This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Procurement teams don’t win frozen-date sourcing by “beating up unit price.” They win by controlling two variables that create most surprises: usable yield (defects, pit fragments, moisture/texture) and cold-chain integrity (temperature stability from plant to your dock). This guide translates those realities into procurement artifacts—spec sheets, scorecards, portfolio splits, and contract clauses—so you can reduce landed-cost variance, shorten disruption response time, and make supplier awards more defensible with QA/Ops/Finance.

(Analyzed at: Mar, 2026)

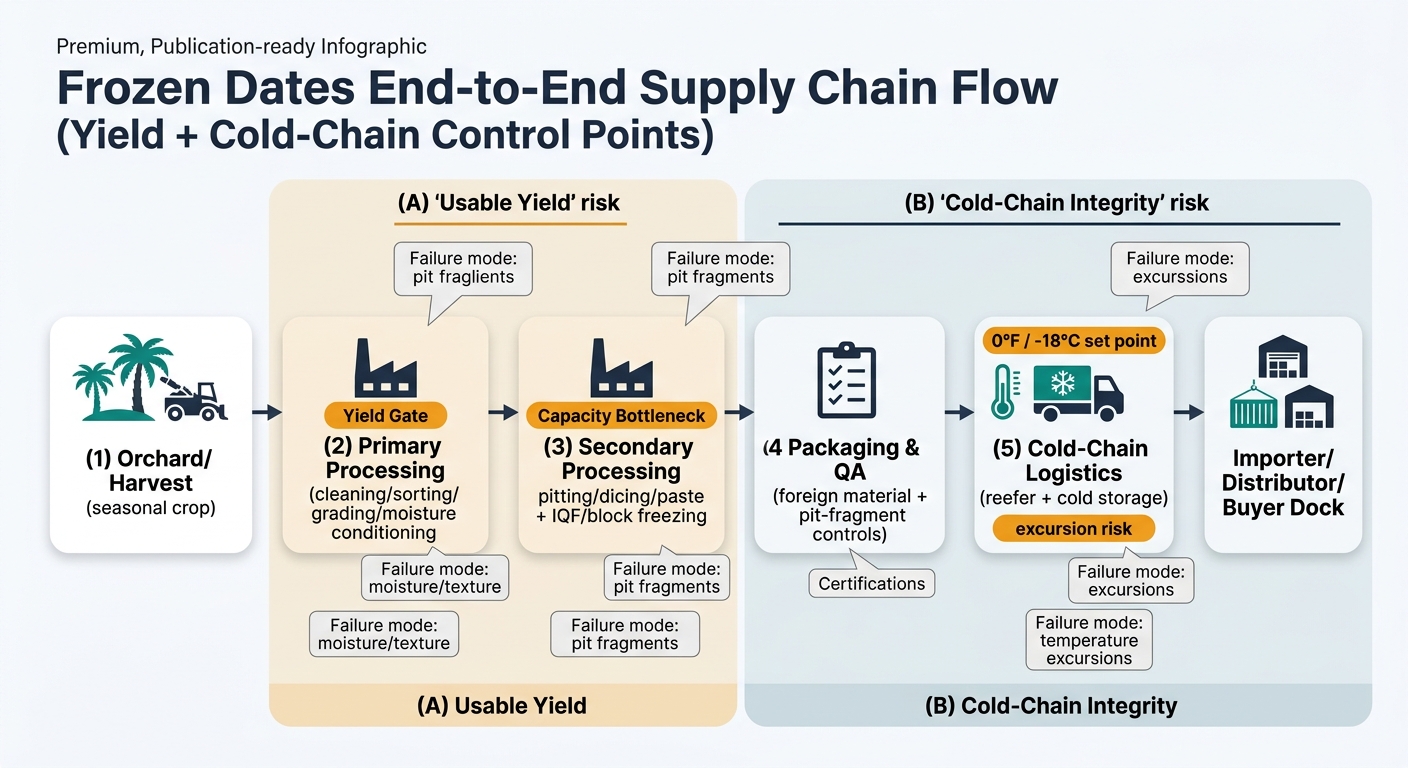

Frozen dates are not “just another dried fruit.” They sit between a highly seasonal orchard crop and a cold-chain-dependent ingredient. That means procurement outcomes are driven as much by pack-out yield, processing capability, and cold-chain discipline as by farmgate price.

Key insight: In frozen dates, the biggest procurement mistake is treating quotes as if they reflect only raw material. In practice, sorting losses + processing + cold chain can be the difference between a stable contract and a year of claims/expedites.

