This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Frozen bone-in pork can look like a straightforward commodity buy, but procurement outcomes are usually driven by a few repeatable “gotchas”: spec non-comparability (bone/trim/pack), plant & market eligibility, and cold-chain execution (dwell time, reefer availability, temperature integrity). This guide translates those realities into decision-ready actions—how to structure specs, build backup coverage, time/shape contracts, and govern supplier concentration so you avoid expensive surprises.

(Analyzed at: Mar, 2026)

Frozen bone-in pork looks like a simple commodity SKU. In practice, it’s a cold-chain, plant-eligible, spec-sensitive product where small mismatches (cut style, trim, pack, labeling, eligibility) create big differences in yield, claims risk, lead time, and true landed cost.

Here’s the ground-truth flow most procurement teams are implicitly relying on:

Key buyer reality: your biggest controllable levers are usually (a) spec discipline, (b) plant/origin optionality, (c) contract structure + timing, (d) logistics design, not just supplier unit price.

Key insight: Hog/carcass cost moves with feed and herd economics, but cut prices don’t move evenly—they move based on whole-carcass balancing and demand for each primal.

Key insight: A “bone-in ham” is not just one thing—cut style + trim + bone content changes yield, carton count, and downstream labor.

Market structure signal you can use: USDA’s pork cutout methodology aggregates values from major primal components (e.g., belly, butt, ham, loin, picnic, rib) into a carcass cutout view; those component shares and values can shift quickly with demand. [1]

Key insight: Freezing is not “just a step”—it’s a working-capital and quality step. Longer freeze-to-ship cycles increase inventory financing and exposure to temperature excursions.

Key insight: In frozen bone-in pork, documentation failures (labeling, eligibility, traceability gaps) can be as costly as quality failures because they create holds, re-export, or forced discounting.

Key insight: Cold chain is a cost amplifier. Refrigerated warehousing is structurally energy-intensive; refrigeration frequently represents the majority share of cold storage electricity/energy cost, which helps explain why landed logistics can stay “sticky” even when raw material eases. [5]

Key insight: The “cheapest” supplier can become the most expensive when you add claims, trim variance, and service failures—especially for bone-in cuts where spec variance is common.

