This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

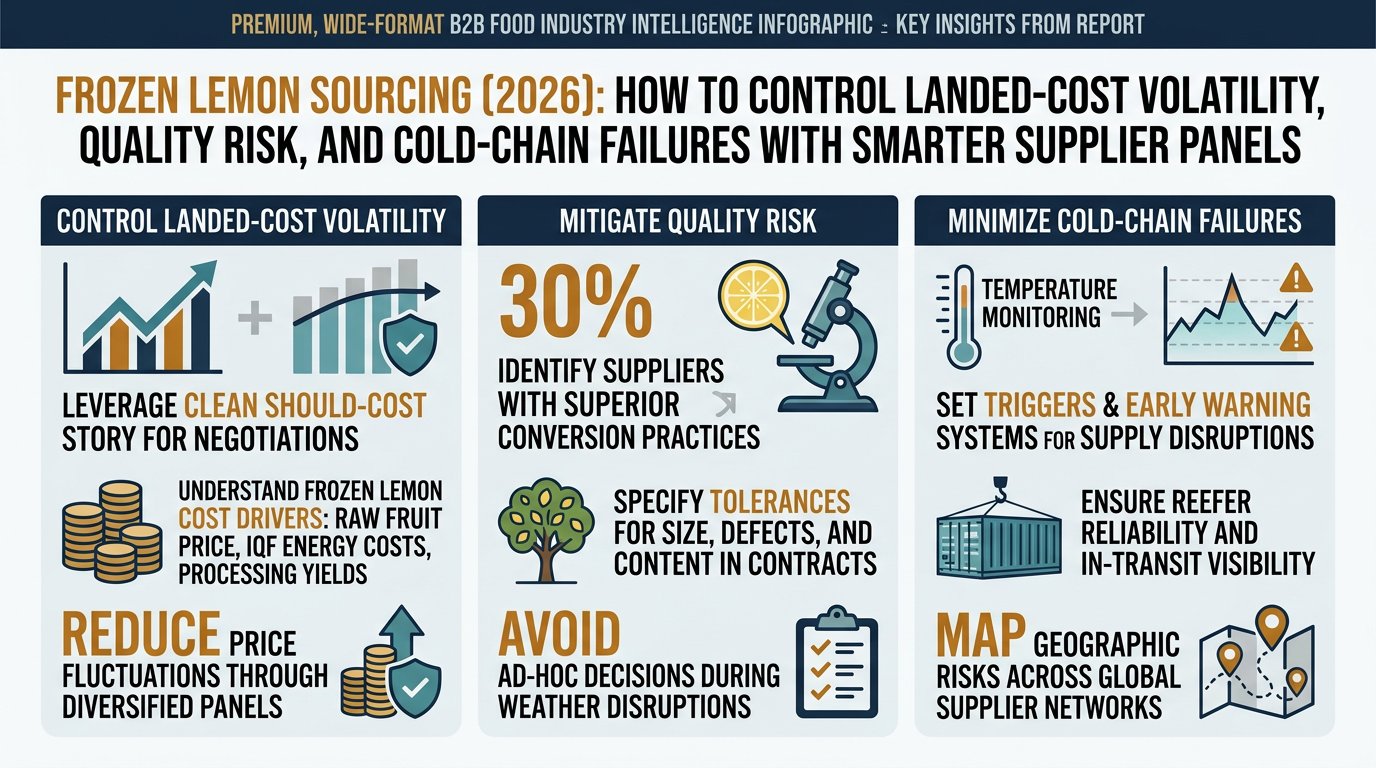

Frozen lemon is a deceptively complex category: it behaves like a fresh commodity (seasonal, weather-sensitive), but it’s priced and operationalized like a conversion + cold-chain product (cut/yield, IQF energy, reefer reliability). This guide is written for experienced procurement/category managers who know sourcing—but want a practical, frozen-lemon-specific playbook for building a resilient supplier panel, negotiating with a clean should-cost story, and setting triggers before disruptions force bad decisions.

(Analyzed at: Mar, 2026)

Frozen lemon (slices, wedges, diced, IQF pieces, zest/peel, puree/pulp, and sometimes juice/concentrate inputs) is not just “lemons, frozen.” It’s a chain where fresh-market dynamics, yield loss during cutting, energy-intensive freezing, and cold-chain reliability decide your true landed cost and service performance.

