This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

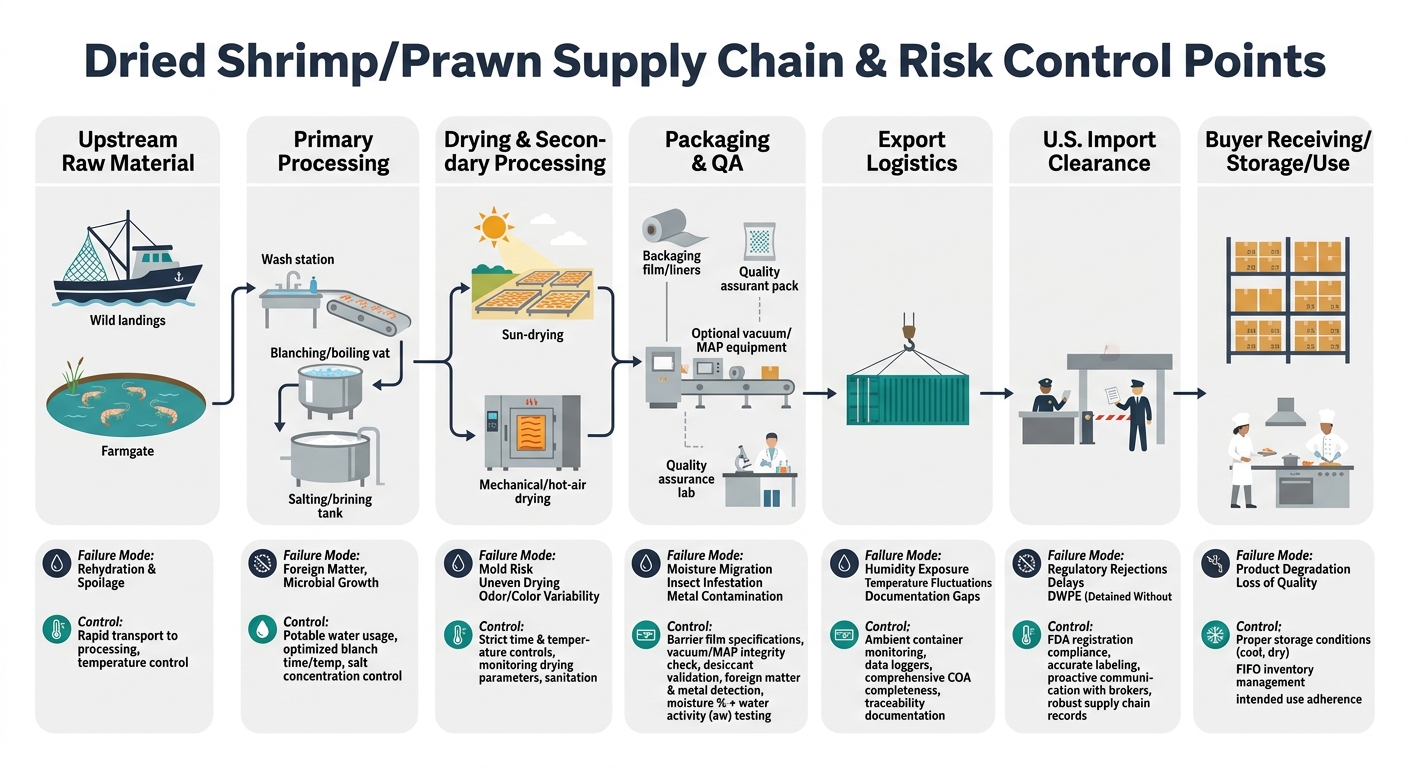

Dried shrimp/prawn can look like a simple, shelf-stable ingredient, but procurement outcomes (cost, continuity, and claims exposure) are usually driven by a few fundamentals: upstream raw-material variability, the supplier’s ability to control moisture/water activity and contamination risk during drying, and U.S. import compliance discipline (especially for aquaculture-origin shrimp/prawns where drug-residue enforcement can create sudden holds and cost). This guide translates those realities into practical award, contracting, and governance actions for procurement & sourcing management teams.

(Analyzed at: Apr, 2026)

Dried shrimp/prawn looks like a “simple, shelf-stable ingredient,” but procurement outcomes are driven by upstream biology + processing yield + moisture/water activity control + import compliance.

Procurement implication: dried shrimp/prawn is not a single commodity. It is a spec-defined risk bundle (species/grade + moisture/aw + additive policy + hygiene controls + packaging + documentation) that must be governed like a high-risk ingredient.

