This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

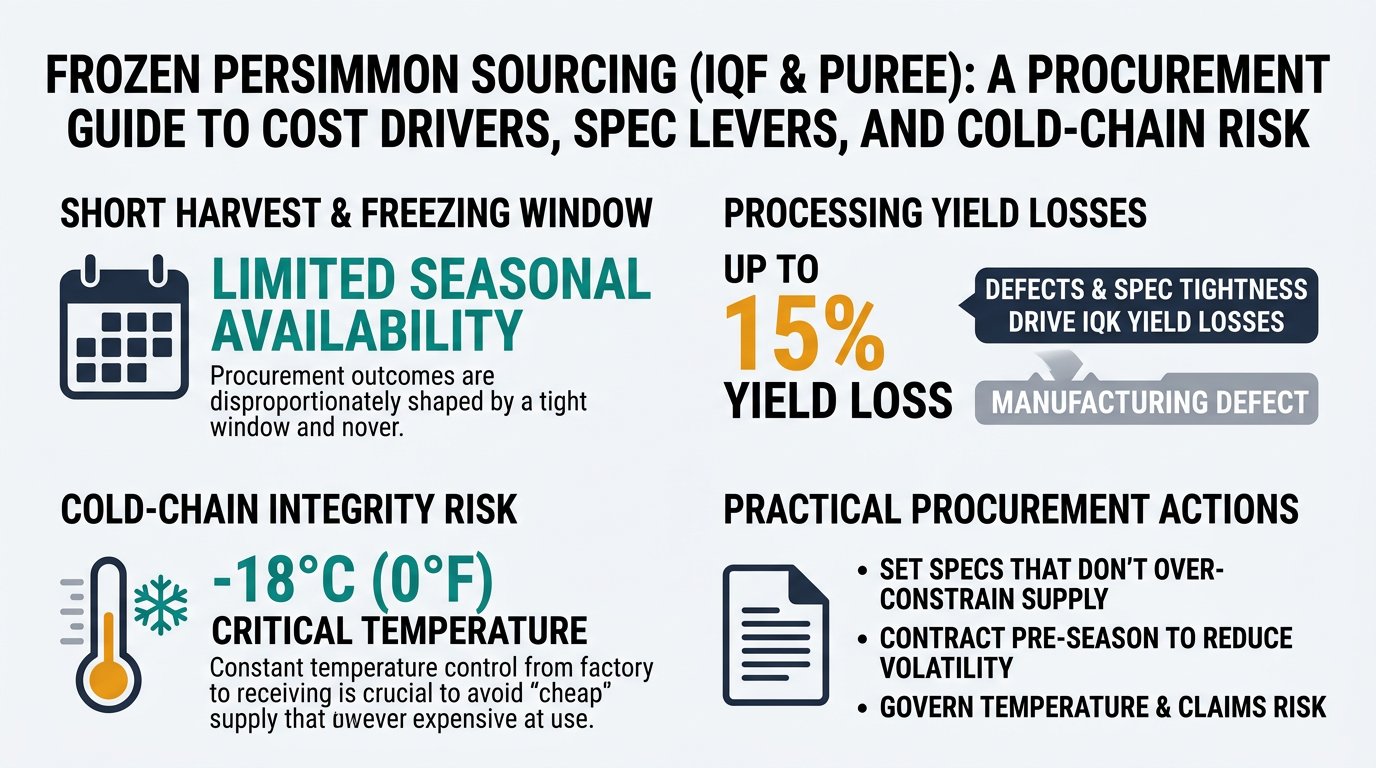

Frozen persimmon is a small, niche frozen-fruit category where procurement outcomes are disproportionately shaped by (1) a short harvest/freezing window, (2) processing yield losses driven by defects and spec tightness, and (3) cold-chain integrity from factory to receiving. This guide translates those realities into practical procurement actions—how to set specs that don’t over-constrain supply, how to contract pre-season to reduce volatility, and how to govern temperature and claims risk so “cheap” supply doesn’t become expensive at use.

(Analyzed at: Mar, 2026)

Frozen persimmon looks like “just another frozen fruit,” but procurement outcomes are disproportionately driven by raw-fruit seasonality + processing yield + cold-chain integrity.

Below are the cost accumulation points procurement can actually influence (via specs, contracting, and logistics terms).

Key insight: In frozen persimmon, the “raw fruit price” is only half the story—grade distribution and firmness/sugar suitability for IQF can change effective input cost more than the orchard price itself.

Key insight: This is the yield-loss engine of the category. Tight defect tolerances, peel removal requirements, and cut geometry (slice vs dice) can swing yield materially.

Key insight: The freezer is a capacity and energy bottleneck; when energy costs spike or IQF capacity is tight, IQF prices often move faster than puree.

Key insight: In niche frozen fruits, QA cost is partly “insurance.” Skimping here often reappears as downgrades, credits, and line disruptions.

Key insight: Reefer logistics is not just freight—it’s temperature integrity + dwell time + inventory carrying cost.

Key insight: For frozen persimmon, downstream margin often compensates for inventory risk and claims risk more than marketing spend.

These are modeled ranges to show where cost concentrates. Actual ratios vary by origin, crop year, pack format, and freight market. Use these as a negotiation “where to look,” not as a market benchmark.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream raw fruit | 30% | Grade suitability drives effective input cost |

| Primary processing | 20% | Peeling/cutting + yield loss + sorting intensity |

| Secondary processing | 18% | IQF energy + capacity constraints |

| Packaging & QA | 7% | Metal detection, micro, piece integrity checks |

| Logistics & distribution | 15% | Reefer + frozen storage + claims reserve |

| Wholesale/importer margin | 10% | Inventory risk + service buffering |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream raw fruit | 28% | Slightly more tolerance on appearance than slices |

| Primary processing | 22% | Dicing yield + size distribution sorting |

| Secondary processing | 17% | IQF + clump control |

| Packaging & QA | 7% | Size distribution + foreign material controls |

| Logistics & distribution | 16% | Similar cold-chain cost |

| Wholesale/importer margin | 10% | Similar risk premium |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream raw fruit | 25% | Can utilize more seconds if specs allow |

| Primary processing | 15% | Less cut labor; still sorting + peel/seed control |

| Secondary processing | 16% | Plate freezing + standardization (Brix/viscosity) |

| Packaging & QA | 10% | Higher QA for foreign material (sieving/metal detection) |

| Logistics & distribution | 18% | Heavy packs/drums; storage and handling add up |

| Wholesale/importer margin | 16% | Often higher due to financing and handling complexity |

If you manage frozen persimmon like a “monthly replenishment” item, you’ll overpay and under-serve.

Teams often ask: “Why did the persimmon quote rise when farmgate didn’t?” In frozen persimmon, the disconnect is usually yield + cold chain, not orchard pricing.

The decision you’re trying to make is usually one of these:

Frozen persimmon is a compact example of a broader procurement truth: in cold-chain agricultural ingredients, the biggest risks are often invisible in the PO price.

Frozen persimmon forces clarity on the fundamentals that separate reactive buying from category management:

If you can manage frozen persimmon with discipline—balancing spec governance, yield reality, and cold-chain execution—you can usually improve performance across the rest of your frozen fruit portfolio.

© Frozen Persimmon Sourcing Guide

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.