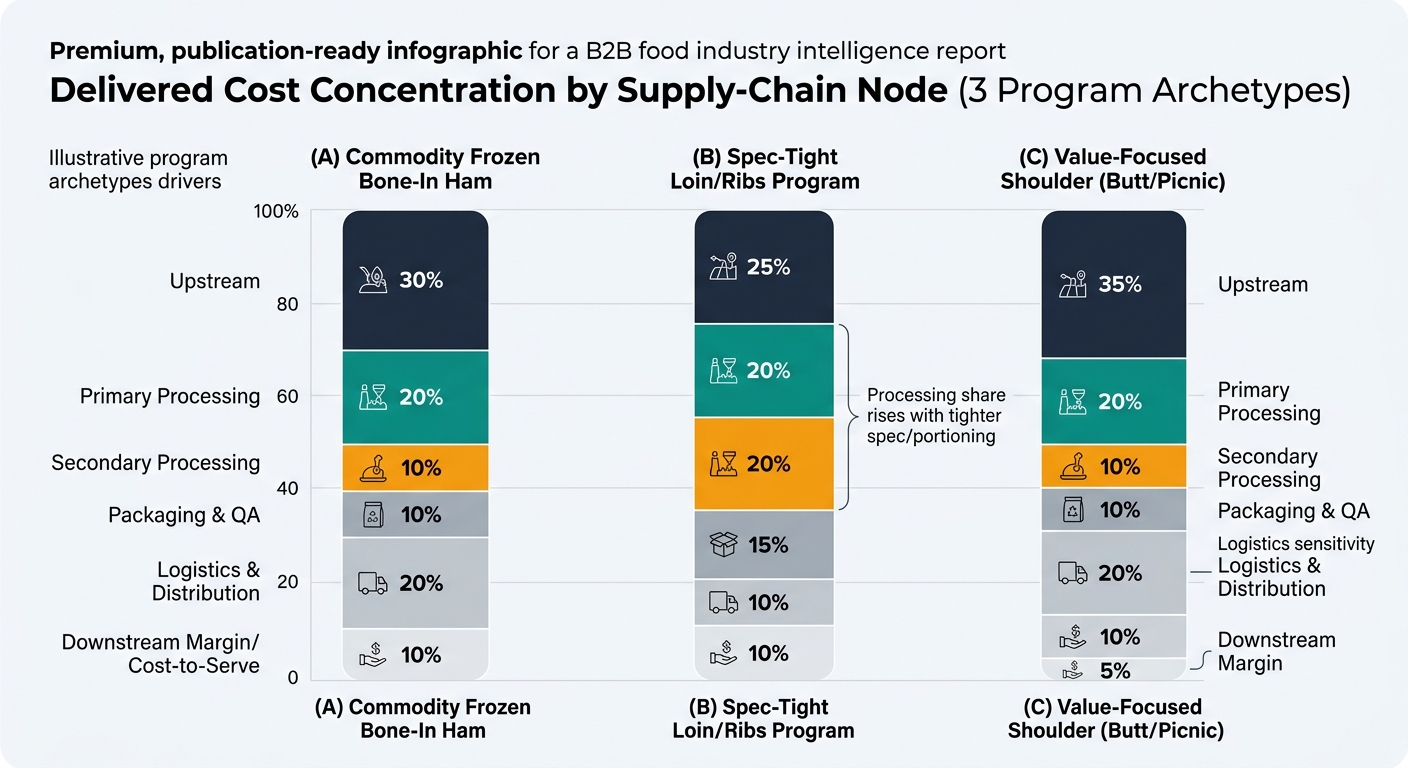

Modeled to show where cost tends to concentrate for frozen bone-in pork programs. Actual ratios vary by origin, incoterms, freight market, and spec.

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Upstream (hog/carcass) | 50% | feed + hog cycle |

| Primary processing | 18% | labor + yield vs spec |

| Secondary processing | 7% | freezing energy + handling |

| Packaging & QA | 5% | pack style + inspection |

| Logistics & distribution | 12% | reefer rates + cold-store dwell |

| Downstream margin/cost-to-serve | 8% | distributor terms + claims |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Upstream (hog/carcass) | 45% | carcass value + primal demand |

| Primary processing | 22% | tighter trim/yield loss |

| Secondary processing | 10% | portioning + rework |

| Packaging & QA | 7% | QC intensity + labeling |

| Logistics & distribution | 10% | cube efficiency + lane risk |

| Downstream margin/cost-to-serve | 6% | service level + rejects |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Upstream (hog/carcass) | 53% | hog price baseline |

| Primary processing | 16% | plant efficiency |

| Secondary processing | 6% | freezing + handling |

| Packaging & QA | 4% | basic spec |

| Logistics & distribution | 14% | low value density → freight sensitivity |

| Downstream margin/cost-to-serve | 7% | inventory turns |

Frozen bone-in pork is priced and allocated through a whole-carcass system, not a SKU system.

That means:

USDA’s cutout framework explicitly reflects this “composite primal” view of carcass value, which is why primal-level monitoring is often more decision-useful than a single SKU quote history. [1]

Procurement teams often ask: “Why is the market down but my bone-in ham offer isn’t?”

The most common reasons are structural:

Below is how an intelligence service improves decisions without “feature-dumping”—capability → decision impact → governance action.

Decision it improves: build a short-list of suppliers that can actually meet your spec and eligibility needs.

Governance action: define an “approved-capable” pool by spec tier (commodity vs spec-tight) so buyers don’t improvise during shortages.

Decision it improves: select suppliers and negotiate terms based on total landed cost and reliability.

Governance action: require a normalized bid sheet before award—no award on non-comparable specs.

Decision it improves: when to lock, how much to lock, and what clause to use.

Governance action: adopt a layered-buy or index-linked approach only when driver signals justify it (and document why).

Decision it improves: reallocate volume, increase safety stock, or switch origin before service breaks.

Example risk signal: ASF remains a material tail risk in pork supply chains; separately, trade policy actions like China’s EU pork duties (effective Dec 17, 2025 for five years) can compound volatility by re-routing volumes and changing regional basis relationships. [3]

Decision it improves: portfolio design and auditability.

Governance action: add a quarterly “resilience coverage” KPI (e.g., % of volume with a qualified backup within X weeks lead time).

Objective: ensure you can switch supply within a defined lead time without breaking spec or compliance.

Objective: reduce claims and hidden yield loss.

Objective: reduce cost volatility without sacrificing service.

Objective: make supplier choices explainable and repeatable.

Frozen bone-in pork is a clean example of a broader procurement truth: price is rarely the only variable that matters.

Other categories where the same intelligence logic pays off:

In each case, the winning teams do three things consistently:

This category makes intelligence value visible because:

If you can run frozen bone-in pork with disciplined intelligence—spec-normalized buying, portfolio optionality, and event-to-action risk governance—you can apply the same operating model across most perishable and commodity-linked categories.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.