This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

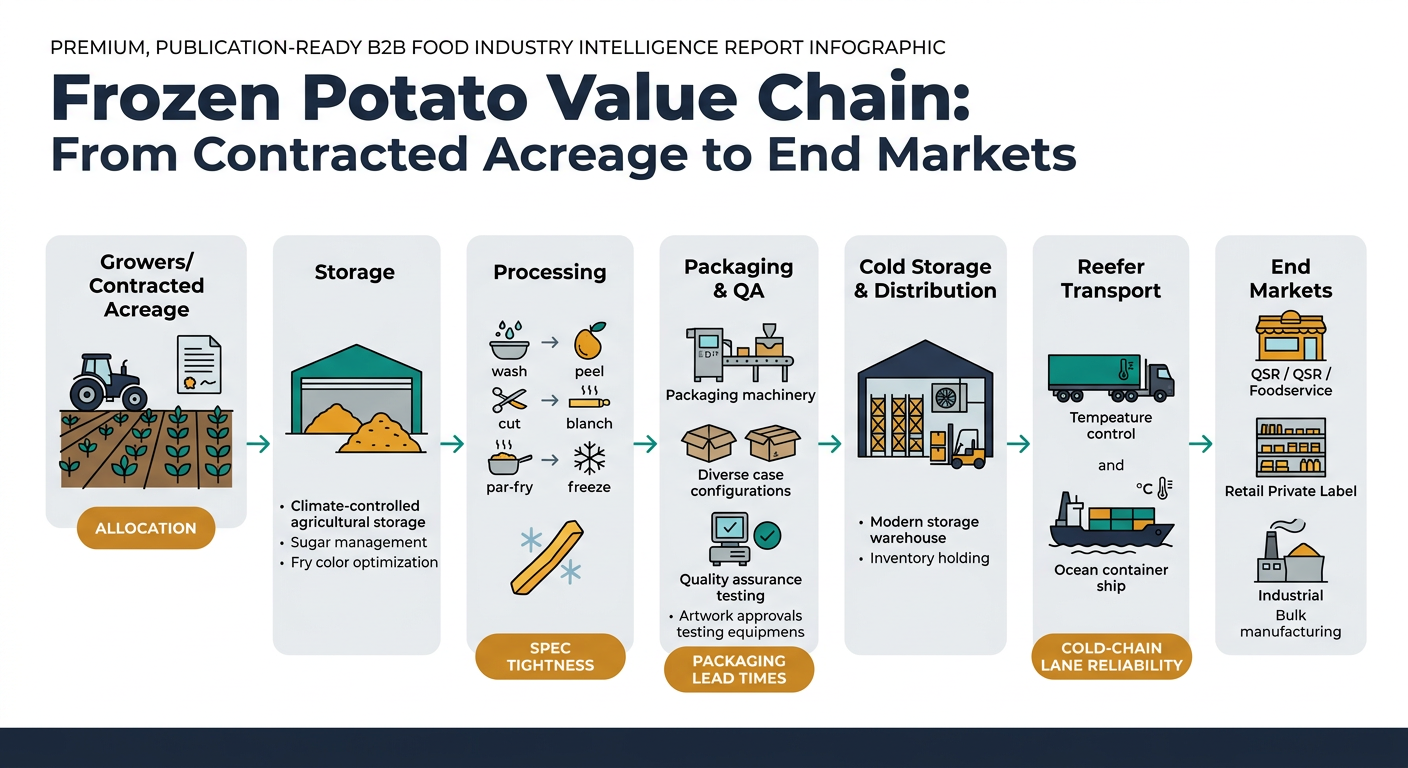

Frozen potato sourcing looks like a simple “commodity buy” until you try to switch suppliers mid-quarter and discover your real constraints: contracted acreage, processing capacity allocation, packaging/artwork lead times, and cold-chain lane reliability. This guide translates frozen-potato supply chain realities into procurement actions—how to benchmark suppliers on cost-to-serve, design volatility-aligned contracts, pre-qualify switch-ready alternates, and govern performance with trigger-based escalation.

