This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

This guide is written for Procurement & Sourcing Management teams who are strong buyers in other ingredient categories but want a practical, decision-led view of dried coriander leaf (dried cilantro) sourcing. The goal is to help you connect what’s happening upstream (agriculture + dehydration) to what you experience downstream (quote volatility, spec failures, micro/residue holds, and emergency switching). It also shows where procurement intelligence changes the decision—supplier strategy, contracting, and risk posture—without pretending it replaces QA testing, audits, or regulatory counsel.

(Analyzed at: Apr, 2026)

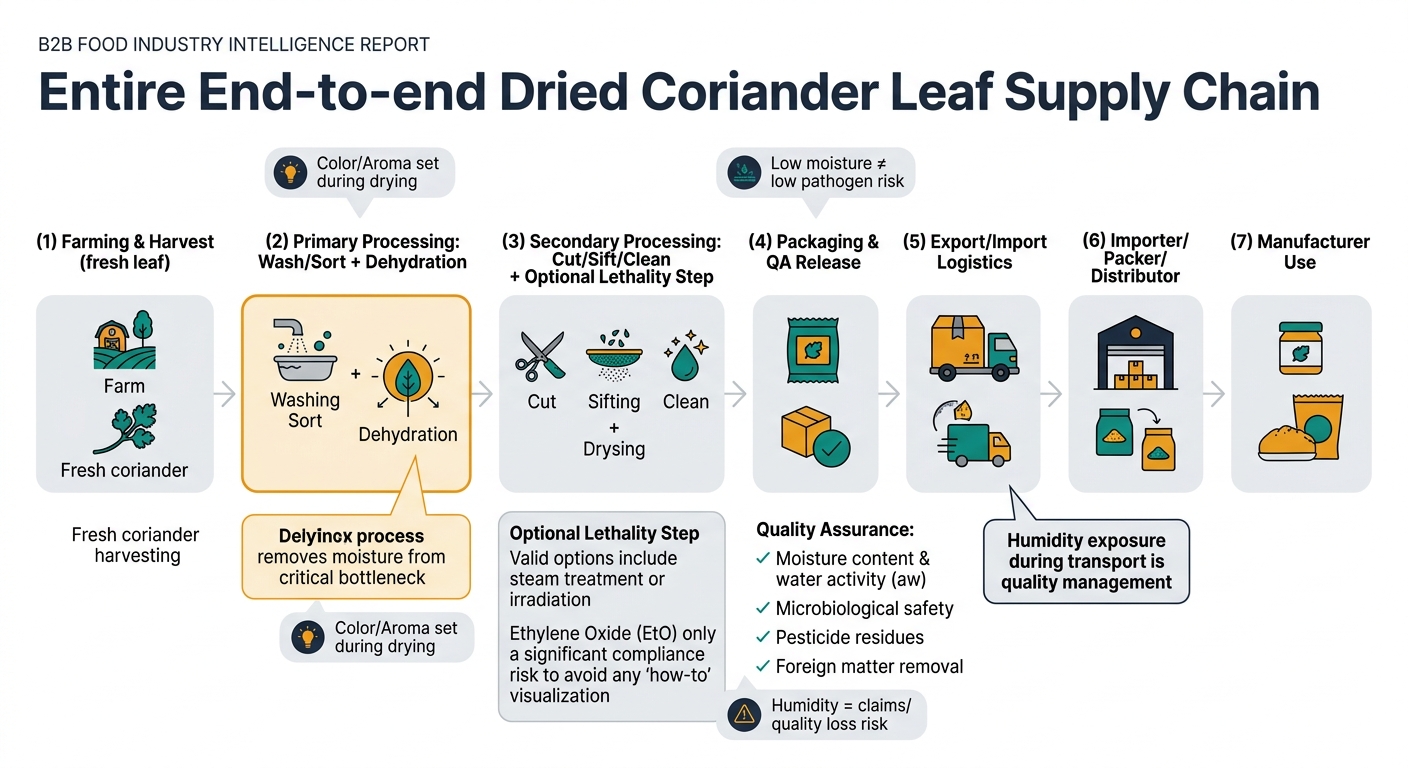

Dried coriander leaf (often sold as coriander leaf flakes; sometimes labeled as dried cilantro in North America) is not a “spice” supply chain in the way coriander seed is. It is a dehydration supply chain built around converting a highly perishable green leaf into a shelf-stable ingredient.

