This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

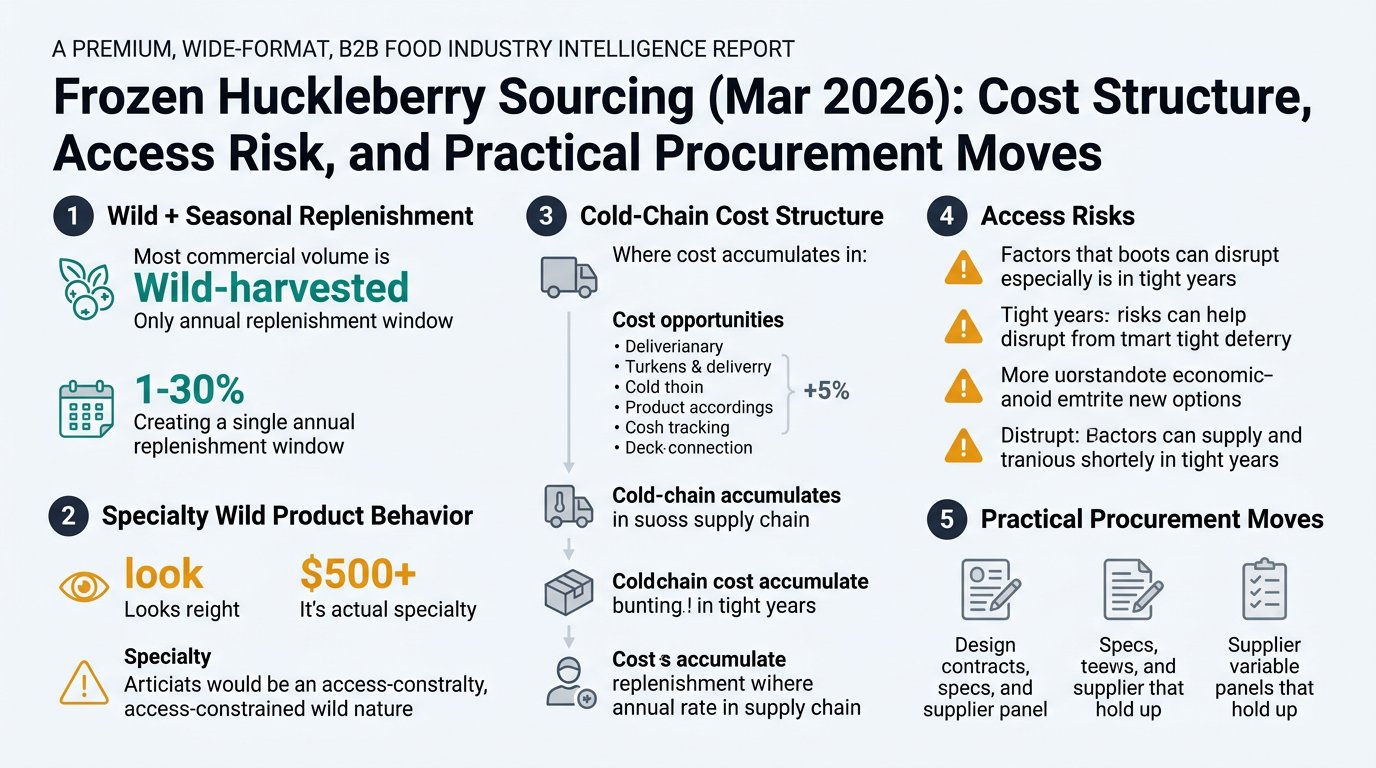

Frozen huckleberries look familiar (they’re “just another berry”), but they behave like a specialty, access-constrained wild product with a cold-chain cost structure. This guide translates that reality into procurement language—what you’re really buying, where cost accumulates, what can disrupt supply, and how to design contracts, specs, and supplier panels that hold up in tight years.

Analyzed at: Mar, 2026

Frozen huckleberries are not a “normal berry” supply chain.

Practical implication for Purchase – Product & Category Management: in tight years, the negotiation often flips from price-first to allocation-first (who will commit volume at your spec, with traceability and QA gates intact).

