This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

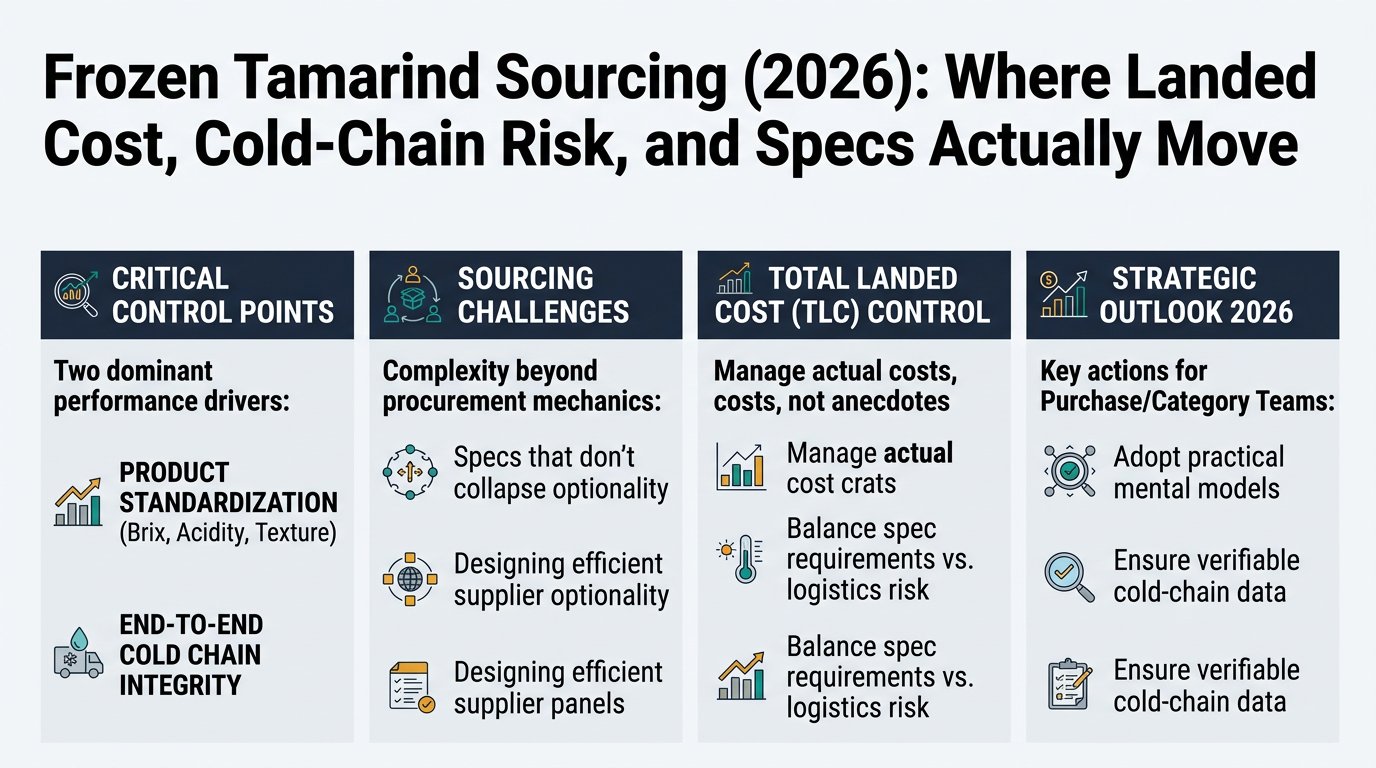

Frozen tamarind procurement looks straightforward until you get hit by the two things that most often drive real-world outcomes: (1) where and how the product is standardized (Brix/acidity/texture) and (2) whether the cold chain is actually held end-to-end. This guide is written for Purchase / Category Management teams who already know procurement mechanics, but need a practical mental model for frozen tamarind so you can design a supplier panel, set a spec that doesn’t collapse optionality, and control total landed cost (TLC) without relying on anecdotes.

(Analyzed at: Mar, 2026)

Frozen tamarind looks like a simple ingredient (pulp/paste/blocks). In reality, your outcomes (cost stability, continuity, claims rate) are determined by where standardization happens and how well the cold chain is held.

In frozen tamarind, yield loss + standardization + cold chain often matter as much as farmgate price. A “cheap” supplier can become expensive through:

Below is a practical, procurement-oriented view of what each node adds.