(Analyzed at: Mar, 2026)

Frozen potato looks like a “simple” commodity until you try to switch suppliers mid-quarter.

The category behaves like a contracted-agriculture + high-capex manufacturing + cold-chain logistics business. That combination creates three procurement realities:

Key frozen-potato nuance non-experts miss: even if raw potato tonnage is “fine,” storage quality can degrade (e.g., cold-induced sweetening → higher reducing sugars → darker fry color), shrinking usable supply for fry-grade output and tightening certain SKUs. [1]

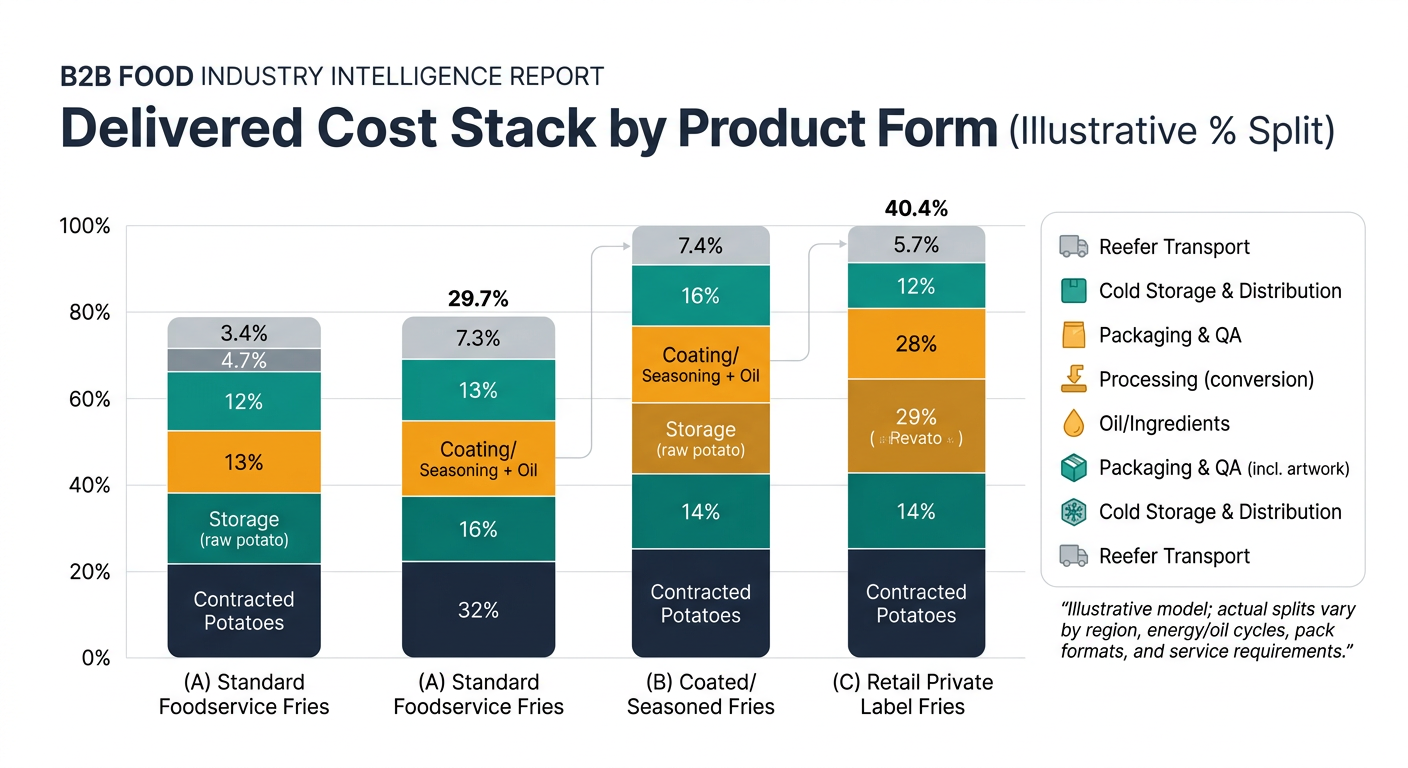

Key insight: Frozen potato is not raw-potato-cost-driven alone. The delivered cost is a layered stack where conversion energy, edible oil exposure, packaging, and cold-chain logistics can swing the outcome even when farmgate prices are stable.

