This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

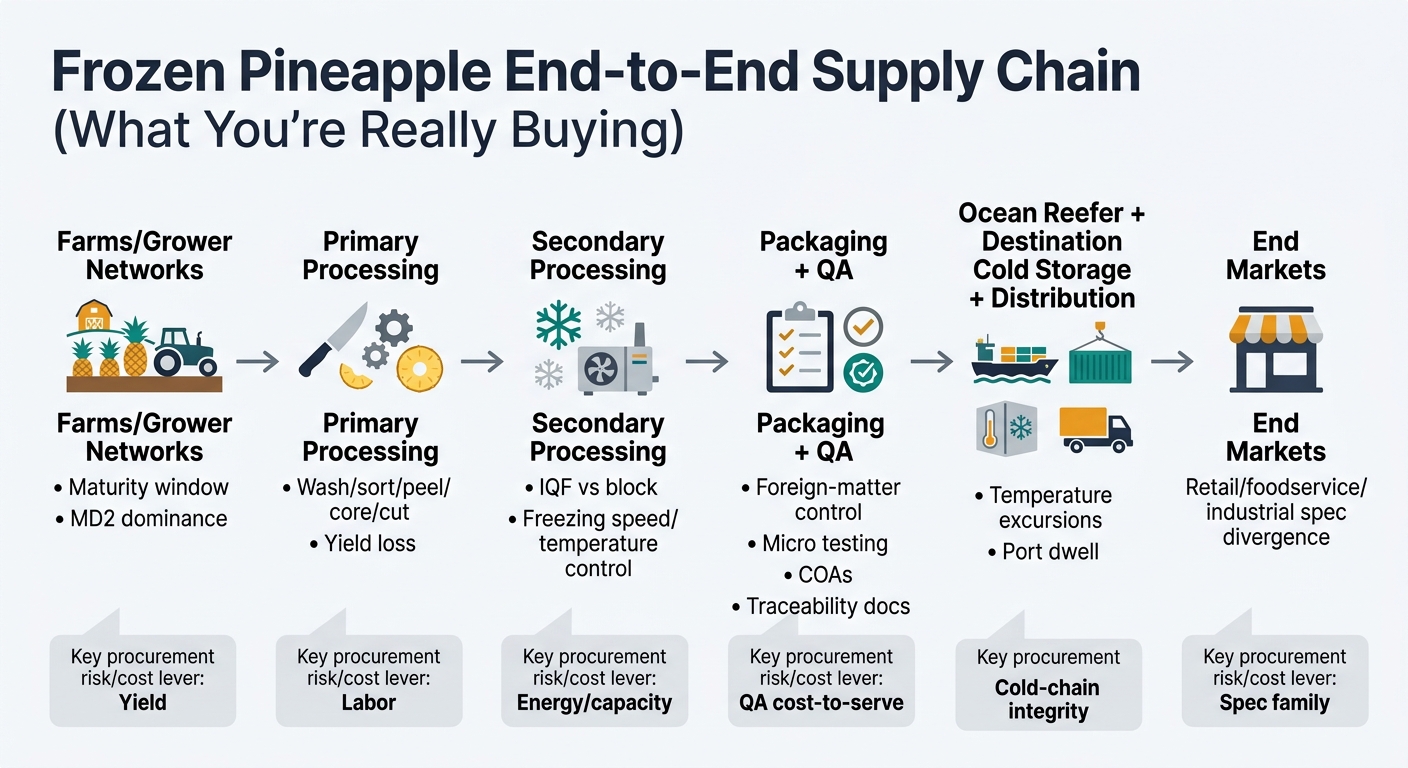

Frozen pineapple looks like a simple commodity (chunks in a bag), but procurement outcomes are determined upstream—by harvest maturity, processing yield, qualified capacity, and cold-chain integrity. This guide is written for procurement and sourcing leaders who are experienced category managers but newer to frozen pineapple: it explains what actually drives cost and risk, what to watch, and how to convert market/supplier signals into concrete sourcing actions you can defend internally.

Analyzed at: Mar, 2026

These steps commonly unlock mid-single-digit savings by reducing rejects/chargebacks and preventing premium-priced spot buys during disruptions, while improving continuity and auditability. [2]

Frozen pineapple looks like a simple commodity (chunks in a bag), but procurement outcomes are determined upstream—by harvest maturity, processing yield, and cold‑chain integrity.

Procurement implication: Your biggest levers are usually portfolio design (origin/supplier mix), spec discipline, and contract structure, not just unit price.

Key insight: Frozen pineapple cost is yield‑sensitive and logistics‑sensitive. Two suppliers can quote the same FOB but deliver different landed cost after factoring yield loss, claims, and cold‑chain failures.