Harvest timing varies by region. India-facing references commonly cite harvesting roughly Feb–early Apr, and many non-technical summaries generalize Jan–Apr. Use this as directional seasonality only and validate by your origin and supplier. [2]

Treating tamarind like a uniform commodity: not accounting for yield variability that shows up later as higher conversion cost.

Labor-heavy removal of shell/seed, coarse pulping; sometimes compressed blocks are produced for storage/trade.

Specs that don’t define seed/fiber tolerance clearly, leading to hidden yield loss at your plant or at the secondary processor.

This is the “value-add” step that most affects finished-product consistency:

Buying frozen tamarind on price without confirming where standardization happens (supplier-controlled vs buyer-controlled) and how they manage lot-to-lot variation.

Packaging formats (industrial liners/cartons, pails/tubs, 0.5–5 kg blocks) affect handling loss and thaw management.

Overlooking packaging as a spec lever: switching from tubs to blocks can reduce packaging cost but may increase handling time and thaw exposure at receiving.

Cold chain integrity is a first-order quality driver. Frozen pulp/purée is commonly expected to remain at about 0°F / −18°C or colder with minimal fluctuation (air temp vs product temp must be understood and monitored). [3]

Comparing suppliers on FOB price while ignoring lane risk (a “cheaper” origin can have systematically higher temperature-excursion incidence).

Importers/DCs absorb cold storage, inspection holds, and onward frozen distribution.

Not modeling total landed cost (TLC): unit price + freight + cold storage + shrink + claims.

These are modeled ratios to show where costs concentrate for different frozen-tamarind forms. Actuals vary by origin, spec tightness, packaging, and season.

| Supply chain node | Cost ratio (% of final delivered cost) | What typically moves it |

|---|---|---|

| Raw material (pods/collection) | 25% | harvest tightness, domestic demand |

| Primary processing | 18% | labor, yield loss, foreign matter control |

| Secondary processing + freezing | 22% | finishing losses, energy, standardization |

| Packaging & QA | 8% | liners/cartons, testing frequency |

| Export + import logistics (cold chain) | 17% | reefer rates, port dwell, cold storage |

| Importer/DC + distribution margin | 10% | service level, shrink, financing |

| Supply chain node | Cost ratio (% of final delivered cost) | What typically moves it |

|---|---|---|

| Raw material | 22% | same drivers as pulp |

| Primary processing | 16% | same drivers, slightly less leverage |

| Secondary processing + freezing | 28% | more finishing, tighter viscosity/texture, more rework |

| Packaging & QA | 9% | often higher QA + handling needs |

| Export + import logistics | 15% | lane risk still material |

| Importer/DC + distribution margin | 10% | same |

| Supply chain node | Cost ratio (% of final delivered cost) | What typically moves it |

|---|---|---|

| Raw material | 18% | fruit cost diluted by sugar input |

| Primary processing | 14% | yield and labor |

| Secondary processing + freezing | 26% | formulation control, blending, energy |

| Added ingredients (e.g., sugar) | 10% | sweetener price and dosing |

| Packaging & QA | 10% | labeling, allergen/cross-contact controls |

| Export + import logistics | 12% | reefer + cold storage |

| Importer/DC + distribution margin | 10% | same |

Frozen tamarind’s risk profile is dominated by two control points:

If either control point is weak, you get:

In this category, raw pod tightness and frozen delivered price can disconnect for months.

Your best hedge is not “guessing the harvest” but building a model that separates:

This is where procurement intelligence is practical: it helps you make earlier, better-scoped decisions—but it does not replace supplier qualification, audits, lab testing, or contract negotiation.

Turn specs into supply-market implications:

Output: a controlled substitution ladder for continuity events.

Track disruption signals that matter for frozen tamarind:

Output: trigger points for pre-booking capacity, safety stock, or volume reallocation.

Frozen tamarind is a clean example of a broader procurement pattern: spec + conversion yield + cold chain create hidden TCO.

If you build the muscle here—spec governance, lane risk modeling, and substitution ladders—you reuse it across your frozen fruit ingredient portfolio.

Frozen tamarind rewards teams that manage the category like a system, not a SKU:

The practical takeaway: in frozen tamarind, the best procurement outcomes come from aligning spec discipline, supplier capability, and lane reliability—and using intelligence to make those trade-offs explicit and auditable.

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.