This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

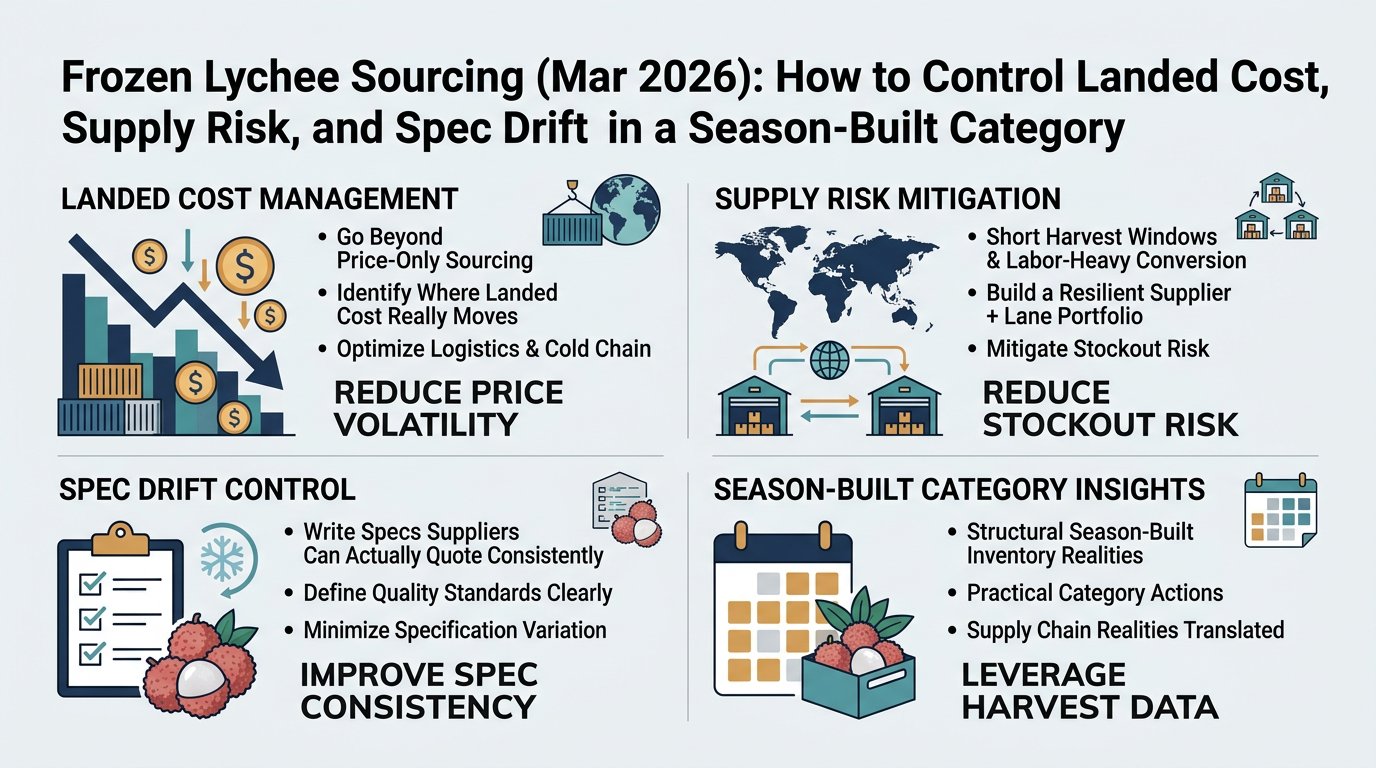

Frozen lychee is a deceptively small category that behaves like a “stress test” for procurement: short harvest windows, labor-heavy conversion, and cold-chain-dependent quality make price-only sourcing fragile. This guide translates frozen-lychee supply chain realities into practical category actions—how to write specs that suppliers can actually quote consistently, where landed cost really moves, and how to build a supplier + lane portfolio that reduces volatility and stockout risk.

(Analyzed at: Mar, 2026)

Frozen lychee is not “fresh lychee, just colder.” It is a time-compressed supply chain designed to beat lychee’s rapid post-harvest deterioration (browning, texture loss, flavor fade). The commercial reality is:

Procurement implication: The “right” supplier is the one whose capability matches your spec + lane + governance model—not the one with the lowest FOB on a single quote.

Below is an illustrative cost-and-margin decomposition. Use it as a negotiation and governance map (where to ask questions, where to audit, where to index), not as a universal truth.