Below is a procurement-oriented walkthrough of cost build-up by node—what drives it, what signals matter, and what tends to surprise teams.

Market reality example (capacity action): Lamb Weston’s FY25 restructuring plan (announced Oct 1, 2024) included permanent closure of its Connell, Washington facility and temporary curtailments across its North American network—an example of how processor network decisions can quickly change supply availability and negotiating leverage. [2]

Teams negotiate price but ignore that packaging changeovers + artwork lead times can make “switching suppliers” a 8–16 week process in practice.

These ratios are modeled to show where cost concentrates by product form. Actual splits vary by region, contract terms, energy/oil cycles, pack formats, and customer service requirements.

| Supply Chain Node | Cost Ratio (% of delivered cost) | What drives variance |

|---|---|---|

| Contracted potatoes (raw) | 25% | crop size/quality, contract terms |

| Storage (raw potato) | 6% | shrink, energy, quality drift |

| Processing (conversion) | 30% | energy, labor, yield, throughput |

| Oil / ingredients | 7% | oil price and usage rate |

| Packaging & QA | 8% | cartons/film, QA intensity |

| Cold storage & distribution | 10% | electricity, capacity, dwell |

| Reefer transport | 14% | lane rates, equipment, accessorials |

| Supply Chain Node | Cost Ratio (% of delivered cost) | What drives variance |

|---|---|---|

| Contracted potatoes (raw) | 20% | crop size/quality |

| Storage (raw potato) | 5% | shrink, energy |

| Processing (conversion) | 28% | line efficiency, changeovers |

| Coating/seasoning + oil | 15% | ingredient inflation, formulation |

| Packaging & QA | 9% | tighter QA, labeling |

| Cold storage & distribution | 10% | dwell, electricity |

| Reefer transport | 13% | lane volatility |

| Supply Chain Node | Cost Ratio (% of delivered cost) | What drives variance |

|---|---|---|

| Contracted potatoes (raw) | 22% | crop and contract |

| Storage (raw potato) | 5% | energy, shrink |

| Processing (conversion) | 27% | throughput, downtime |

| Oil / ingredients | 8% | oil cycle |

| Packaging & QA (incl. artwork) | 12% | film, print lead times, compliance |

| Cold storage & distribution | 11% | inventory days, DC fees |

| Reefer transport | 15% | retail delivery constraints |

Structural fact #1: Export supply is geographically concentrated. Belgium and the Netherlands are repeatedly cited as a dominant export cluster for frozen processed potato products; industry materials referencing Rabobank-style framing commonly place them at roughly ~50% of global frozen processed potato exports. [3]

Structural fact #2: In the U.S., processing is the majority use, and frozen is the largest processing outlet. USDA reporting and synthesis literature show >60% of the U.S. crop typically goes to processing, and within processing, frozen fries/other frozen products are the largest share (one 2023 synthesis cites ~62% of processing allocated to frozen). [4]

Procurement teams often expect a simple relationship:

In practice, the relationship breaks because the delivered cost is dominated by conversion + cold chain + spec-driven yield.

Procurement takeaway: You need to separate:

This isn’t about “more data.” It’s about linking signals to decisions with an audit trail.

Frozen potato is a clean example of a broader procurement pattern: the biggest risks sit in the “in-between” layers (conversion constraints, logistics, and spec-driven optionality), not just raw input price.

Examples procurement leaders commonly own alongside frozen potato:

The transferable lesson: intelligence is most valuable when it ties signals to actions (contract structure, dual-source readiness, spec governance, inventory policy) and creates an auditable decision record.

Frozen potato procurement forces discipline because the category punishes “price-only” thinking quickly.

It’s powerful as an example because:

If you can operationalize intelligence here—benchmarking cost-to-serve, building switch-ready alternates, and running trigger-based governance—you typically can replicate the operating model across other volatile, spec-driven, logistics-sensitive categories.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.