This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

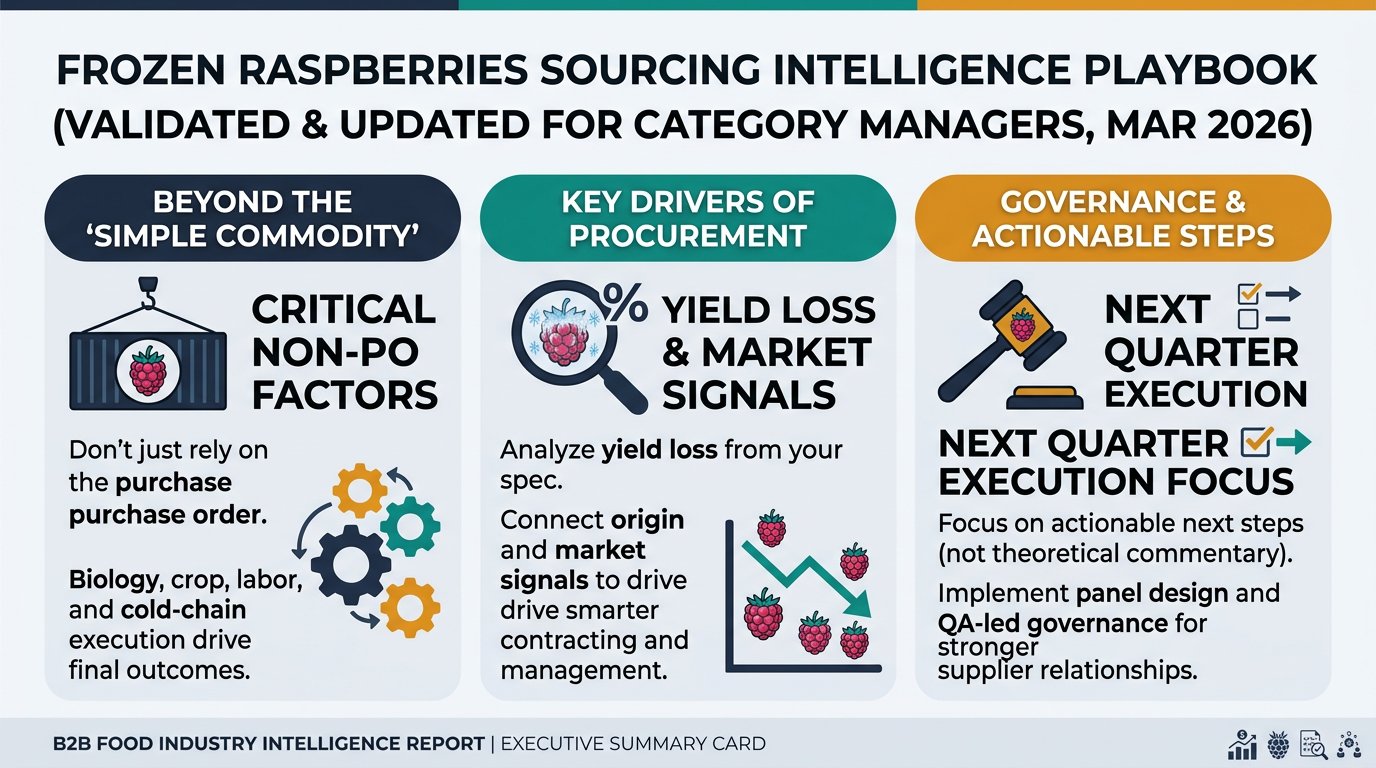

Frozen raspberries behave like a “simple commodity” only on the PO. In reality, outcomes are driven by biology (crop + labor), yield loss created by your spec, and cold-chain execution—so the best procurement decisions come from connecting market/origin signals to contracting, panel design, and QA-led governance. This playbook is written for Purchase – Product & Category Management teams who are strong procurement professionals but newer to frozen raspberries, and it focuses on what to do next quarter (not theoretical market commentary).

Analyzed at: Mar, 2026

Frozen raspberries look like a simple commodity, but procurement outcomes (cost, continuity, claims, audit exposure) are determined by where value and risk concentrate in the chain.

Key insight: In frozen raspberries, procurement leverage is often misapplied to “processor price per kg” while the biggest controllable drivers sit in (a) raw fruit + yield, (b) spec-driven sorting loss, and (c) cold-chain and inventory time.

A “cheap origin” can become expensive if it produces more crumble/broken than your spec allows.

This is where your spec becomes a cost function:

Tightening defect tolerances can raise price and reduce available supplier pool, increasing continuity risk.

Purée can be a resilience tool (substitution) but changes functional specs and stakeholder approvals.

Modeled ranges to show where cost concentrates. Actual ratios vary by origin, spec tightness, lane, incoterms, and seasonality.

| Supply Chain Node | Cost Ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Farm & harvest (raw fruit) | 40–55% | labor + weather-driven yield |

| Primary processing (sort + IQF freezing) | 15–25% | spec tightness, sorting loss, energy |

| Secondary processing | 0% | N/A |

| Packaging & QA | 5–10% | testing holds, carton/liner |

| Cold-chain logistics | 10–18% | reefer + cold storage + dwell |

| Importer/distributor margin | 5–15% | service level, financing |

| Supply Chain Node | Cost Ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Farm & harvest (raw fruit) | 35–50% | raw fruit pricing |

| Primary processing | 12–20% | lower sorting loss than whole |

| Secondary processing | 0% | N/A |

| Packaging & QA | 4–9% | similar pack, sometimes lighter QA |

| Cold-chain logistics | 10–18% | lane + storage |

| Importer/distributor margin | 8–20% | more spot trading / blending |

| Supply Chain Node | Cost Ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Farm & harvest | 25–40% | grade flexibility |

| Primary processing | 8–16% | intake + base freezing |

| Secondary processing (milling/standardization) | 12–25% | blending, possible heat treatment |

| Packaging & QA | 7–14% | specs: Brix/seed/viscosity |

| Cold-chain logistics | 8–16% | density helps freight efficiency |

| Importer/distributor margin | 5–15% | application support + inventory |

Structural fact:Processing and trading hubs can decouple “where it’s grown” from “where it’s exported.” Poland is widely referenced as a primary exporter of frozen berries into Europe, and Serbia is heavily export-oriented in frozen raspberries/processed raspberry products. [1]

Treat origin as a two-layer concept:

In many categories, higher price implies lower risk (better suppliers, better controls). In frozen raspberries, price spikes often coincide with higher risk.

Enteric virus outbreaks have been linked to frozen berries; Germany’s 2012 norovirus outbreak (frozen strawberries) shows how frozen product can still carry viral risk if controls fail upstream and product is consumed without adequate heat treatment. [3]

Your “best price” event timing can be the same window where continuity + quality + compliance are most fragile.

This is not about predicting the exact price. It’s about translating signals into category actions that reduce volatility exposure and prevent forced spot buys.

Frozen raspberries are a clean example of a broader procurement truth: when upstream biology + processing yield + logistics constraints interact, quotes alone are a weak decision tool.

The transferable lesson: intelligence-led procurement is how you connect risk signals → contract choices → operational readiness.

Frozen raspberries force clarity on the questions that separate average category management from excellent category management:

When you can answer those with evidence, you get measurable outcomes:

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.