This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

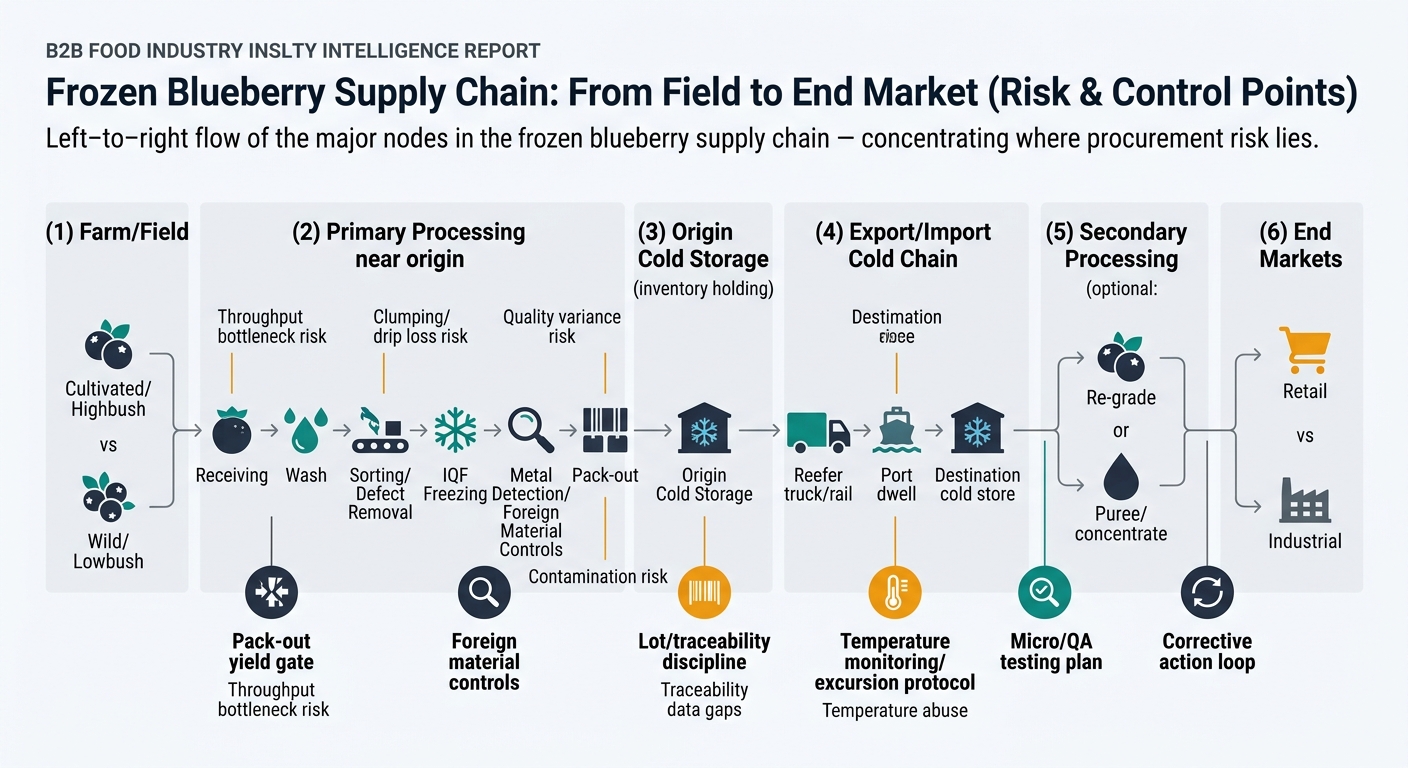

Frozen blueberries behave like a “simple” commodity only at the SKU level. In practice, procurement outcomes (cost, service, quality, and recall exposure) are driven by upstream physics: how quickly fruit is frozen after harvest, how defects/foreign material are removed, how lots are controlled and traced, and how the cold chain performs over months. This guide is written for experienced procurement and sourcing leaders who may be new to frozen blueberries; it translates category-specific realities into practical sourcing rules, governance, and intelligence-enabled decisions.

