This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Frozen pumpkin is easy to treat like a standard frozen-veg line item—until a harvest-quality swing, a plant constraint, or a cold-chain disruption turns into allocation, spec drift, or emergency buys.

This guide is written for procurement and sourcing managers who are strong in general sourcing but newer to frozen pumpkin. It translates the category’s “product reality” (puree vs. dice, solids/Brix, cut integrity, cold chain) into practical levers: how to structure contracts, how to avoid hidden yield costs, how to reduce concentration risk, and what governance triggers to put in place so you act before service fails.

(Analyzed at: Mar, 2026)

Frozen pumpkin looks like a simple vegetable ingredient, but procurement outcomes are usually determined by three realities:

Decision you’re usually trying to make (even if it’s not stated):

“How do I lock in competitive cost without over‑concentrating on one plant/origin/spec that will break continuity later?”

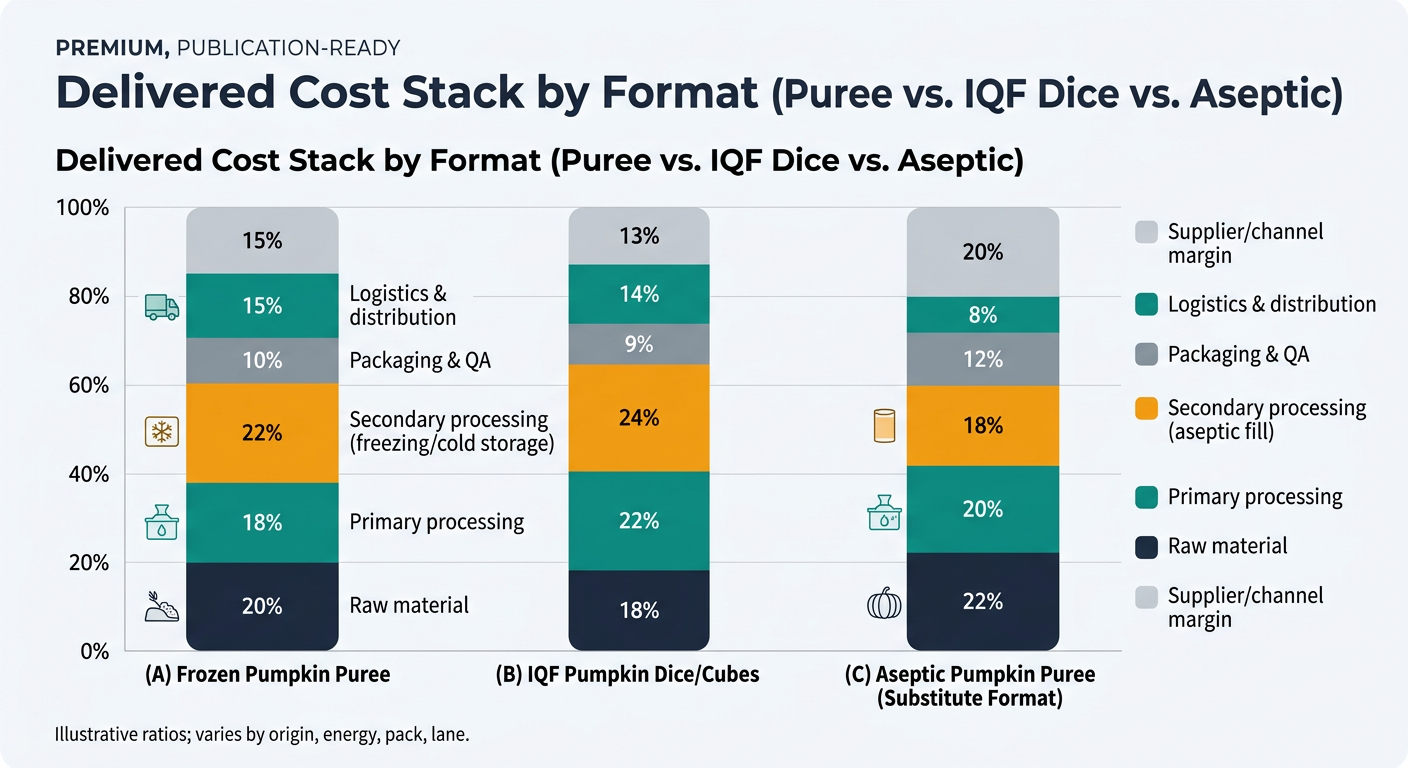

Below is a procurement-oriented cost walk that maps where cost and margin tend to concentrate—and which levers are actually negotiable.

