This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

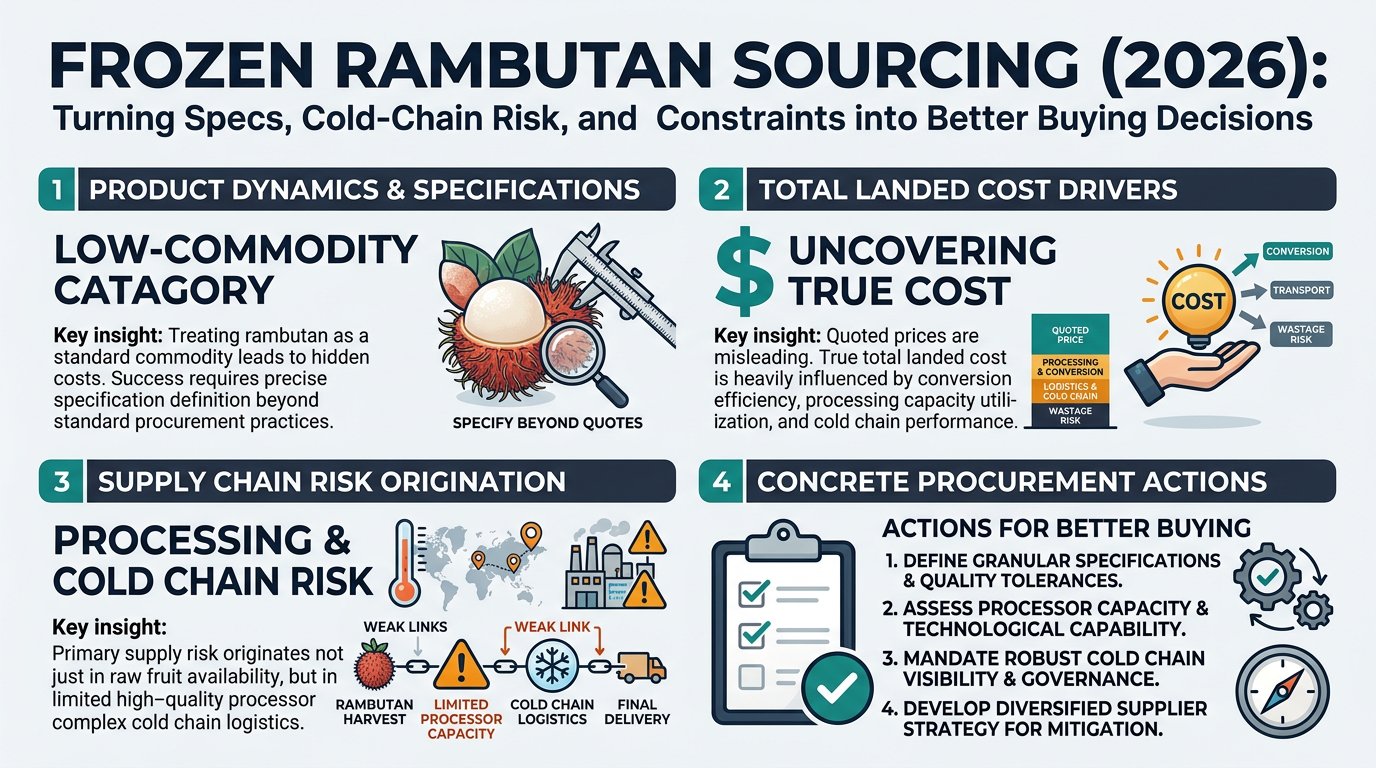

Frozen rambutan is a small but high-friction frozen fruit category: it behaves less like a “commodity buy” and more like a conversion-and-cold-chain procurement problem. This guide is written for category managers who are strong procurement professionals but newer to rambutan specifically. It explains what drives true landed cost (not just the quote), where supply risk really originates (often in processing capacity and cold chain), and how to translate intelligence into concrete actions across specs, supplier strategy, contracting, and ongoing governance.