Key insight: In frozen huckleberries, cost is structurally concentrated in hand harvest + yield loss + freezing/cold storage. That makes prices less responsive to “standard” procurement levers (e.g., adding more suppliers quickly) because the upstream is capacity- and access-constrained.

Reference point: USDA AMS frozen blueberry grade standards explicitly describe frozen blueberries as cleaned and stemmed, and note they include Vaccinium species “often called huckleberries” (with exclusions), showing how “cleanliness/defect” is embedded into grading logic and cost [4].

A practical benchmark from a UMass frozen-produce cost study: energy (gas + electricity) can represent ~46% of utility expenses for freezing operations. (Treat as directional; plant designs and energy tariffs vary.)

Frozen berry food-safety scrutiny is real: FDA has communicated findings from sampling where genetic material from hepatitis A virus and norovirus was detected in some frozen berry samples, and notes that freezing generally does not kill viruses—reinforcing why buyers emphasize preventive controls and supplier governance [3].

Cold storage energy is often the dominant operating load: refrigeration is commonly cited as ~70–80% of cold storage energy costs (facility dependent), which is why energy volatility transmits into frozen fruit landed cost [2].

These are modeled ratios to show where cost concentrates; actuals vary by origin, pack format, Incoterms, audit requirements, and crop conditions. Use these as a negotiation “map” (what’s structurally sticky vs what’s commercially movable), not as a universal should-cost.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream raw (wild harvest + aggregation) | 38% | Labor + access constraints dominate |

| Primary processing (clean/sort/destem) | 16% | Yield loss increases with tight specs |

| Secondary processing (IQF freezing) | 14% | Energy + utilization sensitivity (directional) |

| Packaging & QA | 10% | Retail/brand documentation adds cost; virus-risk governance is a driver [3] |

| Logistics & cold storage | 12% | Refrigeration + reefer trucking volatility [2] |

| Channel margin | 10% | Service level + allocation premium |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream raw | 42% | Same structural constraint upstream |

| Primary processing | 14% | Somewhat lower rework intensity |

| Secondary processing (block freezing) | 9% | Lower unit cost than IQF |

| Packaging & QA | 7% | Bulk packs |

| Logistics & cold storage | 14% | Storage still significant [2] |

| Channel margin | 14% | Often sold through fewer, specialized channels |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream raw | 30% | Can use more mixed/broken grade |

| Primary processing | 12% | Still needs FM control |

| Secondary processing (formulation + freezing) | 18% | Sugar + mixing + additional handling |

| Packaging & QA | 10% | Labeling, allergen/ingredient controls |

| Logistics & cold storage | 12% | Frozen distribution [2] |

| Channel margin | 18% | Value-added convenience premium |

Frozen huckleberry behaves less like a globally traded commodity and more like a managed wild resource.

Procurement takeaway: treat huckleberry as a category where policy and access risk sits alongside weather and logistics risk.

Buyers often expect a simple linkage: “if raw prices soften, my IQF price should drop quickly.” In frozen huckleberry, that linkage breaks for four reasons:

If you’re making one of these decisions—panel refresh, contract renewal, backup qualification, or allocation planning—intelligence changes outcomes by reducing the two biggest uncertainties: who can truly supply your spec and what will disrupt supply before you can react.

What changes your decision:

Outcome you can measure: higher “spec coverage” across your panel (less single-supplier dependency for the tightest SKU).

What changes your decision:

Why it matters: access policy can be a binary shock (permit available vs not), which is different from gradual agronomic shifts [1].

What changes your decision:

Outcome you can measure: faster time-to-switch (weeks instead of months) when allocation tightens.

Frozen huckleberry is an extreme case of a broader procurement pattern: when upstream is constrained and quality is fragile, intelligence beats negotiation tactics alone.

Because it forces clarity on the four procurement truths that matter in most “difficult” categories:

If you can run frozen huckleberry with stable service levels, controlled QA risk, and fewer in-season surprises, you can apply the same intelligence-led discipline across your broader frozen fruit and specialty ingredient portfolio.

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.