This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Frozen red beets look like a straightforward frozen-vegetable SKU, but procurement outcomes (price, service, and risk) are driven by a few structural realities: seasonal raw supply, capacity bottlenecks at processors, and a year-round cold-chain + energy cost base. This guide translates those realities into decision-ready actions—so procurement leaders can set defensible pricing targets, build a qualified backup bench, and run governance that prevents supply disruption.

Analyzed at: Mar, 2026

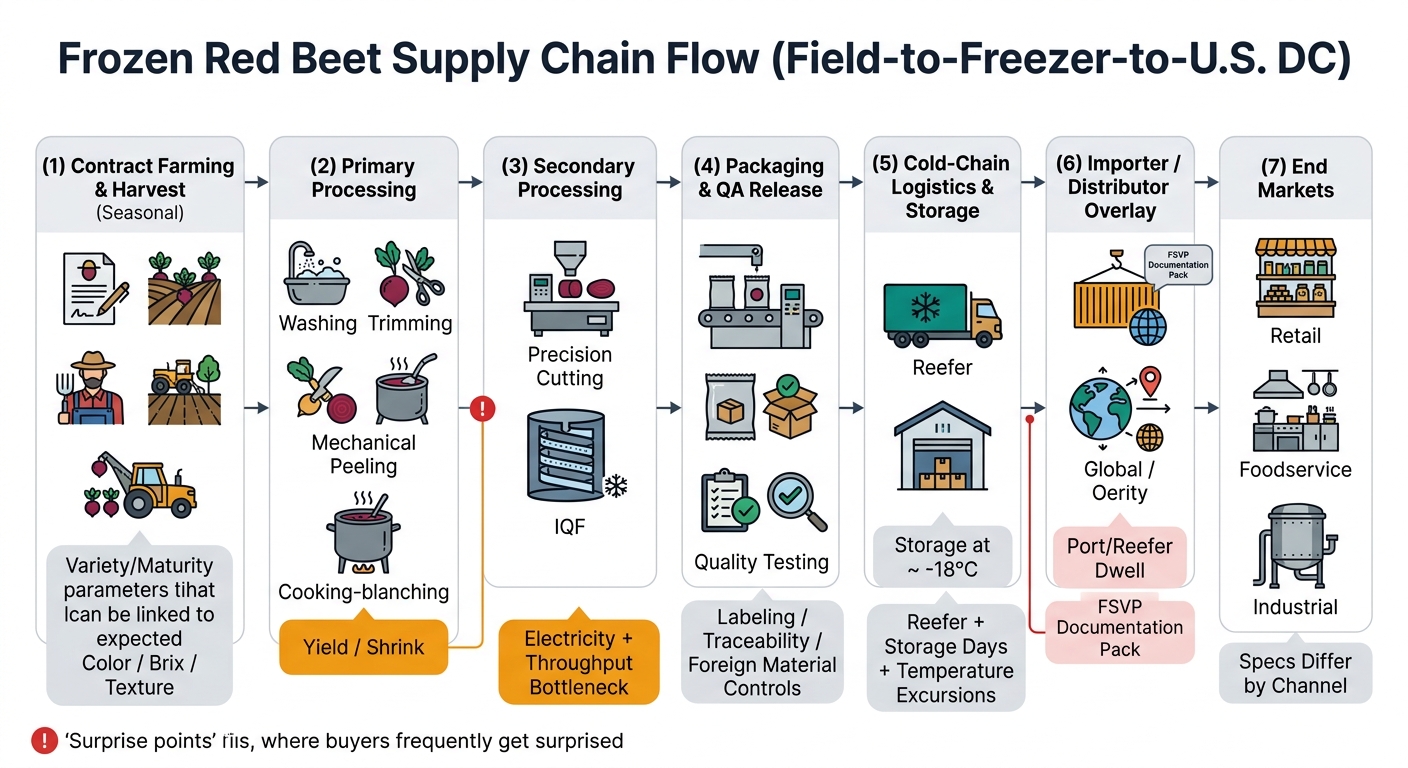

Frozen red beets look like a simple frozen-veg SKU, but the supply chain behaves more like a seasonal crop + energy-intensive processing + cold-chain dependent distribution system.

Key insight: Your final frozen cost is often “locked in” before you ever negotiate—via acreage contracting, variety selection, and quality bands (size, color intensity, defects). A cheap raw beet can still produce expensive frozen output if it creates poor yields or higher sorting/rework.

Key insight: This is where frozen red beets differ from many other frozen veg items: peeling + cooking can turn small upstream variability into big downstream cost. The buyer experiences this as “supplier suddenly needs a price increase” or “color drift.”

Key insight: Frozen red beet economics are highly sensitive to electricity and refrigeration. When energy prices spike, processors either (a) reprice, (b) reduce production runs, or (c) prioritize higher-margin SKUs.

Key insight: Packaging is not just material cost—pack format drives labor, changeovers, and MOQ economics.

Key insight: For frozen red beets, logistics cost is a time function (storage days) as much as a distance function.

Key insight: The downstream margin often reflects service-level commitments (fill rate, short lead times) that require inventory positioning.