Key insight: Dried coriander leaf cost starts as a fresh-leaf economics problem. Yield swings and harvest labor drive volatility more than many procurement teams model.

Margin reality: Farmgate margins are often thin; volatility is mostly yield + labor.

Key insight: Dehydration is where cost and risk concentrate because it is energy- and throughput-constrained and strongly determines whether the material can meet micro + color expectations.

Margin reality: Processors with reliable dehydration control and export-grade QA systems typically earn a premium.

Key insight: This is where your spec language turns into real money. Tight cut-size distributions, low dust, low foreign matter, and validated lethality steps create measurable cost adders.

Margin reality: Secondary processors often capture margin via “spec compliance capability” (not just volume).

Key insight: For dried coriander leaf, QA cost is not overhead—it is the price of market access and recall avoidance.

Key insight: The main logistics risk is not temperature—it is humidity exposure that drives caking, mold risk, aroma loss, and claims.

Key insight: In many buying programs, the “supplier” is an importer/packer. Their margin often reflects risk absorption: inventory, QA release, and compliance liability.

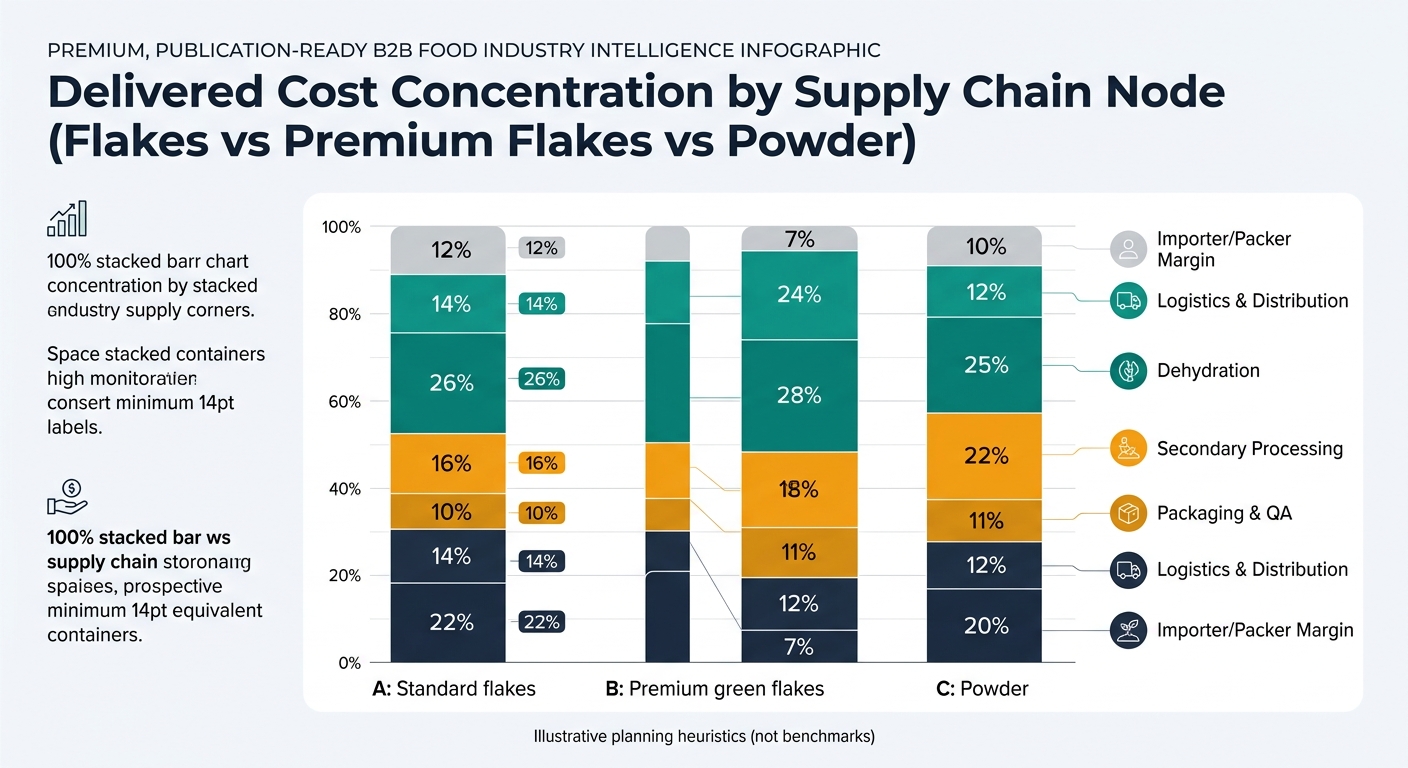

These ratios are modeled to show where cost concentrates by product form. Actual splits vary by origin, season, kill-step policy, and spec tightness. Treat as planning heuristics, not benchmarks.

| Supply Chain Node | Cost Ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Farming/harvest | 22% | yield + labor |

| Dehydration (primary processing) | 26% | energy + capacity |

| Secondary processing (cut/sift/clean) | 16% | fines removal + foreign matter |

| Packaging & QA | 10% | testing + barrier packaging |

| Logistics & distribution | 14% | freight + consolidation |

| Importer/packer margin | 12% | inventory + QA release |

| Supply Chain Node | Cost Ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Farming/harvest | 24% | agronomy + harvest timing |

| Dehydration (primary processing) | 28% | controlled drying to protect color/aroma |

| Secondary processing (tight cut/low dust) | 18% | yield loss to meet spec |