Key insight: Frozen lychee cost starts with a seasonal raw fruit price spike concentrated into a short harvest window; in heavy crop years more fruit diverts to lower-value channels, but in tight years processors compete aggressively for suitable grades.

Seasonality anchor (planning reality): China’s harvesting season is concentrated within late May–early July (about 1.5 months) [1].

Key insight: This node determines the reject rate that later becomes your hidden cost (yield loss + more labor downstream).

Key insight: This is typically the highest conversion-cost step for IQF arils because it is labor-intensive and yield-sensitive.

Key insight: IQF isn’t just a format; it’s a performance promise (piece integrity, less clumping, better dosing in manufacturing). It usually costs more to produce but can reduce downstream handling loss.

Key insight: Packaging is where suppliers either protect you from claims—or create them.

Key insight: Reefer variability can erase a “good FOB” through temperature excursions, dwell time, and claim disputes.

Assumptions: Delivered cost to a North America/EU buyer; percentages vary by origin, season tightness, pack size, freight rates, and defect tolerance.

| Supply chain node | Cost ratio (% of final delivered cost) | What to watch in procurement |

|---|---|---|

| Raw fruit + aggregation | 30–40% | harvest window exposure; residue program; variety mix |

| Primary processing | 6–10% | reject rate transparency; pre-cool discipline |

| Secondary processing | 18–28% | labor throughput; seed fragment control; rework rate |

| Freezing (IQF) | 6–10% | freezer capacity utilization; piece integrity |

| Packaging & QA | 6–10% | lot coding; micro specs; packaging integrity |

| Logistics & cold storage | 12–18% | lane stability; reefer monitoring; dwell time |

| Importer/wholesale margin | 8–14% | service level, financing, compliance coverage |

| Supply chain node | Cost ratio (% of final delivered cost) | What to watch in procurement |

|---|---|---|

| Raw fruit + aggregation | 32–45% | same as above; grade flexibility can reduce cost |

| Primary processing | 6–10% | sorting standards (less strict than IQF in some cases) |

| Secondary processing | 12–20% | lower piece-integrity requirement but still FM risk |

| Freezing (block) | 4–8% | core freezing time; block size consistency |

| Packaging & QA | 5–9% | block liners; thaw/leak risk |

| Logistics & cold storage | 12–18% | pallet stability; temperature controls |

| Importer/wholesale margin | 8–14% | similar service economics |

| Supply chain node | Cost ratio (% of final delivered cost) | What to watch in procurement |

|---|---|---|

| Raw fruit + aggregation | 25–38% | ability to use lower-grade fruit can buffer shortages |

| Primary processing | 6–10% | sanitation and wash controls |

| Secondary processing (pulping/finishing) | 15–25% | particle size, brix/acid targets, oxidation control |

| Freezing | 5–9% | freeze curve for drums; uniformity |

| Packaging & QA | 7–12% | drum liners, seals, sampling plans |

| Logistics & cold storage | 12–20% | drum handling damage; warehouse capability |

| Importer/wholesale margin | 8–14% | documentation + service levels |

Because major origins have tight harvest windows (for China, concentrated late May–early July), the market is structurally forced into:

Procurement consequence: Spot buying in the “wrong month” often means you’re buying from:

In frozen lychee, price doesn’t move as a single line item. It moves as three interacting systems:

Practical takeaway: Two suppliers quoting the same FOB can produce very different true landed cost once you include:

Below is how an intelligence-driven service changes decisions—mapped to a category manager’s real workflows.

Decision shift: From “negotiate FOB” → to “negotiate the right cost drivers.”

Outcome you can measure: Reduced landed-cost volatility (variance) and fewer surprise surcharges.

Decision shift: From “lowest quote shortlist” → to “risk-adjusted shortlist.”

Benchmark suppliers on:

Outcome you can measure: Higher first-pass qualification rate (fewer failed samples / fewer re-audits).

Decision shift: From “react after shortage” → to “trigger early qualification and buffers.”

Outcome you can measure: Fewer stockouts and fewer emergency buys/premium freight events.

Frozen lychee is a clean example of a broader procurement pattern: when quality and logistics are inseparable, price-only sourcing fails.

Similar dynamics show up in:

Meta-lesson: Intelligence is most valuable where your category has:

Frozen lychee forces good procurement behavior because it makes trade-offs visible:

If a team can run frozen lychee with disciplined intelligence—supplier benchmarking, landed-cost decomposition, and trigger-based risk monitoring—the same operating model typically transfers well to other frozen fruits and cold-chain ingredients.

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.