This playbook is written for procurement leaders who already know how to run competitive bids—but need a practical lens for frozen açaí, where seasonality, processing capacity, and cold-chain volatility can break “lowest $/kg wins.” The goal is to help you separate true cost movement from risk premium, contract the right components, and build executable dual-sourcing.

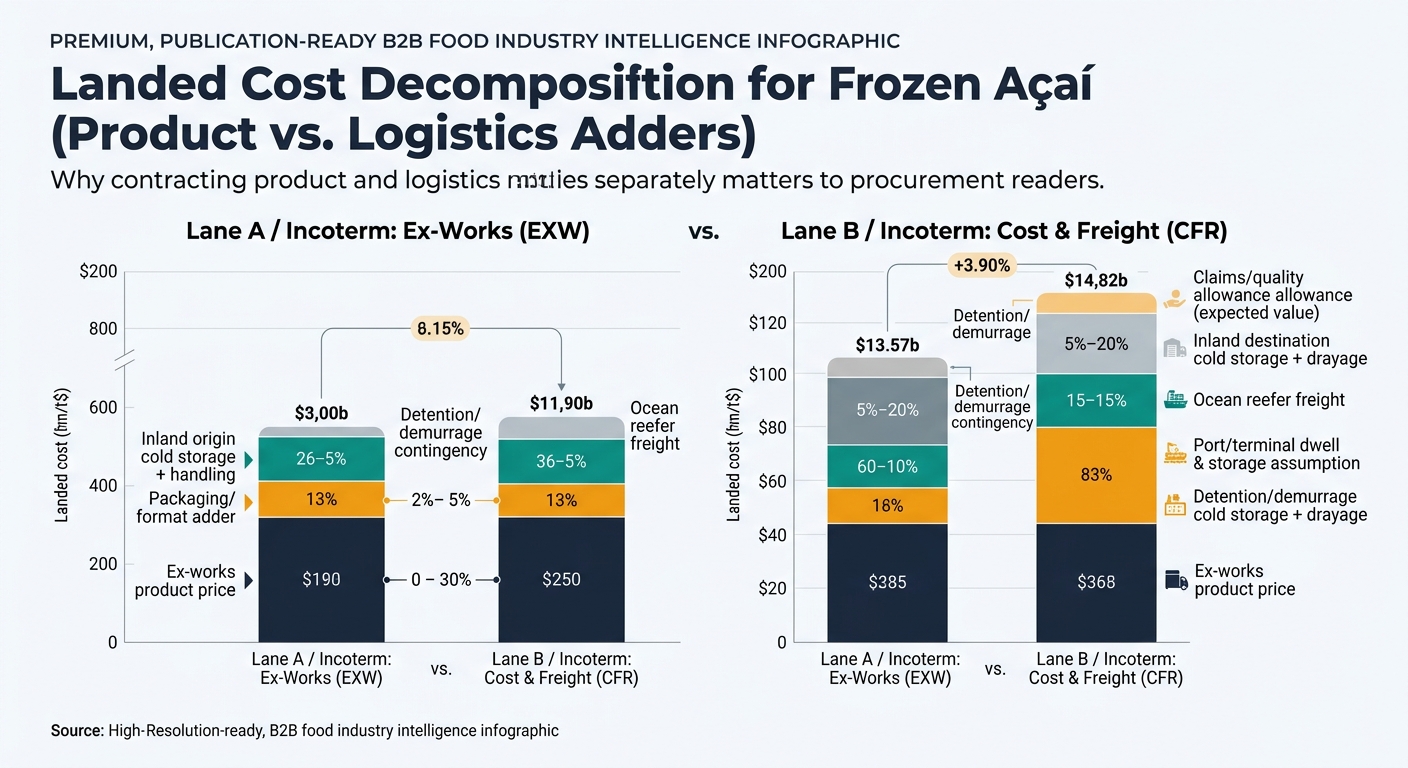

Quick Win: In your next RFQ, require suppliers to quote with two separate lines—ex-works product and logistics adders (freight, cold storage dwell assumptions, detention). You’re not asking for their margin; you’re forcing transparency on what’s moving.

Quick Win: Define “real dual-source” as at least 70/30 or 80/20 across two operationally independent supply paths (different plants or different logistics lanes), not just two vendor names.

| Dimension | Before (traditional) | After (intelligence-driven) |

|---|---|---|

| Pricing posture | Annual/biannual reset; ad-hoc spot buys | 90–180 day coverage decisions tied to inventory + logistics signals |

| Supplier leverage | Incumbent sets the narrative (“fruit is up”) | Buyer tests narrative vs. external signals + peer benchmarks |

| Service level | Reactive expediting during delays | Safety stock sized to lead-time volatility (P50 vs P90) |

| Quality cost | Claims handled case-by-case | Spec drift tracked by supplier/season; corrective actions tied to re-award |

Quick Win: Build a one-page “açaí risk register” that triggers actions (e.g., pre-booking, shifting volume, raising safety stock) based on lane reliability, supplier slot availability, and claims trend—not on anecdotal updates.