Key insight: In frozen pumpkin, farmgate price matters, but usable yield matters more. A cheap crop with low dry matter or high defect rate can be more expensive after conversion.

Key insight: This is where hidden cost sits: yield loss at trim and seed removal + energy/water/effluent costs.

Key insight: Freezing economics are dominated by energy intensity and capacity utilization. When plants are full, they allocate capacity to the “best customers.”

Key insight: For frozen pumpkin, packaging is not “just packaging.” It is line compatibility + traceability + complaint risk control.

Key insight: Landed cost volatility often comes from reefer + cold storage more than from the pumpkin itself—especially for imported supply.

Key insight: Frozen pumpkin is often an ingredient inside a higher-margin SKU (soups, bakery, ready meals). That means procurement pressure typically focuses on cost, while operations/QA pressure focuses on continuity and spec.

Modeled to show where cost concentrates by product form; actual ratios vary by origin, contract terms, energy costs, pack format, and lane.

| Supply chain node | Cost ratio (% of delivered cost) | What to watch as a buyer |

|---|---|---|

| Raw material (pumpkin) | 20% | Solids/dry matter variability changes conversion value |

| Primary processing | 18% | Yield loss at trim/seed removal; cooking energy |

| Secondary processing (freezing + cold storage at origin) | 22% | Allocation risk when freezer capacity tight |

| Packaging & QA | 10% | Lot integrity, foreign material controls |

| Logistics & distribution | 15% | Reefer + cold storage + dwell time |

| Supplier + channel margin | 15% | Margin expands in shortage periods |

| Supply chain node | Cost ratio (% of delivered cost) | What to watch as a buyer |

|---|---|---|

| Raw material (pumpkin) | 18% | Size/firmness affects dice yield and breakage |

| Primary processing | 22% | Cutting losses, blanching losses, labor |

| Secondary processing (IQF + cold storage) | 24% | IQF throughput constraints + energy |

| Packaging & QA | 9% | Screen size, defect tolerances, foreign material |

| Logistics & distribution | 14% | Lane volatility and temperature control |

| Supplier + channel margin | 13% | Premium for tight spec + consistent cut |

| Supply chain node | Cost ratio (% of delivered cost) | What to watch as a buyer |

|---|---|---|

| Raw material (pumpkin) | 22% | Solids variability still matters |

| Primary processing | 20% | Cook/pulp/sieve costs |

| Secondary processing (aseptic processing/fill) | 18% | Sterilization + aseptic packaging line constraints |

| Packaging & QA | 12% | Aseptic packaging material + sterility assurance |

| Logistics & distribution | 8% | No frozen chain; different warehousing |

| Supplier + channel margin | 20% | Value add for shelf-stable continuity |

Note on specs (validated): Published supplier specs for pumpkin puree show Brix ranges that can vary widely by product and application (e.g., one pumpkin puree spec lists Brix 5–10) [3]. This is why procurement should treat “Brix” as an application-specific requirement, not a universal number.

Procurement takeaway: Your leverage is less about “how many farms exist” and more about how many qualified plants can hit your spec, pack, audit, and lead-time requirements.

Frozen pumpkin is a category where price signals lag risk signals.

So the true cost is:

Invoice price + yield loss + quality holds + cold-chain claims + expedite freight.

The goal is to convert scattered signals into repeatable governance: when to rebid, when to dual-source, when to lock, when to flex spec.

Boundaries (important): intelligence supports decisions; it does not replace QA validation, plant audits, or legal review.

Frozen pumpkin is a clean example of a broader procurement pattern: processed-food inputs where capacity + cold chain create hidden constraints.

Comparable categories where intelligence-driven sourcing tends to outperform:

In all of these, the “best price” supplier is not always the “lowest total cost” supplier once you include yield, quality incidents, and logistics reliability.

Frozen pumpkin forces clarity on the questions procurement leadership should be able to answer at any time:

When teams can answer those with evidence, frozen pumpkin stops being a seasonal firefight and becomes a managed category with measurable resilience.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.