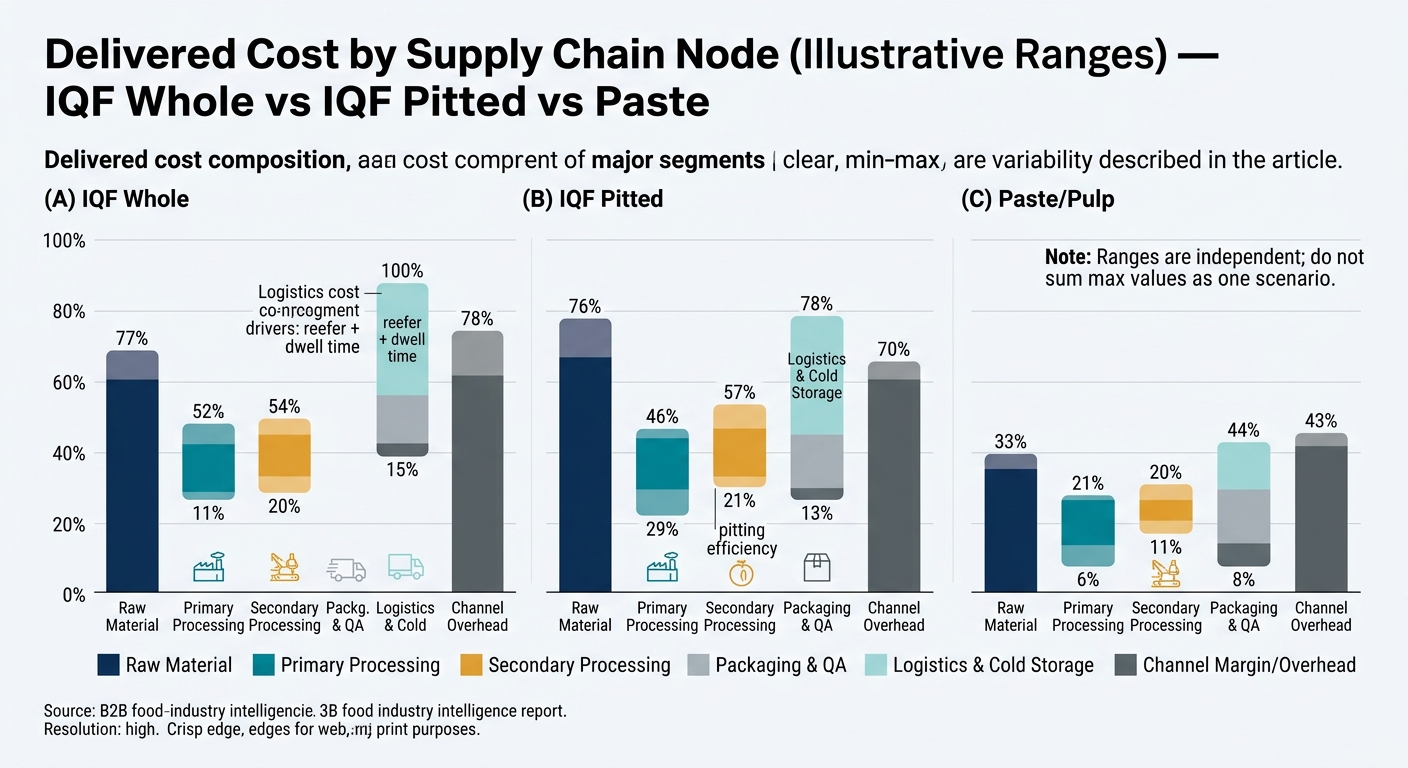

Below is a practical cost-and-margin walkthrough by node. Percentages are illustrative ranges to show where cost concentrates; actuals vary by origin, spec tightness, certifications, and Incoterms.

Modeled to show relative cost concentration by product form. Use this as a negotiation and should-cost structure, not as a price forecast.

| Supply Chain Node | Cost Ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Raw material | 35–50% | crop quality, variety, size/defect spec |

| Primary processing | 10–18% | sorting intensity, yield loss |

| Secondary processing (freezing) | 12–20% | energy, tunnel/IQF capacity |

| Packaging & QA | 6–10% | barrier materials, foreign-material controls |

| Logistics & cold storage | 12–22% | reefer rates, port dwell, cold storage |

| Channel margin/overhead | 8–15% | inventory carry, service level |

| Supply Chain Node | Cost Ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Raw material | 30–45% | pack-out and pitting suitability |

| Primary processing | 10–18% | defect removal, moisture conditioning |

| Secondary processing (pitting + freezing) | 18–28% | pitting efficiency, pit-fragment rejects |

| Packaging & QA | 6–12% | pit-fragment controls, QA testing |

| Logistics & cold storage | 10–20% | reefer/cold storage volatility |

| Channel margin/overhead | 8–15% | inventory financing |

| Supply Chain Node | Cost Ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Raw material | 25–40% | input grade, sweetness/moisture targets |

| Primary processing | 8–15% | cleaning, defect removal |

| Secondary processing (milling/blending + freezing) | 20–35% | throughput, energy, formulation consistency |

| Packaging & QA | 6–12% | pails/cartons, micro specs |

| Logistics & cold storage | 10–18% | reefer + destination storage |

| Channel margin/overhead | 8–15% | service model |

Key structural fact: Your true cost is driven by effective yield delivered to your line and temperature stability, not by the supplier’s ex-works price.

What this means in procurement terms:

Many buyers cannot “flex” specs quickly because QA approvals and customer labels lock parameters (moisture, cut size, variety claims, organic/halal).

Critical insight: Frozen-date pricing can lag or diverge from raw-date market moves because processing capacity, energy, and cold-chain costs behave like separate markets.

So the buyer decision is not “is the crop up or down?” It’s “what’s happening to yield + freezing + reefer lanes + inventory positions?”

Procurement teams coming from shelf-stable categories often make predictable errors:

Buyer decision (one sentence): “How do I award and contract frozen dates so I reduce landed-cost variance and disruption exposure while staying within QA and operational constraints?”

Dual-sourcing and tighter governance add overhead (trials, MOQ test orders, more supplier management), but reduce expected disruption cost.

The same intelligence pattern (yield + processing bottlenecks + logistics constraints) shows up in other procurement-managed ingredients:

If your organization is building a procurement intelligence muscle, frozen dates are a strong “training ground” because they force cross-functional alignment between Procurement, QA, Ops, and Logistics.

If you want, share four inputs—(1) form (IQF/paste/blocks), (2) must-have specs, (3) top two origins/lane split %, (4) biggest pain (cost variance vs stockout vs quality holds)—and I can translate this into a one-page award recommendation template (scorecard + portfolio split + contract posture).

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.