| Packaging & QA | 11% | more frequent testing + tighter release |

| Logistics & distribution | 12% | humidity control practices |

| Importer/packer margin | 7% | less “trading” margin, more spec-driven |

| Supply Chain Node | Cost Ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Farming/harvest | 20% | yield |

| Dehydration (primary processing) | 25% | energy |

| Secondary processing (milling + controls) | 22% | milling loss + metal control |

| Packaging & QA | 11% | micro + residues, more dust control |

| Logistics & distribution | 12% | freight |

| Importer/packer margin | 10% | inventory + QA release |

For dried coriander leaf, drying doesn’t just remove water—it concentrates both value and risk:

Procurement implication: the best leverage point is upstream process capability selection, not late-stage inspection.

In dried coriander leaf, buyers often expect a simple rule: “higher price = safer/better.” In practice:

Procurement implication: you need two linked views—market price drivers and compliance/food-safety gating factors.

Below is how procurement intelligence changes specific management decisions in dried coriander leaf.

Use supplier benchmarking & qualification intelligence to compare:

Procurement action:

Measurable outcomes:

Use price intelligence & cost-driver analysis to separate:

Procurement action:

Measurable outcomes:

Use risk monitoring (early warning) tied to triggers:

Procurement action:

Measurable outcomes:

The “drying multiplies everything” lesson applies across herbs, spices, and botanicals:

Management takeaway: once you build a repeatable intelligence-to-action governance model for dried coriander leaf, you can reuse it across your broader dry ingredients portfolio.

Dried coriander leaf is a high-leverage example because it forces procurement to manage cost, continuity, and compliance simultaneously:

If procurement leadership can make dried coriander leaf sourcing auditable and resilient—through benchmarking, alternate scenario planning, and risk triggers—then the same operating model scales to other botanicals where the cost of a single quality or compliance failure is far larger than the unit price premium.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.