This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Dried common beans look like a straightforward commodity purchase, but most cost overruns and service failures are decided before your PO is cut—by crop-year grade, how much “field-run” turns into your spec after cleaning/sorting (spec yield), and inland logistics basis. This guide translates those realities into procurement decisions you can govern (coverage, supplier strategy, spec tiering) and measure (OTIF, claims, price variance vs benchmark).

(Analyzed at: Apr, 2026)

Dried common beans (Phaseolus vulgaris—pinto, black, navy, kidney, etc.) look like a simple commodity, but procurement outcomes are usually decided upstream of your PO—at harvest quality, cleaning/sorting yield, and inland logistics.

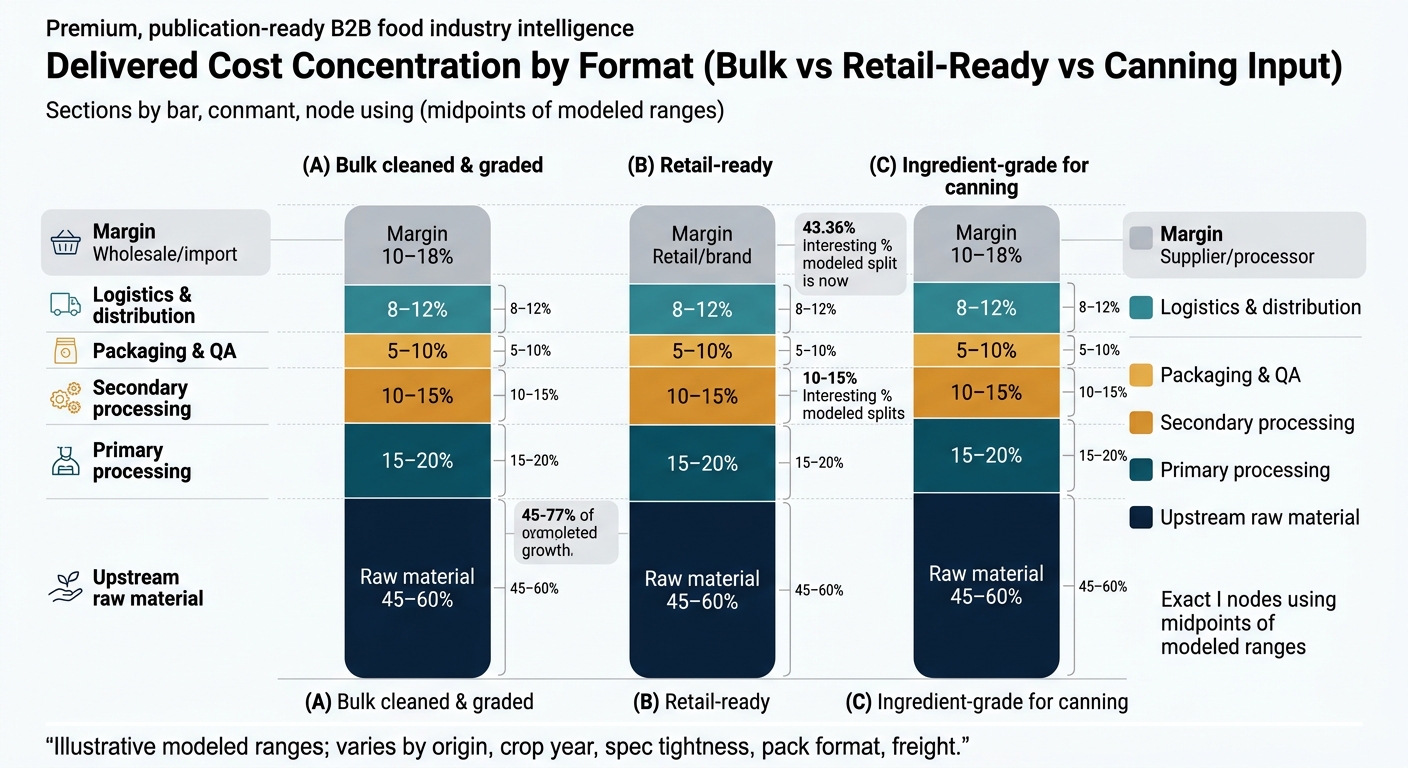

Below is a procurement-oriented “margin map” of where cost accumulates and where suppliers earn (or lose) money.

Key insight: Farm-level variability determines what primary processors can actually turn into exportable/retail-grade lots.

