This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

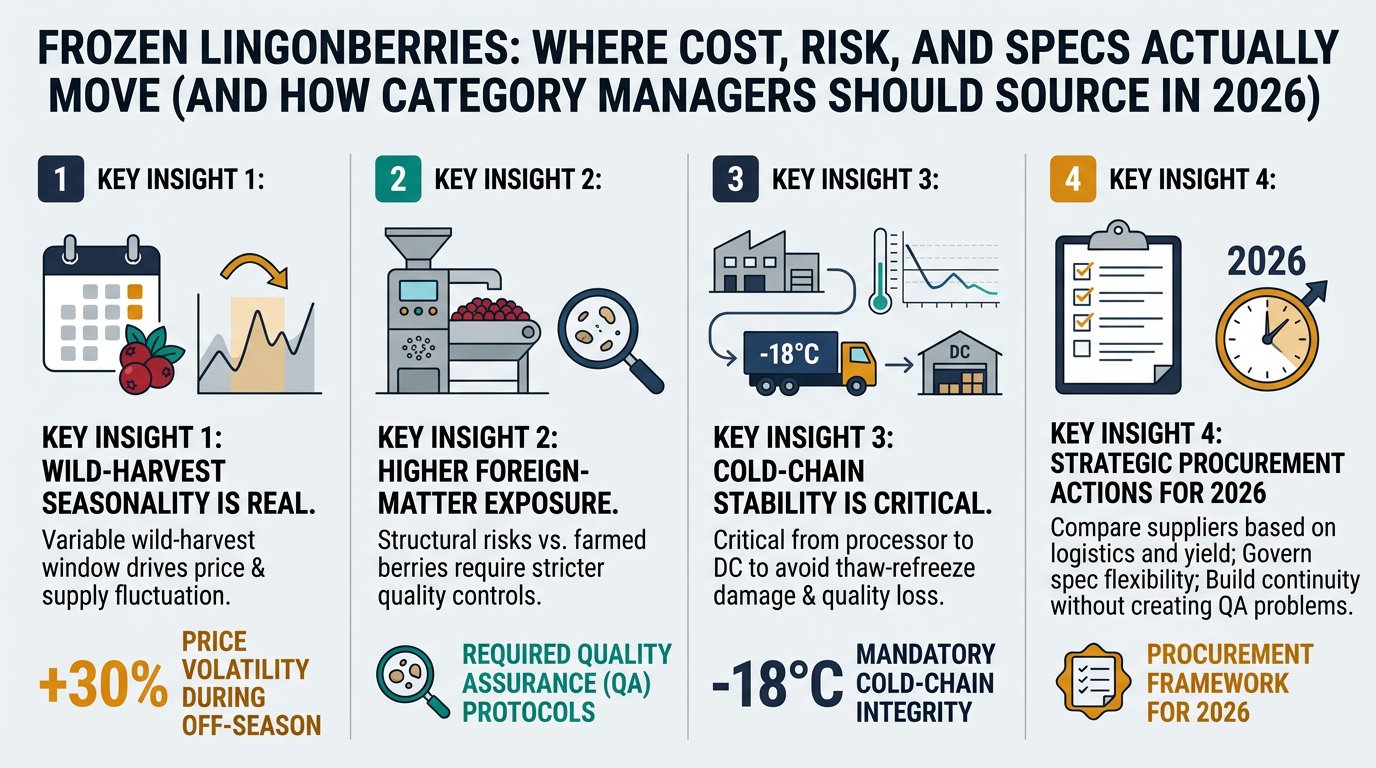

Frozen lingonberries look like a simple frozen fruit SKU, but the buying decision is really about controlling three things that drive total cost-to-serve: (1) a short, variable wild-harvest window, (2) structurally higher foreign-matter exposure vs. farmed berries, and (3) cold-chain stability from processor to your DC. This guide translates those realities into practical procurement actions—how to compare suppliers, govern spec flexibility, and build continuity without creating QA or claims problems.

(Analyzed at: Mar, 2026)

Frozen lingonberries look like a simple SKU (IQF berry in a bag). In reality, you’re buying the outcome of a short, variable wild-harvest window, plus a foreign-matter-intensive intake stream, plus a cold-chain that must stay stable around -18°C end-to-end to preserve quality and prevent claims. [1]

Key insight: In frozen lingonberries, raw berry economics and pack-out yield dominate upstream cost, while energy + cold storage + logistics + working capital dominate downstream cost. The “cheapest” quote often becomes expensive once you price in claims, yield loss, and service failures.

Modeled % of final delivered cost to your DC (not consumer retail price). These are directional to show where cost concentrates; actuals vary by origin, crop year, spec tightness, and lane. Use these as a negotiation framework, not as “market facts.”

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most |

|---|---|---|

| Upstream raw berries (wild collection) | 35% | crop size, picker costs, quality deductions |

| Primary processing & freezing | 25% | sorting intensity, energy, pack-out yield |

| Packaging & QA | 10% | testing plan, traceability, defect tolerances |

| Cold storage + logistics | 20% | reefer rates, dwell time, lane reliability |

| Importer/distributor margin | 10% | service levels, repack needs |

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most |

|---|---|---|

| Upstream raw berries | 40% | raw price swings in short harvest window |

| Primary processing & freezing | 18% | less sorting vs IQF, freezing efficiency |

| Packaging & QA | 7% | simpler packs, sometimes lighter QA |

| Cold storage + logistics | 22% | same cold-chain realities still apply |

| Importer/distributor margin | 13% | consolidation, credit terms |

| Supply Chain Node | Cost Ratio (% of Final Cost) | What moves it most |

|---|---|---|

| Raw fruit inputs (multiple) | 30% | relative pricing of component berries |

| Primary processing & freezing | 15% | component specs and yield |

| Secondary processing (blending/rework) | 18% | handling steps, clumping control |

| Packaging & QA | 10% | labeling governance, lot integrity |

| Cold storage + logistics | 17% | extra handling risk |

| Importer/distributor margin | 10% | private label requirements |

Key structural fact: Lingonberry supply behaves less like a farmed commodity and more like a wild-crop availability market. That means:

Implication for category managers: your leverage comes from pre-qualification, spec governance, and allocation strategy, not last-minute RFQ pressure.

Frozen lingonberry pricing can diverge from your “expected” berry inflation because the biggest hidden drivers are:

This is not about “more data.” It’s about making the next decision (renew/allocate/qualify/spec-change) with fewer blind spots.

Use supplier benchmarking to normalize:

Output you can actually use: a one-page comparability table that shows where “cheaper” product is likely to create downstream cost.

Use substitution mapping + governance tracking to define:

Use supplier discovery + risk watchlists to:

The same intelligence pattern applies to other “looks-like-a-commodity” categories where spec + process controls drive true cost:

The general rule: if a category has high seasonality, variable raw quality, and cold-chain dependence, procurement wins come from governed flexibility + qualified alternates, not just harder negotiation.

Frozen lingonberries are a strong “proof category” because outcomes are visible quickly:

If you can’t measure at least claims + OTIF + hold rate by supplier, you’re negotiating blind—especially in wild-harvest berries.

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.