This report is powered by Tridge market intelligence.

Every data point, price signal, and supply chain insight in this analysis is drawn from the same engine that procurement teams worldwide rely on daily. As you read, consider what this level of visibility could do for your category.

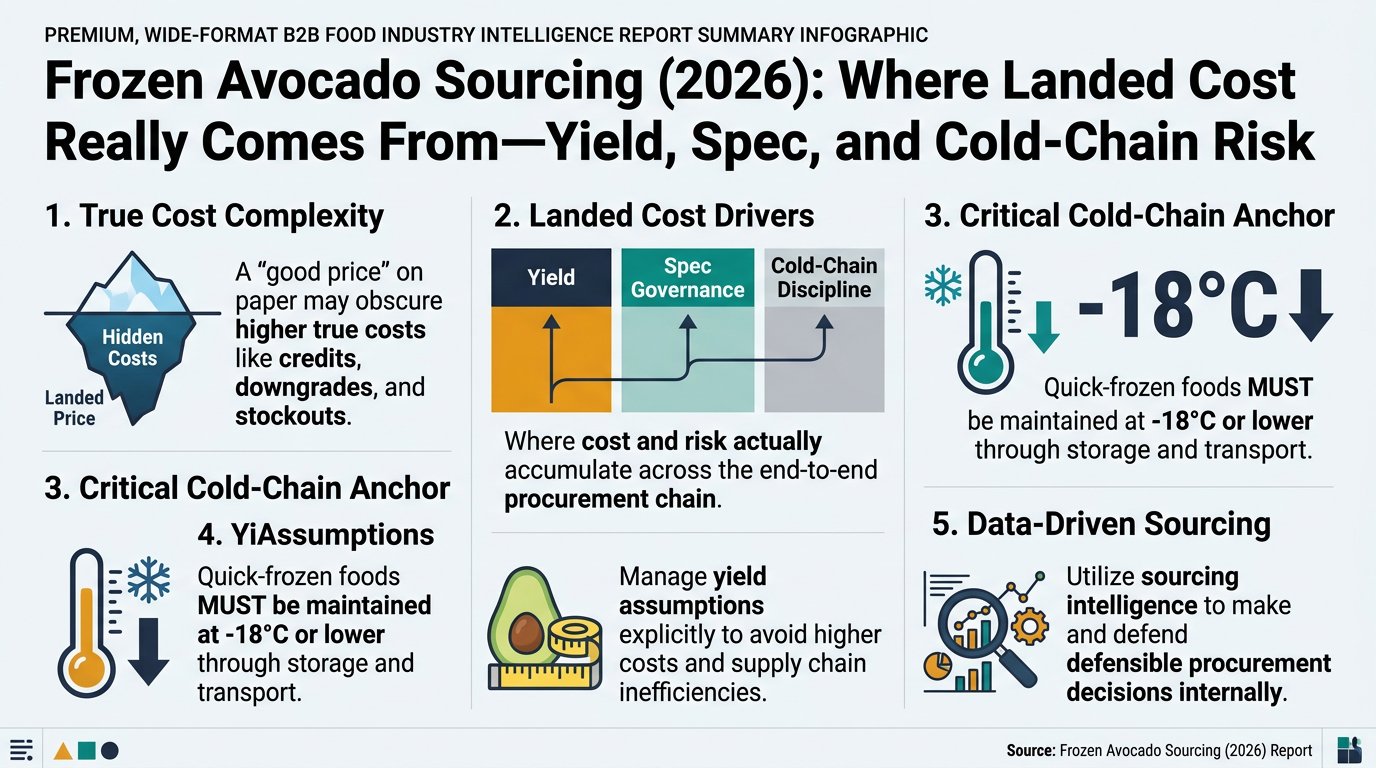

Frozen avocado is one of those categories where a “good price” on paper can still create higher true cost (credits, downgrades, stockouts) if yield assumptions, spec governance, and cold-chain discipline aren’t managed explicitly. This guide maps the end-to-end chain in procurement language, highlights where cost and risk actually accumulate, and shows how sourcing intelligence can be used to make decisions you can defend internally.

(Analyzed at: Mar, 2026)

Frozen avocado looks like a “simple” frozen fruit line item until you map what has to go right between orchard and your freezer.

Frozen-category non-negotiable: quick-frozen foods are typically handled and transported to maintain -18°C or lower through the cold chain, with defined tolerances [1].

Below, each node is written the way a category manager would use it: what cost accumulates here, what can go wrong, and what to measure.

Key insight: Frozen avocado is not insulated from the fresh market; it is economically “tethered” to fresh demand windows. When fresh prices rise, processors must either pay up for fruit or run below capacity—both push up your frozen price with a lag.

Procurement KPI to track: % of your cost exposure that is raw fruit-indexed vs. processing/logistics-indexed (even if you don’t formally index contracts).