Procurement implication: When the crop is “average” on volume but below-average on grade, you will see FOB prices hold up (or rise) even if farmgate prices soften—because processors are losing yield in sorting.

Key insight: Primary processing is where “commodity” becomes “spec.” This node controls defect economics.

Specs are real money: A tighter spec can increase removal rates and reduce available supplier pool; the price impact is not linear.

Reference spec reality (not illustrative): USDA commodity specifications for dry edible beans explicitly define tight parameters for particular deliveries (e.g., moisture ranges and very low foreign material/defect thresholds for some items) and require grade U.S. No. 1 for many deliveries, with inspection tied to FGIS documentation. [1]

Key insight: Secondary processing changes your risk profile: you trade higher conversion cost for more consistent functionality.

Procurement implication: If your downstream cost of failure is high (rework, line downtime, customer complaints), secondary-processed options can reduce total cost even when unit price is higher.

Key insight: Packaging is not just materials—it’s lot integrity + claims prevention.

Procurement implication: The cheapest pack is often the most expensive after claims—especially if moisture ingress or infestation triggers rejections.

Key insight: Beans ship well when dry and protected, but they are highly sensitive to moisture ingress, odor contamination, and delay.

Procurement implication: A “good FOB” can be a bad landed cost if inland basis and congestion are moving against you.

Key insight: Downstream players price in service reliability and quality consistency. If your supply is unstable, you pay a premium in expediting, substitutions, and customer penalties.

These are modeled ranges to show where cost concentrates. Actual ratios vary by origin, crop year, spec tightness, pack format, and freight. Use them to focus negotiations (what to ask, what to audit), not as a universal should-cost.

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Upstream raw material | 45–60% | crop yield/grade, farmgate price, FX |

| Primary processing | 10–18% | sorting yield loss, optical sorting intensity |

| Secondary processing | 0% | N/A |

| Packaging & QA | 3–7% | sack/liner choice, QA/testing |

| Logistics & distribution | 12–22% | inland basis, ocean freight, demurrage |

| Wholesale/import margin | 8–15% | service level, credit terms |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Upstream raw material | 30–45% | crop year spreads by class |

| Primary processing | 10–16% | defect removal and blending |

| Secondary processing | 0% | N/A |

| Packaging & QA | 12–22% | film, printing, labor, compliance |

| Logistics & distribution | 10–18% | destination DC complexity |

| Retail/brand margin | 12–25% | promo cadence, service reliability |

| Supply chain node | Cost ratio (% of delivered cost) | What moves it most |

|---|---|---|

| Upstream raw material | 35–50% | variety availability, grade |

| Primary processing | 12–20% | size uniformity, defect limits |

| Secondary processing | 0–10% | optional conditioning, additional QA |

| Packaging & QA | 4–10% | bulk handling, COA rigor |

| Logistics & distribution | 12–20% | inland + ocean + scheduling |

| Supplier/processor margin | 8–15% | performance expectations, penalties |

Structural fact: In dried beans, the market often clears on exportable/retail-grade availability, not on total harvested tonnage.

That means two suppliers quoting the “same origin and same bean class” can have very different economics depending on:

Management takeaway: If you only benchmark on price/MT, you miss the biggest driver of supplier behavior: how much margin they must earn to cover shrink and claims.

Procurement teams often expect a simple story: “big crop = lower price.” Beans break that logic because quality and storability create a second dimension.

Procurement implication: Your negotiation posture should be anchored to (a) grade availability, (b) logistics basis, (c) supplier sorting yield, not only a generic market index.

These are repeatable failure modes when teams are experienced procurement leaders—but new to beans.

Start from the decision you need to make, then apply only the intelligence that improves that decision.

Use price intelligence & market drivers to separate:

Outcome: lower price variance vs benchmark; fewer emergency buys.

Use supplier discovery + benchmarking to build a qualified bench by:

Outcome: reduced concentration risk; faster time-to-switch.

Use alternative identification + benchmarking to build a two-tier strategy:

Outcome: fewer stockouts and fewer quality incidents on the SKUs that matter most.

Use performance analysis to standardize:

Outcome: faster approvals; clearer supplier accountability.

The “beans lesson” generalizes: quality yield + logistics basis + governance often dominate unit price.

If you treat these as “simple commodities,” you’ll repeatedly pay hidden premiums (claims, expediting, line downtime) that never show up in your bid sheet.

Dried common beans are a clean demonstration of what procurement intelligence should do:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.