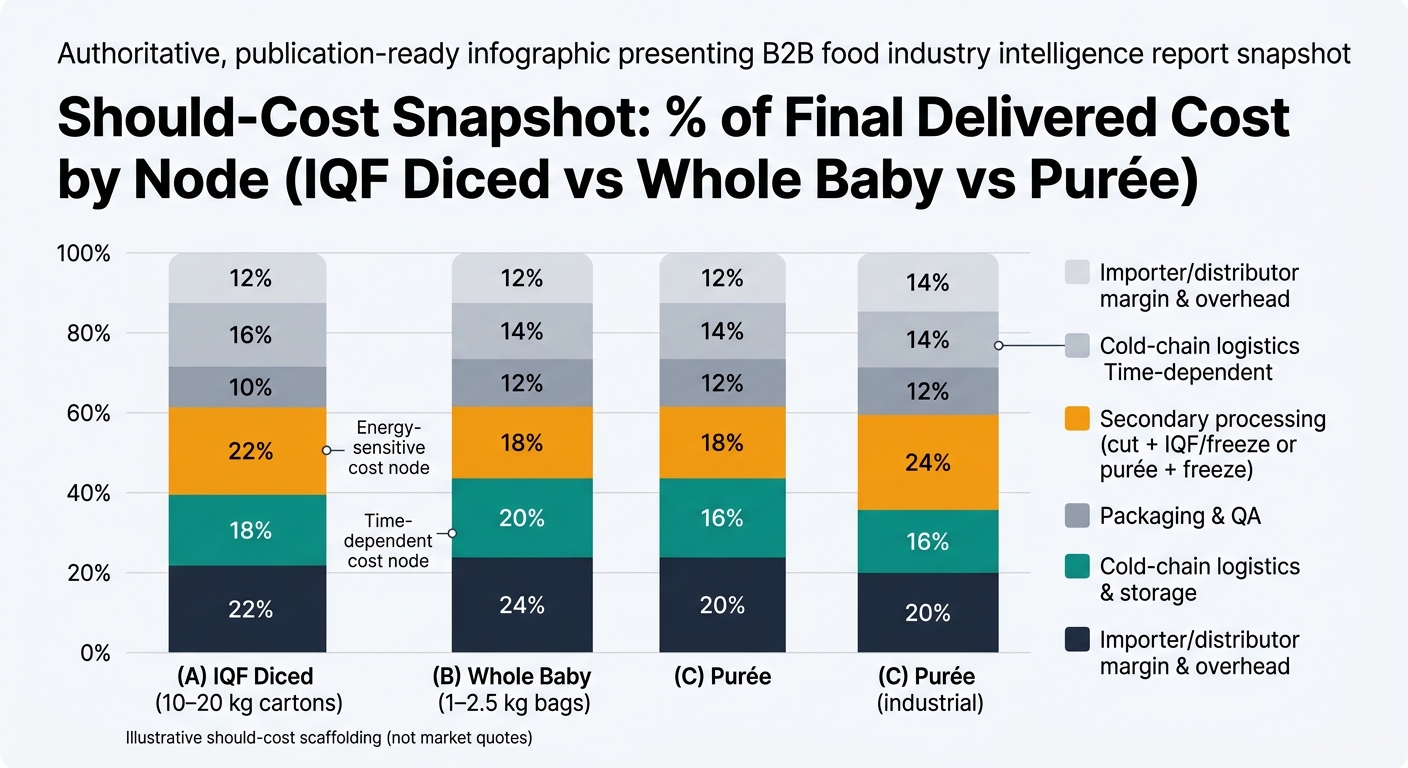

The table below is a practical procurement model of % of final delivered cost (delivered to your U.S. DC or plant). Actual ratios vary by origin, energy regime, pack format, and Incoterms.

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most |

|---|---|---|

| Farming / raw beets | 22% | crop yield/grade, contract terms |

| Primary processing (wash/peel/cook) | 18% | shrink, water/wastewater, thermal energy |

| Secondary processing (cut + IQF freeze) | 22% | electricity, freezer capacity, labor |

| Packaging & QA release | 10% | carton/liner, QA holds/rework |

| Cold-chain logistics & storage | 16% | reefer rates, storage days, port dwell |

| Importer/distributor margin & overhead | 12% | service level, financing, compliance |

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most |

|---|---|---|

| Farming / raw beets | 24% | baby size availability, grade premiums |

| Primary processing (wash/peel/cook) | 20% | peeling losses, uniformity |

| Secondary processing (freeze) | 18% | energy, throughput |

| Packaging & QA release | 12% | bagging labor, label complexity |

| Cold-chain logistics & storage | 14% | storage duration, lane selection |

| Importer/distributor margin & overhead | 12% | fill-rate commitments |

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most |

|---|---|---|

| Farming / raw beets | 20% | solids/brix, color intensity |

| Primary processing (cook) | 16% | thermal energy, yield |

| Secondary processing (puréeing + freeze) | 24% | energy + equipment, QA testing |

| Packaging & QA release | 12% | aseptic/frozen format choice |

| Cold-chain logistics & storage | 14% | density, storage days |

| Importer/distributor margin & overhead | 14% | technical service + compliance |

Frozen red beet supply is stabilized by inventory, but cost is destabilized by utilities:

For U.S. buyers, this matters more because imports and cold-chain infrastructure are integral to the category; USDA ERS data shows frozen vegetable imports reached record values in 2024. [1]

Procurement teams often expect a clean linkage: farm price down → frozen price down. In frozen red beets, you frequently get:

Selected playbook:Build a qualified backup supply plan before disruption

Not “who is cheapest,” but:

Frozen red beets are a clean example of a broader procurement truth: unit price is rarely the best decision variable when yield, energy, and logistics dominate.

If your organization buys multiple frozen items, the same intelligence approach (benchmarking + risk triggers + governance artifacts) scales across the portfolio.

Frozen red beets are a “small enough” category to pilot better sourcing governance, but “complex enough” to prove value quickly:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.