Analyzed at: Mar, 2026

Frozen rambutan is not “a frozen fruit commodity” in the way frozen mango or pineapple can be. It’s a seasonal, labor-intensive conversion (peeling/de-seeding + freezing) that must happen fast and hygienically near origin, then survive a long cold chain.

What this means for a category manager: you’re buying a seasonal inventory build that processors freeze and hold, so your contract timing and volume allocation decisions matter more than “spot price shopping.”

Below is a node-by-node view of cost and margin structure, written for the decisions you control: spec, supplier selection, contract structure, and continuity plans.

Key insight: Fresh rambutan cost is the trigger for volatility, but it’s not the whole story—your spec determines how much of that fruit becomes sellable frozen aril.

Main cost drivers

Margin behavior

Key insight: This is the economic center of gravity for frozen rambutan. The category is constrained by labor throughput + yield loss + freezing capacity.

Main cost drivers

Margin behavior

Key insight: Secondary processing often looks “cheap” per kg, but it can hide rework losses and spec disputes (brix, piece integrity, syrup ratio, mix composition).

Main cost drivers

Margin behavior

Key insight: Packaging is not just a materials line—it's also compliance + claim prevention.

Main cost drivers

Key insight: Frozen is commonly managed at -18°C or colder; your risk is not only the setpoint, but dwell time, rollovers, and temperature excursions.

Main cost drivers

Operational reality to anchor specs:

Standards and commercial practice commonly anchor quick-frozen/frozen handling around -18°C (or colder), with temperature abuse showing up later as texture/drip loss. [2]

Key insight: Downstream margin is heavily influenced by service level (OTIF) and claim rates. A “cheaper” supplier that creates defects can cost more in net margin.

Main cost drivers

These are modeled to show where cost concentrates by product form. Actual ratios vary by origin, crop year, spec tightness, freight market, and customer channel.

| Supply chain node | IQF rambutan arils (seed-in) | IQF rambutan arils (seedless) | Frozen rambutan purée (industrial) | Notes (what moves the % in practice) |

|---|---|---|---|---|

| A) Farmgate & aggregation | 25–35% | 22–32% | 20–30% | Farmgate spikes in short crops; quality sorting affects usable input |

| B) Primary processing | 25–35% | 32–45% | 18–30% | Seedless increases labor + yield loss; purée can use broader grade fruit |

| C) Secondary processing | 0–5% | 0–5% | 10–18% | Purée standardization/blending adds processing and QA |

| D) Packaging & QA | 8–14% | 8–14% | 6–10% | Retail packs and strict QA increase share |

| E) Cold-chain logistics | 12–20% | 12–20% | 12–20% | Reefer market volatility shifts this materially |

| F) Import/distribution margin | 10–18% | 10–18% | 8–15% | Claim rates and service levels drive margin requirements |

Frozen rambutan is often processor-constrained, not purely farm-constrained.

Even if rambutan is widely grown, the exportable frozen product depends on a smaller set of processors that can reliably execute:

So when a buyer tightens specs (seedless, low browning, tight size uniformity), the available supplier universe shrinks non-linearly—and pricing power shifts upstream to processors.

For frozen rambutan, price moves are often driven by conversion economics more than headline fruit availability.

Procurement implication: You need a cost view that separates:

This is not about “more data.” It’s about changing buying behavior at four decision points.

Intelligence inputs

Actions

Intelligence inputs

Actions

Intelligence inputs

Actions

Intelligence inputs

Actions

Frozen fruit has had notable virus-related outbreak investigations (e.g., hepatitis A / norovirus in frozen berries). This is a reminder that freezing does not “kill” all hazards and that supplier hygiene and controls matter. [3]

Frozen rambutan behaves like a “processor-constrained tropical,” which is a pattern you’ll also see in:

The transferable lesson: the best procurement outcomes come from separating raw material volatility from conversion + logistics constraints, then structuring contracts and supplier portfolios accordingly.

Frozen rambutan forces good procurement discipline because it combines:

If your team can build a repeatable intelligence-driven sourcing approach here—spec tiers, dual-sourcing triggers, cost-driver decomposition, and performance governance—you can reuse the same operating model across your broader frozen and specialty fruit portfolio.

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.