Quick Win: Require temperature recorder data (or equivalent evidence) on a defined sampling rate for high-risk lanes; tie noncompliance to chargebacks or downgrade rules.

(Analyzed at: Apr, 2026)

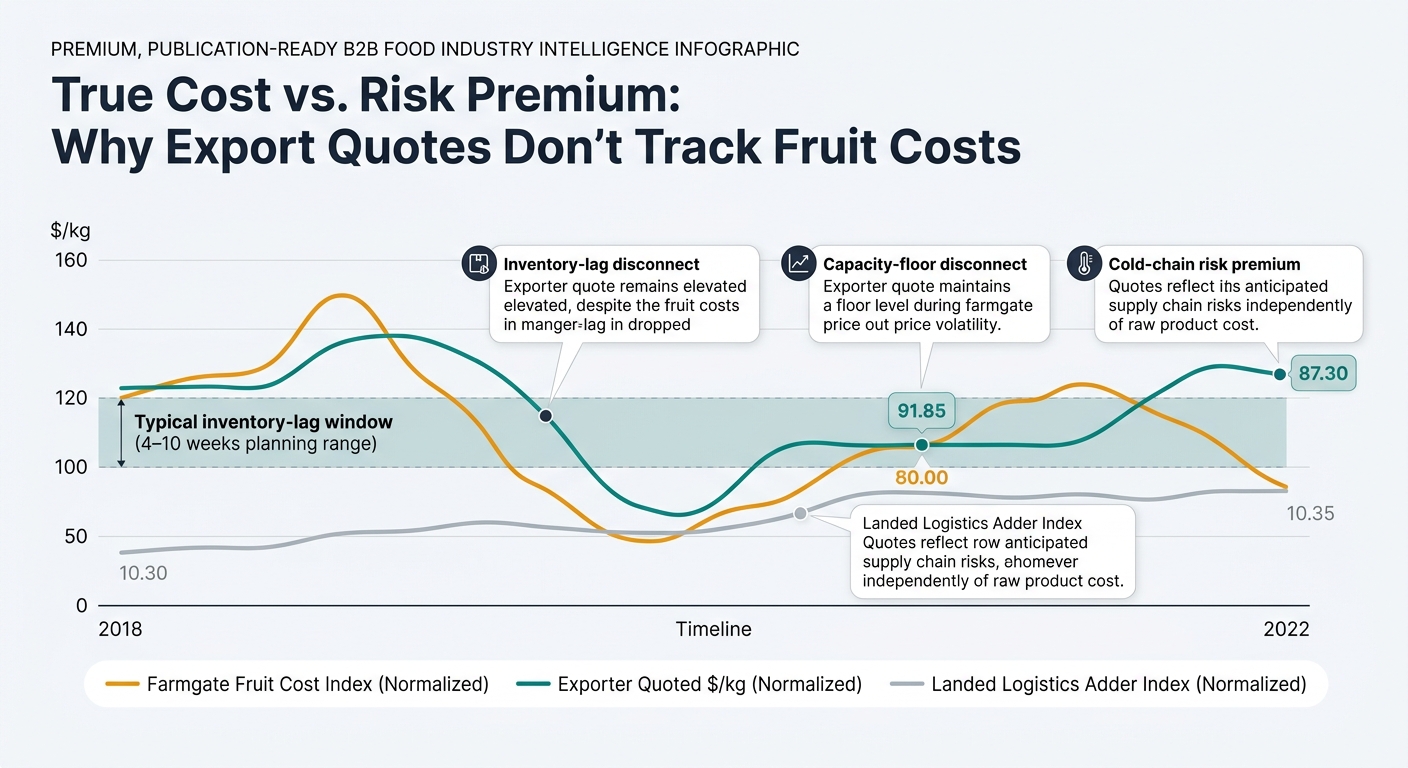

Brazil’s açaí supply remains structurally seasonal and concentrated, with a large share of harvest commonly described as occurring in a short “~100‑day” peak window—so the real negotiation is still about who gets plant slots and cold-chain priority when the window tightens, not just whose fruit narrative sounds best. [1] For your next contract, split pricing into (1) a 90–180 day product mechanism and (2) a documented logistics adder with caps, then reserve capacity by running a real 10–20% volume through an alternate lane before peak pressure builds. If you wait until allocation season to “activate” a backup, the premium you pay (plus the downstream cost of claims and rescheduling) can easily dwarf the unit-price delta you fought for in the bid—especially on programs large enough that one or two late reefers can disrupt a full production cycle.