This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

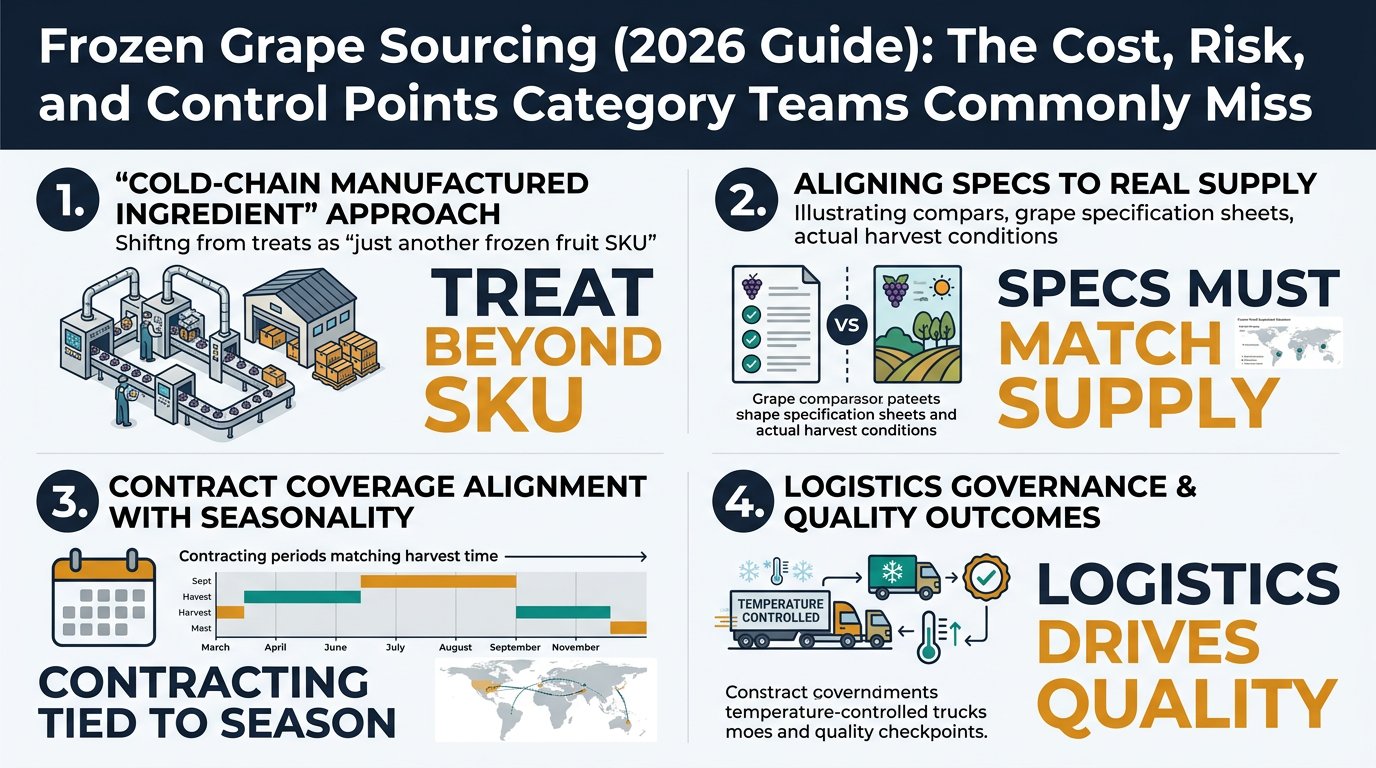

Frozen grapes are easy to treat like “just another frozen fruit SKU,” but buyers who win this category manage it more like a cold-chain manufactured ingredient: they align specs to real supply, contract coverage to seasonality, and logistics governance to quality outcomes. This guide translates frozen-grape supply chain mechanics into the procurement decisions you actually own—supplier portfolio design, contracting/coverage, spec governance, lane strategy, and contingency planning.

Frozen grapes look like a simple commodity, but the supply chain behaves like a cold-chain manufactured ingredient with a farm input.

Below is a practical cost-and-margin view you can use to sanity-check supplier quotes and to frame negotiations around real drivers.

Key insight: Frozen-grape input cost is anchored to the fresh table grape market more than most buyers model.

Key insight: This node determines your true yield and your foreign material/defect risk.

Key insight: Frozen grapes are not “just frozen fruit”—they’re a throughput-constrained, energy-intensive manufactured output.

When energy costs spike or capacity tightens, suppliers protect margin by:

Key insight: Packaging is often the second-largest controllable cost after raw fruit for retail formats.

Key insight: Logistics is where “cheap product” becomes expensive through temperature risk, demurrage, and inventory carrying cost.

Key insight: The downstream margin stack is strongly influenced by who holds:

Modeled % of final delivered cost to your DC (not shelf price). Ratios vary by origin, pack format, contract terms, and freight market.

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Raw grapes | 35% | fresh market pull; defect/yield variability |

| Primary processing | 12% | sorting intensity; stem/defect removal |

| Secondary processing (IQF) | 18% | energy; freezer capacity utilization |

| Packaging & QA | 15% | film/carton costs; testing cadence |

| Logistics & cold storage | 20% | reefer rates; cold-store days; demurrage |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Raw grapes | 40% | fruit price and diversion availability |

| Primary processing | 14% | defect rate; sorting yield |

| Secondary processing (IQF) | 20% | energy and throughput |

| Packaging & QA | 6% | liners/cartons; fewer retail materials |

| Logistics & cold storage | 20% | lane selection; cold-store time |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Raw grapes | 30% | ability to use lower-grade fruit |

| Primary processing | 10% | wash/sort requirements |

| Secondary processing (crush/pasteurize/freeze) | 25% | energy + processing inputs |

| Packaging & QA (pails/drums) | 10% | packaging spec; aseptic/frozen handling |

| Logistics & cold storage | 25% | weight/handling; cold-store dwell |

Frozen-grape pricing often lags farm conditions—until it doesn’t.

Below are two high-leverage capability pairings that map to real buyer decisions.

Use capabilities:

How decisions shift:

What it cannot do:

Use capabilities:

How decisions shift:

What it cannot do:

Frozen grapes behave like other categories where processing capacity + cold chain + specs create hidden constraints:

The transferable lesson: category performance is a system outcome, not a unit-price outcome.

Frozen grapes compress multiple procurement challenges into one category:

If you can run frozen grapes with driver-based pricing, lane-aware service control, and spec-flex governance, you can typically apply the same operating model across a broad set of frozen and refrigerated categories.

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.