Key insight: Plants are buying maturity, not just tonnage. Under-mature fruit increases trimming loss and degrades thaw texture; over-mature fruit raises browning risk and can increase overall quality risk.

What to capture in governance: lot maturity proxies (supplier-side), reject rates, and any “blend to spec” practices for pulp.

Key insight: Avocado has structurally high waste: peel + pit + defects. In foodservice yield references, edible portion is commonly ~67% for avocado (i.e., ~33% is non-edible before additional defect trimming) [2].

Negotiation reality: Two suppliers can quote the same $/lb frozen chunks but have materially different fruit-to-finished yield assumptions. If you don’t pressure-test yield, you’re negotiating blind.

Key insight: Color stability is not “free.” Oxidation control choices (process design, oxygen exposure, acidulants) change:

Key insight: IQF pieces carry a double premium: (1) energy-intensive freezing and (2) tighter spec sensitivity (uniform cut size, minimal browning, low defects). Pulp/puree can often be standardized via blending, reducing some variability.

What to benchmark: defect limits, cut-size tolerances, and complaint rates by format (chunks vs. pulp).

Key insight: Even when product stays safe, temperature abuse degrades texture and color, turning into commercial loss (downgrades, credits, customer churn). The cold chain expectation for quick-frozen foods is -18°C or lower in storage/transport (subject to permitted tolerances) [1].

Governance metric: temperature excursion incidents per lane + claim value per incident.

Key insight: Importers/distributors often price not just product but inventory risk (frozen working capital), case-pick complexity, and service expectations.

Procurement lever: align pack formats/MOQs with your demand profile to avoid paying for someone else’s safety stock.

These ratios are modeled to show where cost tends to concentrate by product form. Actual splits vary by origin, season, spec tightness, freight conditions, and whether you buy direct vs. via importer.

| Supply Chain Node | Cost Ratio (% of landed cost) | What typically moves it |

|---|---|---|

| Orchard & harvest (fruit) | 40% | Fresh-market pull; maturity/yield |

| Conditioning + sorting | 6% | Reject rates; energy |

| Peel/pit/trimming | 14% | Labor + yield loss (~33% non-edible baseline before defects) [2] |

| Cutting + anti-browning controls | 7% | Oxidation management; additives |

| Freezing + packing | 13% | Energy + barrier films |

| Cold-chain logistics | 12% | Reefer rates; port dwell; cold storage |

| Import/distribution margin | 8% | Inventory risk + service level |

| Supply Chain Node | Cost Ratio (% of landed cost) | What typically moves it |

|---|---|---|

| Orchard & harvest (fruit) | 38% | Fruit size/grade requirements |

| Conditioning + sorting | 7% | Stricter grading |

| Peel/pit/trimming | 16% | Higher defect rejection |

| Processing controls (color/texture) | 8% | Tighter spec and handling |

| Freezing + packing | 14% | Higher packaging standards |

| Cold-chain logistics | 10% | Similar lanes, higher claim sensitivity |

| Import/distribution margin | 7% | Retail compliance, chargebacks |

| Supply Chain Node | Cost Ratio (% of landed cost) | What typically moves it |

|---|---|---|

| Orchard & harvest (fruit) | 45% | Fruit price dominates |

| Conditioning + sorting | 5% | Can absorb more variability |

| Peel/pit/trimming | 12% | Still labor/yield intensive |

| Pulping + standardization | 10% | Blending, QA, spec targets |

| Freezing/packing (blocks/totes) | 10% | Pack type (tote vs. bag) |

| Cold-chain logistics | 10% | Weight/volume efficiency |

| Import/distribution margin | 8% | Lower case-pick complexity |

The important structural fact: A large portion of your “raw material” spend is paying for non-edible mass (peel/pit) plus variable defect trimming. Even before defects, common edible yield references put avocado around ~67% edible portion [2].

Buyer decision this supports: when to pay for tighter specs vs. when to widen tolerances (especially for pulp) to protect continuity and cost.

Frozen price behavior often confuses non-specialists because it’s not a single commodity price—it’s a stack of linked markets.

Context signal: USDA reports Mexico’s avocado production forecast at 2.75 MMT for 2025 (fresh avocado context that influences processing economics) [3].

This is how sourcing intelligence changes category outcomes in frozen avocado—without pretending it replaces audits or QA.

Frozen avocado is a clean example of a broader procurement pattern: when yield + processing + cold-chain matter, price alone is a trap.

Comparable categories many procurement teams also buy:

The transferable lesson: intelligence is most valuable where conversion yield and spec governance determine your true landed cost and continuity.

Because it forces the right procurement behavior:

Net effect: better decisions you can defend—more stable landed cost, fewer disruptions, and clearer category governance.

Take Your Sourcing Intelligence to the Next Level

The insights in this report are just the starting point. Tridge Eye gives you real-time market signals, origin risk alerts, and price benchmarks — so you can act before the market moves.