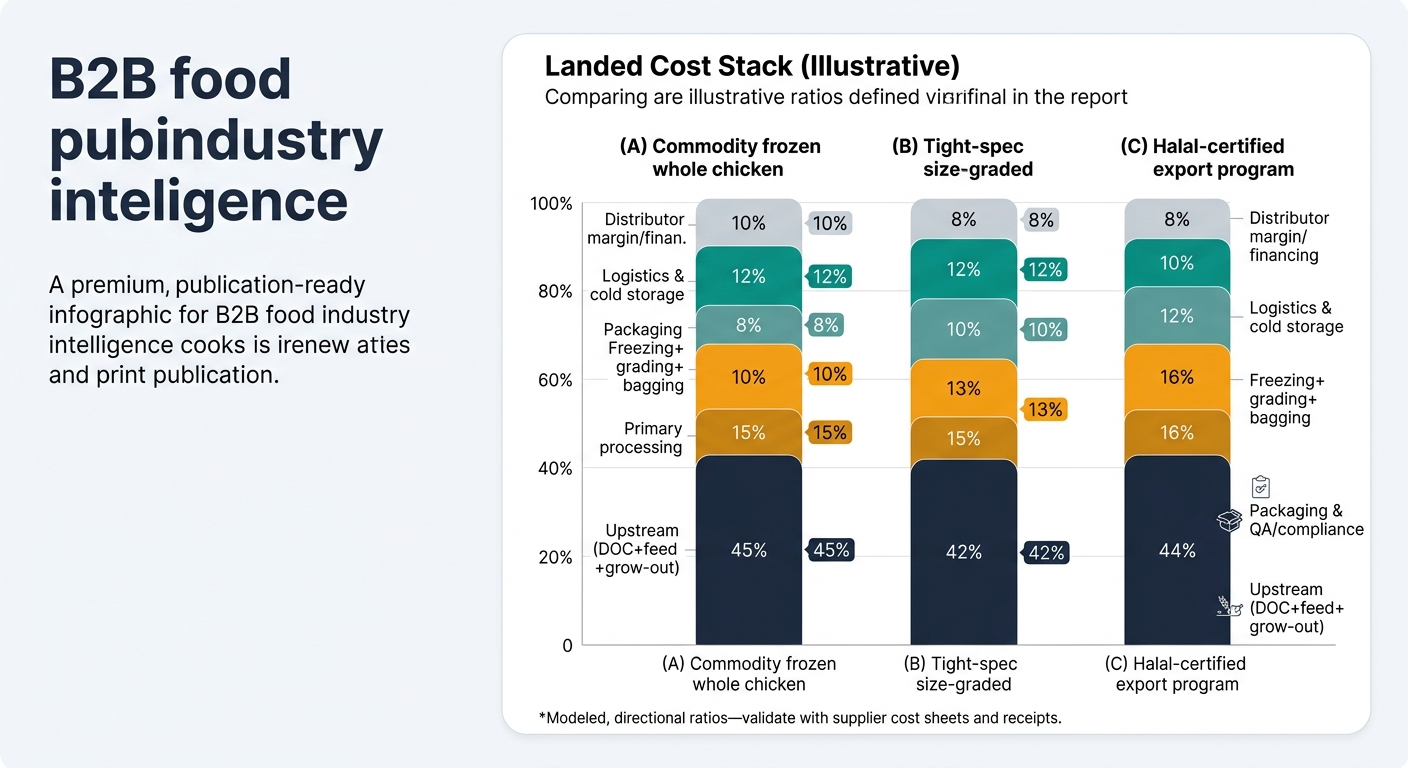

These ratios are modeled, directional to show where cost concentrates by product form. Validate with supplier cost sheets, freight invoices, and internal receipts.

| Supply Chain Node | Cost Ratio (% of landed cost) | What typically explains variance |

|---|---|---|

| Upstream (DOC + feed + grow-out) | 45% | Feed moves, flock performance, mortality |

| Primary processing | 15% | Labor, yield loss, sanitation downtime |

| Freezing + grading + bagging | 10% | Electricity, freezer capacity, tight size grading |

| Packaging & QA/compliance | 8% | Labeling, certs, inspection intensity |

| Logistics & cold storage | 12% | Reefer availability, dwell time, demurrage |

| Distributor margin/financing | 10% | Inventory carry, FX (if import), credit terms |

| Supply Chain Node | Cost Ratio (% of landed cost) | What typically explains variance |

|---|---|---|

| Upstream (DOC + feed + grow-out) | 42% | More birds needed to hit narrow band; selection loss |

| Primary processing | 15% | Similar base cost |

| Freezing + grading + bagging | 13% | Higher grading labor, more rework/segregation |

| Packaging & QA/compliance | 10% | Higher inspection/hold risk, more documentation |

| Logistics & cold storage | 12% | Same physics; higher risk cost if rejected |

| Distributor margin/financing | 8% | Often negotiated down with volume commitments |

| Supply Chain Node | Cost Ratio (% of landed cost) | What typically explains variance |

|---|---|---|

| Upstream (DOC + feed + grow-out) | 44% | Same biology; segregation costs can appear upstream |

| Primary processing | 16% | Halal process controls, segregation |

| Freezing + grading + bagging | 10% | Similar |

| Packaging & QA/compliance | 12% | Halal documentation, audits, export certificates |

| Logistics & cold storage | 10% | Route-specific reefer and port handling |

| Distributor margin/financing | 8% | Market structure and credit risk |

Frozen whole chicken supply is concentrated in vertically integrated systems, which means:

Key insight: In frozen whole chicken, price is a blend of (1) lagged feed economics, (2) sudden risk events, and (3) cold-chain/logistics basis—so two buyers can see very different outcomes in the same month.

This is not about replacing audits or supplier relationships. It’s about making your decisions earlier and with better evidence.

The same intelligence-led mechanics apply whenever biology, compliance, and logistics interact.

Frozen whole chicken is a harsh test because it forces procurement to manage all four at once:

If your team can institutionalize:

…you reduce emergency buys, improve OTIF, and make sourcing decisions easier to defend in audits and finance reviews.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.