This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Frozen blueberries can look like a simple “IQF commodity” on a spec sheet, but procurement outcomes (price, continuity, and compliance) are usually decided upstream—by how fresh-market pull, harvest-week processing capacity, foreign-material control, and cold-chain reliability interact. This guide translates those realities into practical sourcing decisions and an operating cadence procurement leadership can run.

Analyzed at: Mar, 2026

Frozen blueberries look simple at the SKU level (IQF berries in a bag or carton), but the supply chain has two competing demand channels upstream (fresh vs. frozen) and two value-creation choke points midstream (sorting/foreign-material control and freezing/cold storage). Those realities drive most of the cost volatility and supply risk procurement teams experience.

Why this matters for procurement leadership: frozen blueberry pricing is not only “crop-driven”—it is also allocation-driven (who gets plant time, freezer space, and inventory) and spec-driven (how tight your defect/foreign material/size requirements are).

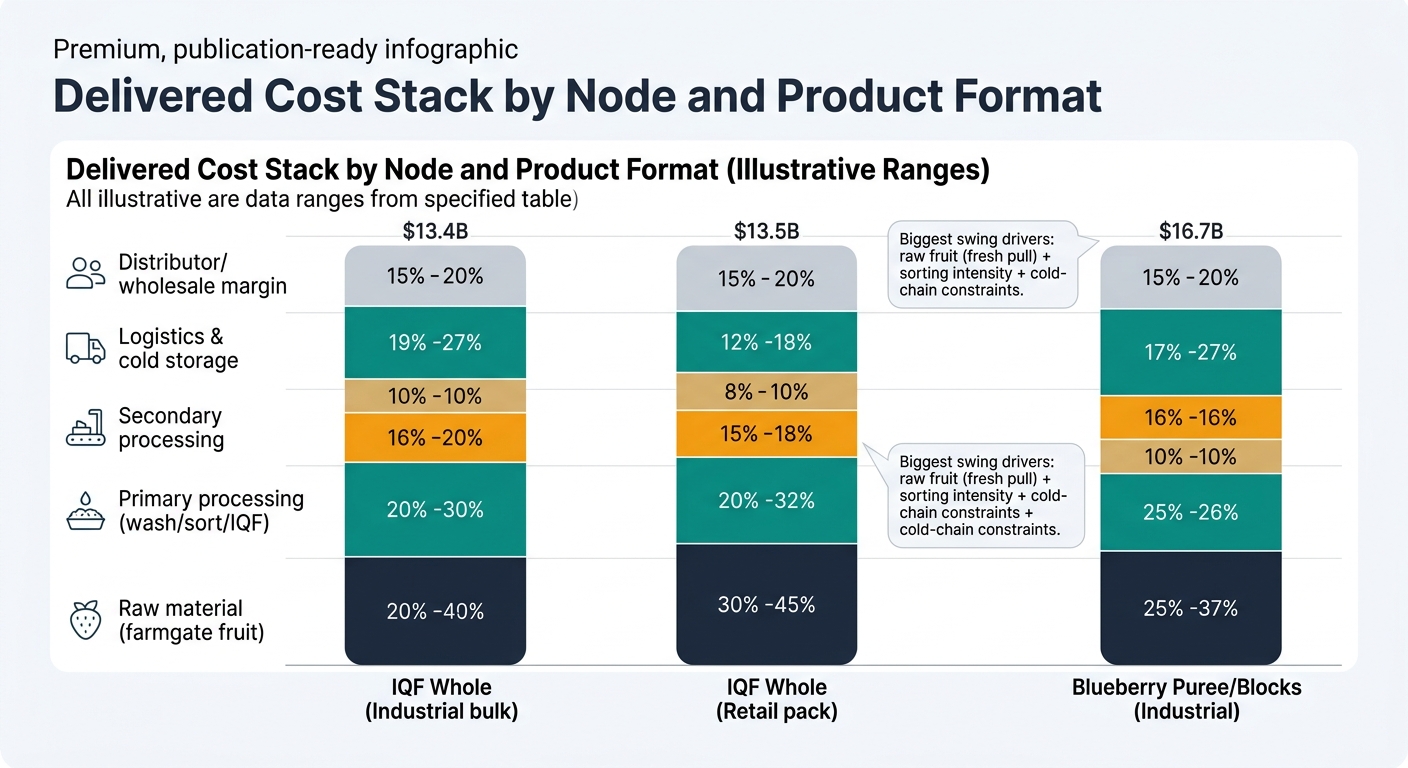

Below is an “inside the P&L” view of why two suppliers can quote very different numbers for what looks like the same frozen blueberry item.

Key insight: The largest single swing factor is often fresh-market competition (for cultivated/highbush). When fresh prices are attractive, less fruit is diverted to freezing, tightening frozen availability and lifting frozen prices (often with a lag).

Main cost drivers

Margin reality

Key insight: This is the first major value-add node. Procurement often underestimates how much sorting intensity and freezing throughput determine both cost and risk.

Main cost drivers

Operational reality you can use in negotiations

Tight specs (foreign material tolerance, defect limits, size distribution) usually require:

Key insight: Secondary processing can be a cost stabilizer (using rework streams) or a cost amplifier (additional conversion losses + QA).

Main cost drivers

Key insight: QA is not just compliance—it is working capital and service level. A lot can be “technically produced” but not “released for shipment.”

Main cost drivers

Quality governance anchor (common reference point)

USDA AMS defines U.S. grades/standards for frozen blueberries/berries and describes expectations around defects and quality scoring (useful as a neutral baseline when aligning QA and procurement on “must-have vs tradeable” attributes) [2].