Below is a procurement-oriented view of cost build-up. Percentages are illustrative modeling ranges; actuals vary by origin, grade, yield, labor intensity (esp. peeling), and packaging format.

Key insight: The raw shrimp price and size distribution dominate the economics of dried shrimp/prawn. When disease or seasonal shifts change what sizes are available, your dried spec can become structurally “harder to make,” not just “more expensive.”

Key insight: This node determines the baseline hygiene and uniformity. If upstream handling is weak, drying does not “fix” it.

Key insight: Drying is a yield and risk conversion step: you’re paying for water removal, but you’re also buying the supplier’s ability to hit stable moisture and water activity without contamination.

Key insight: Packaging is not “just a bag.” For dried shrimp/prawn, packaging is a humidity-control system.

Key insight: Because product is shelf-stable, many buyers underestimate inventory carrying cost + quality drift risk (rehydration, oxidation, infestation) across long ambient lanes.

Key insight: The “cheapest FOB” supplier can be the most expensive landed option once you price claims, delays, and rework.

Modeled as % of final delivered cost to a U.S. buyer; ranges reflect typical variance by origin, packaging, and quality regime.

| Supply chain node | Cost ratio (% of final delivered cost) | Notes |

|---|---|---|

| Upstream raw shrimp/prawn | 45–60% | Dominated by landing/farmgate price and size mix |

| Primary processing | 8–12% | Sorting + blanching/salting labor/energy |

| Drying & secondary processing | 10–18% | Yield loss + energy or weather risk |

| Packaging & QA | 4–8% | Liners/cartons + basic testing |

| Logistics & duties + inventory carry | 10–16% | Port dwell time and working capital matter |

| Importer/distributor margin | 6–12% | Risk premium varies with compliance history |

| Supply chain node | Cost ratio (% of final delivered cost) | Notes |

|---|---|---|

| Upstream raw shrimp/prawn | 35–50% | Higher conversion cost reduces raw share |

| Primary processing | 10–15% | More grading and prep labor |

| Drying & secondary processing | 15–25% | Peeling/shelling yield + labor is material |

| Packaging & QA | 5–10% | Often tighter foreign matter and micro specs |

| Logistics & duties + inventory carry | 10–16% | Similar lanes; higher value increases finance cost |

| Importer/distributor margin | 6–12% | Premium for consistent compliance |

| Supply chain node | Cost ratio (% of final delivered cost) | Notes |

|---|---|---|

| Upstream raw shrimp/prawn | 30–45% | Can use fines/off-cuts, but quality risk can rise |

| Primary processing | 8–12% | Baseline hygiene still crucial |

| Drying & secondary processing | 20–30% | Milling, sieving, foreign matter control |

| Packaging & QA | 6–12% | Higher oxidation/odor control needs |

| Logistics & duties + inventory carry | 10–16% | Powder is sensitive to moisture pickup |

| Importer/distributor margin | 6–12% | Higher due to spec sensitivity |

Dried shrimp/prawn supply is a “sink” for variability upstream: it absorbs small sizes, off-grades, and seasonal gluts, but it is also the first product to get squeezed when upstream supply tightens or size distributions shift.

Procurement implication: you should treat dried shrimp/prawn as seasonal + disruption-sensitive, even though it ships ambient and stores well.

In this category, paid-price variance is rarely just negotiation skill. It’s usually a mismatch between:

FDA import enforcement can include Import Alerts that allow detention without physical examination (DWPE) for future shipments when violations are identified. FDA has also issued shrimp/prawn-specific communications referencing nitrofuran/chloramphenicol residues and DWPE actions (e.g., Peninsular Malaysia update).

This is where an intelligence-driven approach improves decision quality without pretending to replace QA.

Procurement intelligence supports four buyer decisions:

Intelligence can prioritize where to investigate; it does not replace:

Decision threshold: Maintain at least one document-ready alternate per critical spec (shell-on bulk, peeled, powder).

Trade-off: Slightly wider spec may reduce unit price and increase supplier options, but must be validated by QA and product teams.

Decision threshold: If port dwell time or inspection delays rise, increase buffer stock before peak humidity periods.

The pattern here—spec-defined risk + upstream shocks + compliance exposure—is not unique to dried shrimp.

Examples procurement teams commonly manage in parallel:

Transferable lesson: procurement intelligence is most valuable when quality and compliance risks create hidden costs that are not visible in a quote sheet.

This category is a strong demonstration case because it combines:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.