(Analyzed at: Mar, 2026)

Frozen blueberries look like a simple commodity, but procurement outcomes are mostly determined upstream of the RFQ—in how fruit is harvested, what gets diverted from fresh, how fast it reaches a freezer, and how the cold chain behaves for months.

Procurement implication: You’re not only buying “IQF blueberries.” You’re buying a set of agronomic risks + plant throughput constraints + cold-chain exposure + QA system maturity.

Key insight: In frozen blueberries, cost is dominated by the farmgate fruit price and pack-out yield, but the most avoidable cost for procurement is often downstream: claims, rework, expedited freight, and quality-driven yield loss. That avoidable cost is shaped by supplier capability and governance, not by the lowest quoted $/lb.

These are illustrative ratios to show where costs concentrate by product form. Actual ratios vary by origin, certification, crop year, freight market, and spec tightness.

| Supply Chain Node | Cost Ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Farm / raw fruit | 50% | Crop size + fresh diversion dynamics |

| Primary processing (wash/sort/IQF/pack-out) | 18% | Pack-out yield, labor, freezing energy |

| Packaging & QA | 7% | Testing plan, lotting/traceability rigor |

| Cold storage (origin + destination) | 8% | Storage duration, energy rates |

| Logistics & import handling | 10% | Reefer rates, port dwell, lane volatility |

| Distributor/wholesale margin | 7% | Intermediation level, service model |

| Supply Chain Node | Cost Ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Farm / raw fruit | 45% | Variety/firmness, harvest timing |

| Primary processing | 22% | Extra sorting, tighter defect removal, clump control |

| Packaging & QA | 10% | Retail pack-out, label compliance, higher QA frequency |

| Cold storage | 8% | Similar, but higher service expectations |

| Logistics & import handling | 8% | Temperature excursion sensitivity |

| Retail/brand margin | 7% | Channel economics |

| Supply Chain Node | Cost Ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Farm / raw fruit | 52% | Commodity fruit availability |

| Primary processing | 15% | Less IQF complexity, but still sanitation/controls |

| Packaging & QA | 6% | Simpler packaging |

| Cold storage | 9% | Often similar storage time |

| Logistics & import handling | 11% | Weight/handling, reefer exposure |

| Distributor/wholesale margin | 7% | Intermediation |

Structural fact: The frozen-blueberry market is a hybrid of (a) purpose-grown processing supply (notably wild) and (b) fresh-market overflow/diversion (cultivated). That means your “supply base” can tighten even when farms have fruit—because the fruit may be economically pulled into fresh channels.

A related U.S. indicator: Choices Magazine (citing USDA NASS) reports the share of cultivated blueberries bound for processing increased from ~40% (2010) to ~47% (2022)—evidence that processed volumes are not just “waste fruit,” they are structurally significant and shifting over time. [1]

Procurement implication: You must manage frozen blueberries more like a category with competing end-market pulls, not like a stable industrial input.

In frozen blueberries, the most common disconnect is:

Quoted $/lb (FOB/CIF) can look competitive while total landed cost worsens because of:

Food safety is not theoretical in frozen berries. FDA surveillance work on frozen berries has reported RT-qPCR detections of hepatitis A / norovirus genetic material in sampled products; regardless of the scientific nuance of what a detection means for infectious risk, it has increased buyer scrutiny on preventive controls, sanitation, and traceability expectations. [4]

Procurement implication: The “right” commercial comparison is not only price—it’s price × probability-weighted failure cost (claims, downtime, customer penalties, emergency buys).

Frozen-blueberry reality that matters: The category’s risk is concentrated in origin seasonality + processing bottlenecks + QA maturity + cold chain.

How it changes your decision:

Trade-offs that remain:

Operational outcome to measure:

How it changes your decision:

Trade-offs that remain:

Operational outcome to measure:

Frozen blueberries are a clean teaching case because the product is “simple,” but the risk is embedded in the chain. The same intelligence logic applies to other categories procurement teams often manage:

The common thread: categories where supplier capability and risk governance explain more variance in outcomes than the headline price.

Frozen blueberries force procurement teams to do three things well—things leadership can audit and operations can feel:

If you manage frozen blueberries with these signals and a structured supplier benchmark, you typically see improved landed cost stability, service continuity (OTIF), and audit-ready decision trails—without relying on heroics during disruptions.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.