Key insight: Cold chain cost is a blend of freight + cold storage + risk of delay. Delays are expensive because the product still needs power, space, and monitoring.

Main cost drivers

Key insight: The more “program-like” the business (retail continuity, penalties, OTIF expectations), the more margin is allocated to service reliability and risk absorption, not just product.

| Supply chain node | IQF Whole (Industrial bulk) | IQF Whole (Retail pack) | Blueberry Puree/Blocks (Industrial) |

|---|---|---|---|

| Raw material (farmgate fruit) | 45–60% | 35–50% | 35–55% |

| Primary processing (wash/sort/IQF) | 15–25% | 12–22% | 12–20% |

| Secondary processing | 0–3% | 0–3% | 8–18% |

| Packaging & QA | 4–8% | 10–18% | 5–10% |

| Logistics & cold storage | 8–18% | 8–18% | 8–18% |

| Distributor/wholesale margin | 5–12% | 8–15% | 5–12% |

Frozen blueberry supply is often the balancing channel for cultivated/highbush berries:

This is why procurement teams see:

Also, trade flows are not symmetric:

Procurement leaders often expect a clean pass-through: crop down → farmgate up → finished goods up. In frozen blueberries, three “disconnect mechanisms” intervene:

Practical takeaway: when a supplier says “market is up,” procurement needs to ask: Is that raw fruit, processing yield, energy, logistics, or simply allocation power? The right response (lock vs wait vs diversify vs spec-adjust) depends on which driver is real.

This section maps procurement decisions to the specific intelligence capabilities that change those decisions.

Establish a monthly market + risk review during key windows (pre-harvest planning, harvest/pack, and replenishment months), and a quarterly supplier bench refresh (add/remove alternates based on performance signals).

Frozen blueberry sourcing is a clean “training ground” for intelligence-driven procurement because it combines:

The same operating model transfers directly to categories procurement teams often co-manage:

The “meta-lesson” is consistent: price is an output. The controllable levers are coverage structure, supplier bench depth, spec governance, and risk-triggered decision cadence.

Frozen blueberries make the case to finance, QA, and operations because the value of intelligence shows up in measurable governance outcomes:

If procurement leadership wants one category to prove the operating model—frozen blueberries are ideal because small upstream changes (fresh pull, weather, processing throughput) quickly cascade into delivered cost and service outcomes.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.