Origin concentration is real. Large lemon-producing countries include Mexico, Turkey, Argentina, and others; global citrus statistics and USDA/FAS reporting show these origins are consistently material in supply availability and trade context. [2]

Below is a practical “cost stack” view. The point isn’t precision to the decimal—it’s to show which levers move your landed cost and which ones mainly create risk.

Key insight: Your frozen price often starts with a fresh-market competition problem. When fresh lemon prices rise, processors must pay more to secure fruit (or get smaller/less suitable fruit), which tightens frozen availability and pushes offers up.

What drives cost here:

Procurement “tell” that upstream is driving the move:

Key insight: This is where specs become money. Tight cut-size tolerances, low seed counts, and low defect tolerances increase labor, rework, and yield loss.

Cost drivers:

Hidden margin dynamic:

Key insight: IQF is an energy + equipment utilization business. When energy costs rise or lines run below capacity, unit costs jump.

Cost drivers:

Quality risk linkage:

Key insight: Packaging is not “just packaging” in frozen lemon. It’s protection against dehydration and a compliance layer for audits and claims.

Cost drivers:

Compliance reality:

Key insight: Cold-chain logistics can dominate delivered cost volatility even when ex-works pricing is stable.

Cost drivers:

Why you should treat this as a separate negotiation lane:

Key insight: The last margin layer is where volatility becomes visible to stakeholders (“why did our case cost jump?”). If you don’t separate commodity vs. conversion vs. cold-chain drivers, approvals get political.

Cost drivers:

Modeled ranges as % of final delivered cost to your dock. Real ratios vary by origin, contract structure (FOB/CIF/DDP), pack size, and service model.

| Supply Chain Node | Cost Ratio (% of Final Delivered Cost) | What Usually Moves It |

|---|---|---|

| Upstream raw lemons | 25–40% | Fresh-market pull, weather/yield |

| Primary processing (cut/de-seed/sort) | 15–25% | Spec tightness, labor, yield loss |

| Secondary processing (IQF + FM control) | 10–20% | Energy, utilization, rework |

| Packaging & QA | 6–12% | Barrier materials, testing regime |

| Cold-chain logistics & distribution | 12–25% | Reefer rates, dwell, cold storage |

| Trade + importer/distributor margin | 8–18% | Financing, service model |

| Supply Chain Node | Cost Ratio (% of Final Delivered Cost) | What Usually Moves It |

|---|---|---|

| Upstream raw lemons | 25–45% | Fruit price and availability |

| Primary processing | 12–22% | Cut size tolerance, defect sorting |

| Secondary processing | 10–18% | Energy and throughput |

| Packaging & QA | 5–10% | Bulk liners/cartons, COA |

| Cold-chain logistics & distribution | 10–22% | Reefer + cold store |

| Trade + margin | 8–15% | Channel structure |

| Supply Chain Node | Cost Ratio (% of Final Delivered Cost) | What Usually Moves It |

|---|---|---|

| Upstream raw lemons | 20–35% | Peel oil content, fruit availability |

| Primary processing | 18–30% | Zesting method, contamination control |

| Secondary processing | 8–15% | Freezing + sieving |

| Packaging & QA | 6–12% | Specialty packaging, testing |

| Cold-chain logistics & distribution | 10–20% | Cold chain |

| Trade + margin | 10–20% | Specialty ingredient markups |

Frozen lemon is a “conversion + cold-chain” category built on a fresh commodity base.

That means your price and availability are a composite of:

So two suppliers can quote the same CFR price but deliver radically different outcomes because:

Category teams often expect frozen lemon to track “lemon prices.” In practice, the linkage is lagged and filtered.

These are the repeatable failure modes I see when a team is strong in other categories but new to frozen lemon.

This is not about “more data.” It’s about changing Monday-morning decisions: who is on panel, what you negotiate, and when you switch volume.

Capability used: Supplier discovery + supplier benchmarking

Capability used: Price intelligence + cost driver tracking

Capability used: Supply chain risk monitoring + alternative supplier identification

Capability used: Procurement performance & governance analytics

Frozen lemon is a clean example of a broader procurement pattern: commodity base + conversion step + logistics constraint + compliance risk.

Similar logic shows up in:

The transferable procurement habit is: don’t source the product—source the risk-adjusted outcome.

Frozen lemon is “small enough” to pilot quickly but “complex enough” to prove value.

It forces the right behaviors:

And it produces measurable outcomes within one or two buying cycles:

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.