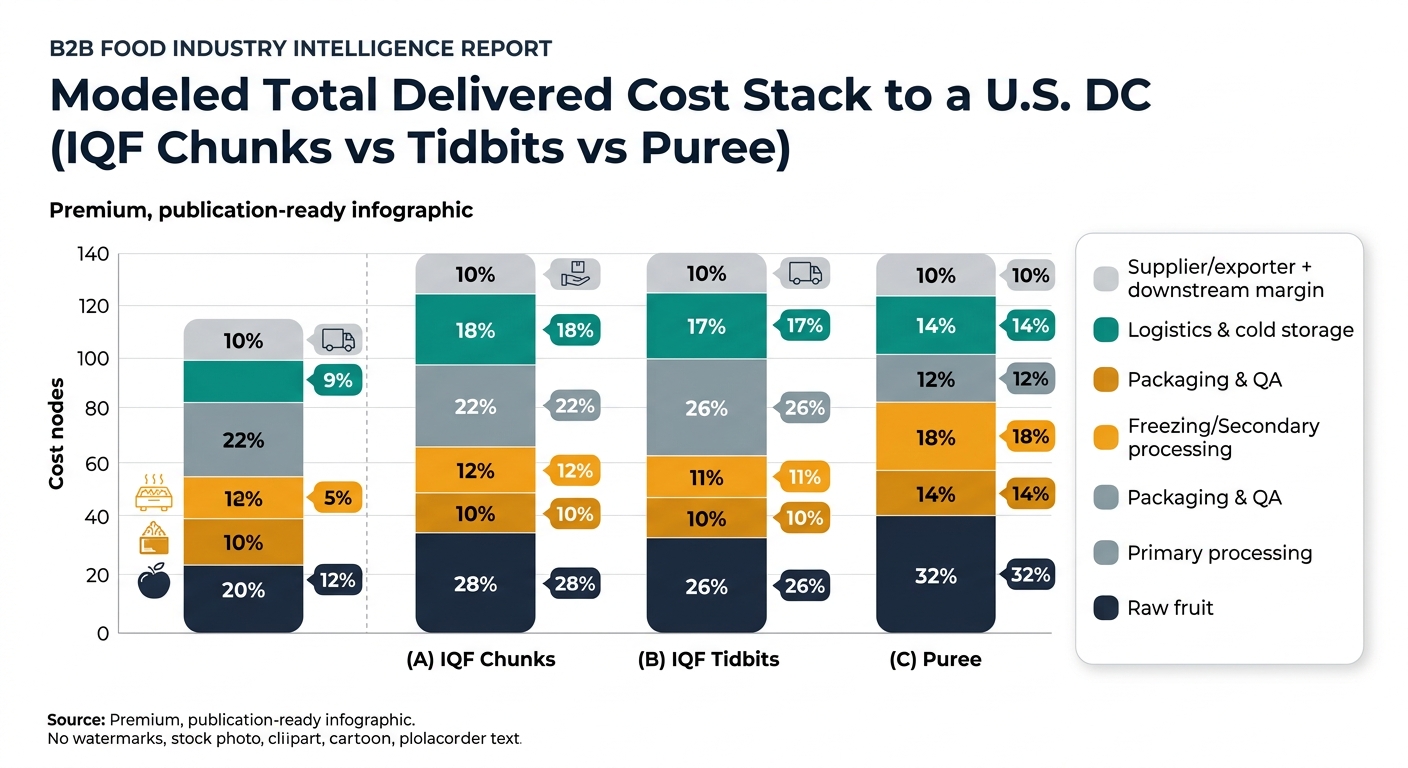

Modeled % of final delivered cost to a U.S. buyer DC. These are directional to show where cost concentrates; actual splits vary by origin, contract terms, seasonality, and spec.

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Raw fruit | 28% | Farmgate price, yield risk |

| Primary processing | 22% | Labor + trim loss from cut/spec |

| Freezing (IQF/block) | 12% | Energy + line utilization |

| Packaging & QA | 10% | Packaging inflation + testing/audit load |

| Logistics & cold storage | 18% | Reefer rates, port dwell, inventory time |

| Supplier/exporter + downstream margin | 10% | Financing, risk premium, channel power |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Raw fruit | 26% | Fruit size mix |

| Primary processing | 26% | Higher labor + yield loss |

| Freezing | 11% | Throughput constraints |

| Packaging & QA | 10% | Foreign-matter controls |

| Logistics & cold storage | 17% | Reefer + storage |

| Supplier/exporter + downstream margin | 10% | Risk premium |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Raw fruit | 32% | Competing demand (juice/puree) |

| Primary processing | 14% | Less cut precision, more bulk handling |

| Secondary processing | 18% | Thermal/processing + QA |

| Packaging & QA | 12% | Drums/totes, aseptic controls |

| Logistics & storage | 14% | Bulk freight + storage |

| Supplier/exporter + downstream margin | 10% | Financing + risk |

Key structural fact: In frozen pineapple, the constraint is often qualified processing capacity for your exact spec, not global pineapple production.

Procurement consequence: Over‑tight specs can unintentionally force single‑sourcing, increasing continuity risk.

Critical insight: Frozen pineapple pricing can disconnect from “pineapple market” headlines because the traded product is a bundle of yield + processing capacity + cold-chain logistics + QA risk.

Procurement takeaway: A “market-justified increase” is rarely explained by one variable. It’s usually a stack (yield + labor + energy + freight + QA).

This is not about “more data.” It’s about turning signals into sourcing actions that improve cost, continuity, and auditability.

Frozen pineapple is a clean example of a broader procurement truth: the “unit price” is the least stable part of the decision.

The transferable procurement capability is the same:

Frozen pineapple is an ideal “proof category” because it forces clarity on what procurement is accountable for:

If you can run frozen pineapple with disciplined intelligence—spec governance, portfolio resilience, and cost-driver negotiation—you can replicate the operating model across most frozen fruit and adjacent ingredients.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.